Global Economies Flash Warning of Sharp Slowdown Business activity in the U.S., Europe and Japan fell in August, according to new surveys, pointing to slowing global economic growth as higher prices weaken consumer demand and the war in Ukraine scrambles supply chains.

U.S. companies reported a sharp drop in business activity in August in a broad-based decline led by services companies, though manufacturing slowed as well. High inflation, material shortages, delivery delays and interest-rate rises all weighed on business activity, the S&P Global survey said.

The composite purchasing managers index for the U.S. economy—which measures activity in both the manufacturing and services sectors—was 45.0 in August, down from 47.7 in July. That marked the second consecutive month with a decline and was the lowest reading since May 2020, early in the pandemic. A reading below 50 indicates a contraction; a reading above that level indicates growth.

“Gathering clouds spread across the private sector as services new orders returned to contractionary territory, mirroring the subdued demand conditions seen at their manufacturing counterparts,” said Siân Jones, senior economist at S&P Global Market Intelligence. (…)

Europe business activity also declined for a second month in a row amid a renewed rise in energy prices over uncertainty about Russia’s willingness to maintain its already reduced supply of natural gas ahead of the heating season. (…)

S&P Global said its composite purchasing managers index for the eurozone fell to 49.2 in August from 49.9 in July, reaching an 18-month low. Manufacturing output fell for a third straight month, while the services sector narrowly avoided a contraction. Businesses in both sectors reported a decline in new orders, which points to weakness in the months to come, while factories reported a buildup in inventories as goods remained unsold.

“This glut of inventories suggests little prospect of an improvement in manufacturing production any time soon,” said Andrew Harker, an economist at S&P Global. (…)

The PMI for Germany pointed to the sharpest decline in business activity since June 2020, while the measure for France pointed to the first decline in activity since the first wave of the pandemic.

The PMI for U.S. service providers fell to 44.1 so far in August, from 47.3 in July. Businesses encountered more client hesitancy in placing new work, leading to a steep decline in new orders, S&P Global said.

U.S. service providers are raising prices more slowly than they have in 17 months as softer orders and more competition lead to pricing moderation. Input costs also have moderated for service providers, but wage, supplier, and transportation costs continue to weigh on businesses.

U.S. manufacturers’ output contracted for a second straight month as they faced softening demand and continued supply-chain issues, though manufacturers also registered the slowest rise in cost burdens since January 2021. (…)

Markit’s PMI surveys, particularly its flash surveys out about one week before the complete ones, received little media attention until last month after S&P Global took Markit over and is doing a better job at promoting its survey findings. Since 2009, I have dutifully reposted Markit’s PMIs which are superior to the ISM’s which receive most media’s attention.

From now on, I will post the WSJ or Bloomberg pieces because of the color they give to the news, but I will add what might be left out as well as charts and the links to the respective pdfs.

From the U.S. flash PMI survey:

- The rate of contraction outpaced anything recorded outside of the initial pandemic outbreak since the series began nearly 13-years ago.

- The reduction in output was broad-based, with manufacturers and service providers registering lower activity. Service sector firms recorded the steeper rate of decline, as activity fell sharply, while goods producers saw a modest drop in output.

- August data signalled a renewed contraction in overall sales as manufacturers and service providers struggled with subdued demand conditions. Though modest, the drop in new orders was the sharpest in over two years. New sales were weighed down by weak domestic and foreign client demand, as new export orders fell further and at a solid pace.

- The rate of input cost inflation eased for the third month running midway through the third quarter, with input prices rising at the slowest pace for a year-and-a-half. That said, the pace of increase in operating expenses remained historically marked, with firms linking hikes in cost burdens to increased interest rates, and higher prices for a range of raw materials and transportation. Some companies also stated that increases in wages to attract and retain workers had placed additional pressure on expenses.

- In line with the trend for cost burdens, firms increased their selling prices at the softest pace in 18 months in August. The softer rise in output charges was linked to efforts to pass through any concessions to customers to encourage the placement of orders. That said, the rate of inflation was marked overall and faster than in any period before March 2021.

- Employment rose at the slowest pace in 2022 to date. Although some companies continued to note challenges finding suitable replacements for voluntary leavers, a growing number of firms stated that uncertainty and rising costs led them to delay the immediate replacement of staff.

