SENTIMENT WATCH

Late Rally Lifts Stocks After S&P 500 Skims Bear Market

We just keep making history! Up and down.

(…) At one point, the S&P 500 slid so far it was on track to close at least 20% below its January peak—what would have been considered a bear market. A comeback in the final hour of the trading day pushed the index higher (…)

It has been decades since stocks have fallen for such a prolonged period. The Dow industrials notched their eighth straight weekly loss, their longest such streak since 1932, near the height of the Great Depression. The S&P 500 and Nasdaq had their seventh straight weekly loss, their longest such streak since 2001, after the dot-com bubble burst. (…)

This week, the pain spread well beyond the technology sector, alarming many investors. Major retailers reported their profits being hurt by rising costs and supply-chain disruptions, driving a selloff that led to Target and Walmart’s worst one-day decline since the Black Monday crash of 1987. As investors took stock of how inflationary pressures and slowing growth could weigh on corporate profits in the coming months, shares of everything from banks to real-estate investment trusts to grocery store chains fell, too. (…)

On Friday, even shares of energy companies, which have benefited from surging oil prices, fell alongside the broader market. (…)

Until the Fed convinces investors it can tighten monetary policy and reel in inflation without triggering a downturn, it is unlikely markets will stabilize, analysts said. The central bank’s job will be made more difficult by factors outside of its control that have added to inflationary pressures this year, including China’s zero-Covid policy and Russia’s invasion of Ukraine. (…)

The yield on the benchmark 10-year U.S. Treasury note fell to 2.785% Friday from 2.854% on Thursday. [And 3.12% on May 6] (…)

For the record: the S&P 500 fell all the way to 3,810 during Friday’s session, or roughly 20.6% below its record close of Jan. 3, then rebounded to cut the loss to 18.7%. The levels could be dismissed as trivial except for a nagging fact: history holds an improbably large number of examples of such rebounds lasting. In 1998, 2011 and 2018, the benchmark slid either below the 20% level or very near it on an intraday basis — only to reverse itself and never test the bear-market waters again.

Another fact to recall from those near-death experiences of the past: how bullish they ended up being. Consider the 19.4% drop from April 29 to Oct. 3, in 2011, for instance. At that bottom, the gauge experienced three days of gains greater than 1.5% — and continued on to its best month in 20 years. The recovery paved the way for the longest bull market ever recorded, the one that ended in the Covid crash.

Something similar happened in 1998, when the benchmark suffered a drop greater than 19%, bottoming on Oct. 8, before a 2.6% rally spared it from oblivion. From October’s start to the end of January the following year, the gauge surged nearly 25%.

In 2018, the bull market got within points of a 20% plunge on Dec. 24 before turning on a dime right after Christmas. Six days later began a year in which the S&P 500 surged 29% and the Nasdaq 100 rose 38%.

Julian Emanuel, chief equity and quantitative strategist at Evercore ISI, says 2018, 2011 and 1998 have been on his mind. “These three episodes notably occurred around periods of Fed tightening and did not accompany US recession,” he wrote in a note. His firm doesn’t predict a recession to happen this time, either.

And John Stoltzfus at Oppenheimer is reported saying:

I’ve been doing this for 39 years, and my gut is telling me right now this looks a lot like early 2009, before things straightened out. It looks like 1994. It looks like the fourth quarter of 2018. These things, if you projected negatively on that point, you missed the rally that followed after things were basically right-sized.

And today, the WSJ’s James Mackintosh also points out that “In the past 40 years, the S&P 500 has bottomed out with a 20%-or-so peak-to-trough decline four times, in 1990, 1998, 2011 and 2018.”

What the above commentators do not mention is that at the 1990, 1994, 2009, 2011, 2018 and 2020 bottoms, valuations were also at their lows, quite unlike presently:

P/E R20 P/E FOMC at low

- 1990: 13.0 18.4 easing

- 1994: 15.7 18.6 tightening

- 2009: 12.7 14.5 done easing

- 2011: 12.3 14.3 QE

- 2018: 14.6 16.8 stopped tightening

- 2020: 13.9 16.2 easing

- now: 18.1 24.0 tightening

James Mackintosh adds that

The common factor in the 20% drops was the Federal Reserve. Each time, the market bottomed out when the central bank eased monetary policy, with the stock market’s fall perhaps helping push the Fed to take the threats more seriously then it otherwise might.

That was exact in 1990 and 2020. But in other instances, the Fed was either tightening (1994), was done easing (2009 and 2011) or signaled it would stop tightening (Powell Pivot, Jan. 4, 2019). So far, Mr. Powell’s only apparent pivot is toward a Paul Volcker incarnation.

As to 1998, the Greenspan Fed decided to ease amid a strong economy, a 4.5% unemployment rate and stable 2-2.5% inflation, launching the second leg of the dot.com froth that Alan Greenspan himself labeled “irrational exuberance” in December 1996. But if you faded that rebound at 22+ P/Es, you could buy again 4 years later 15% cheaper.

I have been doing this for 50 years and I have learned that my gut is not always dependable. Objective risk/reward measurement has proven more rewarding, and less stressful.

I am often told that forward earnings would be more appropriate for P/E multiple calculation. I would only say that the Rule of 20 discipline is working very well with actual trailing earnings and also warn that, of the last 14 bear episodes, only 3 (21%) did not the precede a recession during the next year. These generally come with 10-15% earnings contractions, sometimes much more…

Quincy Krosby, chief equity strategist at LPL Financial, is totally right: “There’s zero certainty on where the economy is heading. You have a ‘recession’ camp, a ‘soft landing camp,’ and everything in between.”

But the world’s biggest hedge fund seems solidly camped:

- Bridgewater’s Greg Jensen Warns Markets Are Still ‘Overly Optimistic’ Investors have yet to adapt to a period of “secular change” that involves both higher inflation and slower growth.

(…) Jensen, who serves as co-CIO with Bridgewater founder Ray Dalio and Bob Prince, also warns that investors also shouldn’t expect the central bank to step in to save them. Instead the Fed will be hamstrung by its need to tighten financial conditions in order to bring inflation under control. This idea that the Federal Reserve is not afraid of a stock market selloff — and in fact may actually welcome one — has been expressed by the likes of former NY Fed President Bill Dudley in a Bloomberg Opinion piece from April.

“They want the asset prices to fall to a certain degree. And even if they fall more than they want them to, they’re weighing the inflation picture against that. So all of a sudden you’ve got a much bigger dip possibility before you get relief from policy makers,” Jensen said. “And in fact, the dip has to become disinflationary in order to do that.”

Jensen estimates that roughly 40% of the US equity market “can only survive essentially with new buyers entering the market because they’re not cashflow generating themselves. And that’s near a historic high, that’s like basically right in line with ‘99, 2000.” (…)

“The assets that need liquidity the most, that don’t themselves have cash flows are getting killed because liquidity is being withdrawn from the aggregate system and those assets that require kind of Ponzi-like ongoing purchases to support the assets, are getting hit the hardest,” he said.

That said,

- bearish sentiment is getting near its extreme highs as Ed Yardeni illustrates with Investors Intelligence data:

- volatility, a measure of fear, is also near extremes (via Ed Yardeni):

- this contrarian indicator is in buy low range…although it can get worse:

- deleveraging is well underway:

But we haven’t got the final capitulation yet:

- The Market Is Melting Down and People Are Feeling It. ‘My Stomach Is Churning All Day’ Many are watching the investments they meant for down payments, tuition or retirement shrink day after day.

“Watching”, but not selling out yet.

EARNINGS WATCH

Analysts must have been shaken by last week shocking revelation that inflation is hurting demand and boosting costs. The string of upside revisions has broken last week.

But it is a slow process among disbelievers. Q2 estimates are for EPS to rise 5.4%, down from 5.7% last week but Q3 and Q4 estimates are unchanged at 10.8% and 10.7% respectively.

Corporate guidance remains cautious but given that April seems to have been a particularly difficult month for revenues and margins, more negative surprises may be in store for Q2. Note that the N/P ratio totals 3.6 for Industrials and consumer centric companies.