- The fall in the level of outstanding business was the fastest in over two years and solid overall.

- New services orders contracted at the steepest pace for over two years, as companies highlighted greater client hesitancy in placing new work. At the same time, new business from abroad decreased at the second-fastest rate since December 2020.

- Service sector firms recorded a slower rise in employment during August. The level of outstanding business decreased at the quickest rate since May 2020, with reduced pressure on capacity resulting in the softest expansion in service sector workforce numbers in 2022 so far.

- Services firms noted that wage pressures, transportation surcharges and greater supplier costs had pushed up business expenses.

In an effort to encourage new sales, output charges rose at the softest pace in 17 months. Despite being robust in the context of the series history, firms stated that greater competition had led to the moderation in selling price inflation.

Trends in services are critical in the USA. This Goldman Sachs chart shows how fast the U.S. Services PMI has declined lately and is now the weakest of all DM economies.

Speaking of services: Restaurant Performance Index Declined1.3% in June

The RPI – a monthly composite index that tracks the health of the U.S. restaurant industry – stood at 101.3 in June, down 1.3% from May and the lowest level in 16 months.

While a majority of restaurant operators continued to report higher same-store sales compared to year-ago levels, customer traffic readings turned negative for the first time since February 2021. Looking ahead, restaurant operators’ outlook for sales growth and the economy continued to deteriorate. (…)

Only 31% of restaurant operators said their customer traffic rose between June 2021 and June 2022, down from 55% who reported similarly in May. Fifty percent of operators said their customer traffic declined in June, up from 31% who reported lower traffic in May.

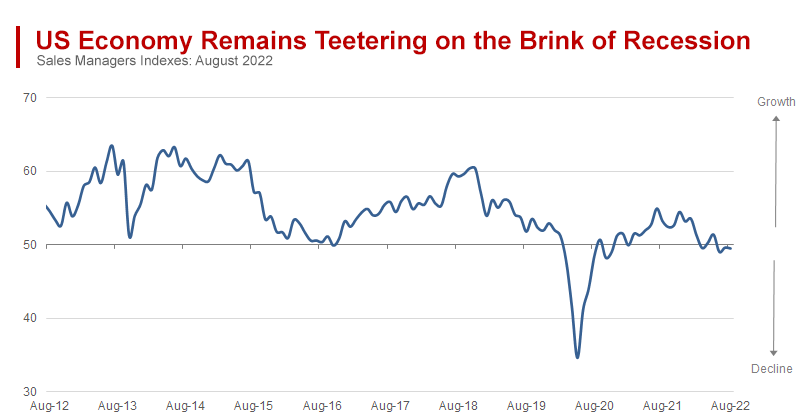

World Economics also released its Sales Managers Index measuring conditions even closer to the consumer than PMI surveys:

- Business Confidence remains firmly rooted to the 50 mark itself.

- The Sales Growth Index crept over the 50 level to arrive at 50.3.

- The Market Growth Index rose slightly to 51 to signal a little optimism.

- Overall staffing levels remained low compared with one year ago.

- The Sales Managers Index, summarising these trends, showed a marginal fall to 49.5, indicating very static market conditions in August, with almost no change on July.

- The Prices Index rose from 53.2 to 54.5 indicating the continuing presence of price inflation in markets generally.

From the Eurozone flash PMI survey:

- The overall drop in output was again driven by a contraction in the manufacturing sector, where production fell for the third month running and at a solid pace. That said, the service sector barely registered any improvement in activity during August as the rate of expansion slowed for the fourth consecutive month to the softest since the sector returned to growth in April 2021.

- New orders fell solidly for the second month running. New business was down in both the manufacturing and service sectors, with the former continuing to post the sharper contraction. The steep drop off in demand in the manufacturing sector has seen a build-up in unsold goods as firms have found it difficult to shift finished products. Post-production inventories increased at the sharpest pace in more than 25 years of data collection in August, with the rate of accumulation hitting a record high for the second month in a row.

- Input costs increased at the softest pace in close to a year, while output charge inflation was the weakest in the year-to-date. Softer inflationary pressures were recorded across both the manufacturing and service sectors.

- The rate of job creation eased for the third month in a row to the softest since March 2021.

- Declining output is now being seen across a range of sectors, from basic materials and autos firms through to tourism and real estate companies as economic weakness becomes more broad based in nature.

Note that the U.S. composite PMI has fallen precipitously in recent months and, at 45.0, is now much lower that the Eurozone’s 49.2.

From Japan flash PMI survey:

- Both manufacturing and services companies recorded a contraction in output in August, with the former falling at the fastest pace for 11 months.

- Of concern was the amount of new business received by private sector firms, which reduced for the first time in six months and pointed to further

weaknesses to come. - Average cost burdens faced by firms in the Japanese private sector rose markedly, yet at the softest rate since March. Concurrently, the increase in prices

charged for goods and services softened to a four-month low. However, firms often commented that weaker demand and economic headwinds were the main factor behind softening inflationary pressures.

Saudis, Allies Open Door to Oil-Output Cut to Keep Prices High Saudi energy minister’s comments, backed by some OPEC members, are a letdown for White House

(…) Saudi Arabia’s energy minister and some OPEC officials have suggested the alliance could extract fewer barrels of oil to stabilize a market buffeted by economic uncertainty, the risk of global recession and energy sanctions triggered by the war in Ukraine.

“OPEC+ has the commitment, the flexibility, and the means…to deal with such challenges and provide guidance including cutting production at any time and in different forms,” Saudi Energy Minister Prince Abdulaziz bin Salman said late Monday. (…)

Several OPEC members also told The Wall Street Journal on Tuesday that they might back a reduction in output, particularly if a global recession materializes. (…)

- Natural-Gas Prices Hit Shale-Era Highs Heating-season gas futures double last winter’s price; analysts see even higher prices ahead

(…) Normally this time of year, prices ease into the mild weather of autumn, encouraging producers and traders to store gas in underground caverns until winter, when demand and prices are usually at their highest.

This year, though, brisk exports, the electricity demand associated with some of the hottest and driest weather on record and sluggish production growth have kept U.S. natural-gas supplies from swelling into heating season.

The U.S. Energy Information Administration last week reported an unseasonably meager injection into storage facilities that enlarged to 12.7% the deficit to typical inventory levels for this time of year. (…) “There is potential for a winter U.S. superspike.” (…)

- Natural gas futures prices shot to a new record high in Europe, as Russia signaled that it will end supplies through its Nord Stream 1, pipeline at the end of the month, ostensibly for maintenance. (Axios)

Bison Interest says that “As the crisis intensifies, oil is increasingly being used to power factories and generate electricity, and oil will likely be an important source of heating fuel this coming winter.”

Macy’s Cuts Full-Year Earnings Outlook The company is the latest retailer to lower its guidance, citing risks of a steeper economic downturn and an industrywide inventory glut that will drive more markdowns.

(…) Same-store sales, or sales from stores that have been open at least a year, fell 1.5% from the previous year. (…) Macy’s reported that revenue was slightly lower in the second quarter compared with the same period last year, $5.6 billion from $5.65 billion.

Overall inventory levels remained elevated, the company said, but were down 7% from the first quarter. Macy’s said sales have been lower since Father’s Day as it and other retailers grappled with excess inventory and a pullback in consumers’ discretionary spending.

Macy’s customers across income tiers slowed their spending, Chief Executive Jeff Gennette told analysts on a call Tuesday. (…)

The retail chain said it is implementing markdowns across several categories, including seasonal goods, its private brands and activewear and sleepwear, as it looks to clear aging stock from its shelves. (…)

Macy’s trimmed its net sales forecast to between $24.34 billion and $24.58 billion, from a range of $24.46 billion to $24.7 billion. It now expects per-share earnings excluding one-time items between $4 and $4.20, compared with its prior forecast of between $4.53 and $4.95. (…)

Macy’s had raised its earnings guidance in May when it reported its first-quarter results, in part to reflect its improved expectations in its credit-card revenue. Executives said card balances are rising as customers grapple with high inflation.

“We’re just taking a measured view on bad debts for the remainder of the year—we’re monitoring credit delinquencies, we’re monitoring payment rates,” Macy’s finance chief, Adrian Mitchell, told analysts. “When we look at the industry more broadly, we see that inflation is outpacing wage growth, that’s just not sustainable for the consumer.”

-

Nordstrom Cut Outlooks as Shoppers Pull Back Retailers say they are looking to reduce inventory levels heading into the holidays.

(…) Nordstrom said it now expects adjusted earnings per share of between $2.30 to $2.60 for the year, down from a range of $3.20 to $3.50.

Nordstrom cited weakness among shoppers at its Nordstrom Rack discount chain, which targets lower-end consumers than its flagship stores. “The uncertainty moving forward is significant,” CEO Erik Nordstrom said on a call with analysts Tuesday. (…)

- Dick Johnson, CEO of Foot Locker, last week predicted a 320-330 basis point hit to its full-year margins due to discounting.

- U.S. New Home Sales Plunge as Prices Rise in July

Toll Brothers Inc., the largest US luxury-home builder, reported a plunge in quarterly orders and cut its sales outlook as rising interest rates challenge buyers, even at the high end of the market.

For the three months through July, signed purchase contracts tumbled 60% from a year earlier to 1,266, according to a statement Tuesday. Analysts were expecting 2,568, the average in a survey compiled by Bloomberg. The company said it expects to deliver 10,000 to 10,300 homes in its full fiscal year, down from a previous estimate of 11,000 to 11,500 homes. (…)

As the quarter progressed, “we saw a significant decline in demand as the combined impact of sharply rising mortgage rates, higher home prices, stock market volatility and macroeconomic uncertainty caused many prospective buyers to step to the sidelines,” Chief Executive Officer Douglas Yearley said in the statement. “However, in more recent weeks, we have seen signs of increased demand as sentiment is improving and buyers are returning to the market.” (…)

- Lower gas prices are making everyone feel a little better, Emily Peck writes for Axios Markets.

- A ‘Tsunami of Shutoffs’: 20 Million US Homes Are Behind on Energy Bills Surging electricity prices spur worst-ever crisis in late utility payments.

(…) about 1 in 6 American homes have fallen behind on their utility bills. It is, according to the National Energy Assistance Directors Association (Neada), the worst crisis the group has ever documented. Underpinning those numbers is a blistering surge in electricity prices, propelled by the soaring cost of natural gas. (…)

California’s PG&E Corp. has seen a more than 40% jump since February 2020 in the number of residential customers behind on payments. For New Jersey’s Public Service Enterprise Group, the total is up more than 30% for customers at least 90 days late—and that’s just since March.

The average price consumers pay for electricity surged 15% in July from a year earlier, the biggest 12-month increase in the data since 2006. A jump of that magnitude isn’t typical, and the gains are only poised to continue. Even in the free-market-oriented US, regulation of electricity rates makes it hard for providers to immediately pass on higher fuel costs, so the recent hikes may be just the start. (…)

Kashkari Says ‘Very Clear’ Fed Needs to Tighten Monetary Policy

“By many, many measures we are at maximum employment and we are at very high inflation. So this is a completely unbalanced situation, which means to me it’s very clear: We need to tighten monetary policy to bring things into balance,” he said Tuesday at a gathering of the Wharton Club of Minnesota in Minneapolis.

“When inflation is 8% or 9%, we run the risk of unanchoring inflation expectations and leading to very bad outcomes that would cause us to have to be very aggressive — Volcker-esque — to then re-anchor them,” he said,” referring to former Fed Chair Paul Volcker who tipped the US economy into recession to conquer inflation in the 1980s.

“We definitely want to avoid allowing that situation to develop. So with inflation this high, for me, I’m in the mode of we need to err on making sure we’re getting inflation down, and only relax when we see compelling evidence that inflation is well on its way back down to 2%,” he said, referring to the Fed’s inflation target. (…)

Kashkari, who prior to the pandemic was the Fed’s most outspoken dovish policy maker, has in recent months become its biggest hawk. (…)

Chinese Banks Cut Rates to Spur Economic Growth The one-year loan prime rate offered by banks was lowered to 3.65% from a previous rate of 3.7%, while the five-year rate was cut to 4.3% from 4.45%, the People’s Bank of China said Monday.

Sadly, and pitifully for such an important financial media, the WSJ omitted the most important part of the PBOC’s announcement. Bloomberg had it:

(…) Financial institutions, especially major state-owned banks, should increase loan issuance to the real economy, the PBOC said in a statement late Monday following a meeting chaired by Yi. Special loans worth 200 billion yuan ($29.3 billion) could be offered to property developers to help them complete housing projects that have already been sold, but which are yet to be finished. (…)

Defaults by property developers and an increase in stalled housing projects continue to plague the industry that once drove almost 40% of overall lending.

The result is that cheaper money and ample credit supply has failed to lead to stronger borrowing, increasing the risk of a “liquidity trap,” where lower interest rates aren’t able to spur more credit demand and economic growth. (…)

More to the point, the PBoC said that local banks should broadly increase lending activity, particularly towards the property sphere, and instructed state-owned lenders to guarantee onshore debt offerings from certain “high-quality” developers.

Clearly, Chinese authorities are experiencing what pushing on a string means. Hence the need to now offer lenders a backstop to boost confidence. But Almost Daily Grant’s adds this:

Analysts from CreditSights predict today that “state-backed bailout funds and policy loans are aimed at resuming unfinished projects, rather than aiding the developers in servicing their debt obligations; and bond guarantee funds are targeted at developers that are viewed as higher quality rather than those most in need of liquidity. In addition, the size of the bailout funds and the guarantee company is miniscule compared to the outstanding debt of the property sector.’

China’s Sales Managers Index remains very weak amid declining market demand:

Source: World Economics via The Daily Shot

Business confidence is holding although staff is being culled. This in turn is eroding consumer confidence, already shaken by the growing real estate crisis where some 70% of Chinese savings reportedly reside.

THE GOODS AND THE BAD

From BlackRock:

The pandemic and unique restart of economic activity brought about a massive re-allocation of resources. During the pandemic, consumer spending shifted to goods and away from services. That propped up goods producers’ earnings. That’s changing, in our view. Goods demand is weakening. Overstocked inventories, from retailers to semiconductor firms, are evidence of that. Meanwhile, spending is returning to services. This shift could hit stocks. Why? Earnings tied to goods are expected to make up 62% of S&P 500 profits this year, versus 38% tied to services. See the top bar of the chart.

In addition, the stock market isn’t the economy. Goods accounted for less than a third of the U.S. economy in the first half of this year. See the bottom bar. This means a boom in services doesn’t power S&P 500 earnings as much as it does the economy.

- Tightening of lending standards by commercial banks is pointing to a contraction in earnings (basically banks are taking precautions as recession risks loom).

Goldman Sachs; @patrick_saner via The Daily Shot

The average reservation wage, or the lowest pay level that Americans would be willing to accept for a new job, rose by 5.7% from a year earlier to $72,873 in July, according to the latest labor-market survey by the Federal Reserve Bank of New York, as soaring prices change the calculus for workers. (…)

The reservation wage reported by Americans with less than college degree, and those age 45 or younger, has risen by more than 23% since March 2020 when the pandemic began, according to the New York Fed. (…)

The new survey showed plenty of job-search activity, with 21.1% of respondents reporting that they received at least one job offer in the past four months, up from 18.7% a year earlier.

FYI, from FiveThirtyEight polls

Democrats currently have the lead in the race for the Senate. This is in part because in a few key races, Republicans have selected weak candidates, hurting their chances of taking the chamber in November. But as editor-in-chief Nate Silver writes, Republicans still have plenty of potential opportunities for pick-ups. The party’s best chance is currently in Georgia.

Things have improved for Democrats in the House — even though they are still underdogs. Following the Supreme’s Court decision to overturn Roe v. Wade, polls for the race for Congress have inched toward Democrats. The question now is whether that shift will last or if these polls shift back toward Republicans, as historically speaking, the party not in the White House does better in the midterms.

Amazing image via Axios!

This new image of Jupiter, which shows the planet’s famed Great Red Spot, its northern and southern auroras, and even its faint rings. Far-off galaxies are also visible to the planet’s left.

“We hadn’t really expected it to be this good, to be honest,” said planetary astronomer Imke de Pater in a statement. “It’s really remarkable that we can see details on Jupiter together with its rings, tiny satellites, and even galaxies in one image.”

The above image is the work of Judy Schmidt, a citizen scientist from California who processes deep space visuals for fun. Nice work, Judy!