BTW: Despite higher sales of small farm machinery during the three months ended May 1, Deere said its quarterly profit fell by 20% as its operating margin shrank by nearly 5 percentage points. Quarterly profit from large farm equipment rose 5% from a year earlier, but the profit margin contracted. Deere said it expects to continue raising prices on its equipment. Deere raised its net income forecast for this year by $300 million to a range of $7 billion to $7.4 billion. Deere’s shares fell 19% from $385 on Wednesday to $313 on Friday.

THE GOODS ECONOMY LESS GOOD

On May 15, the Chase consumer card spending tracker was 1.1% above its pre-COVID trend. That’s before adjusting for inflation. Actually, the tracker is 7.3% over its 2019 level. Total CPI since December 2019: +11.6%; CPI-Durable Goods: +22.1%; CPI-Nondurable Goods: +15.9%.

- End of April: Walmart and Target inventory jumped by 32% and 43%, respectively. Kohl’s was up 40%.

- Kodak now holds around six months of inventory, compared with three months before the supply-chain challenges began, Mr. Bullwinkle said. During the first quarter, the company reported $247 million in net inventory, up more than 12% from the prior-year period. (…)

- [Olaplex], The Santa Barbara, Calif.-based company went from having four to five months of supply in the first three months of 2021 to holding six to seven months of inventory by the end of last year’s third quarter. Inventory levels will remain elevated until supply-chain conditions show signs of improvement, according to Mr. Tiziani. (…)

- Other companies, including energy drinks maker Monster Beverage Corp. , microcontroller chip maker Microchip Technology Inc. and medical equipment company Steris PLC, also said they are carrying higher levels of inventory. (WSJ)

From April’s Senior Loan Officer Survey: “Among the most cited reasons for strengthening demand, major net shares of banks cited increased customer needs to finance inventory and accounts receivable, as well as higher customer investment in plant or equipment.”

Voluntary or involuntary accumulation?

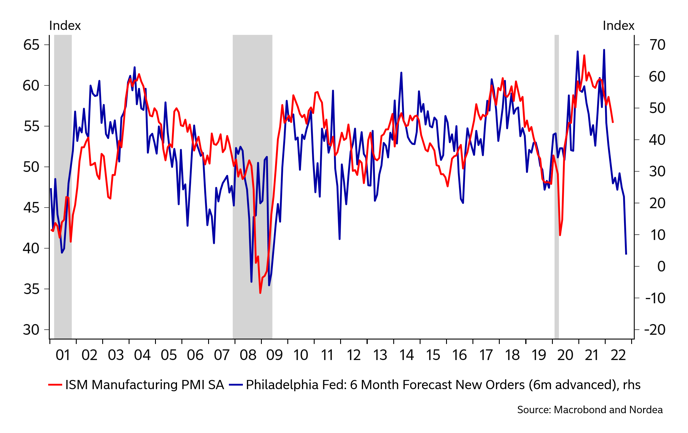

Bespoke finds much business pessimism in the Philly Fed’s latest survey, suggesting involuntary inventory accumulation:

Expectations indices meanwhile are generally more depressed with some readings even near record lows. As such, the average normalized distance between the current conditions and expectations categories throughout the report have broken out to the highest level since February 1988 and mid-1975 before that. Put differently, there have rarely been times in which the region’s manufacturers have reported such a dramatic difference between healthy current conditions while also holding a pessimistic outlook.

(Bespoke)

Meanwhile, we know that housing is facing strong headwinds:

(Bespoke)

The Loan Officer Survey revealed “weaker demand for all RRE loans over the first quarter.”

This is happening when the supply side of the equation is swelling:

(Bespoke)

- On Monday, the industry group representing Canada’s real estate agents said a key metric measuring the balance of power between buyers and sellers — the sales to new listings ratio — was about to tip from favoring sellers to an equal footing. Metropolitan Toronto is already a buyer’s market, Bank of Montreal research shows. Buyers no longer appear eager to purchase properties now to avoid increased prices in the future, the mindset that helped drive Canadian home values up by 50% since the start of the pandemic. (Bloomberg)

Hence:

FIBER: Industrial Commodity Prices Continue to Decline

Despite the recent improvement in U.S. factory output, many industrial commodity prices have weakened. The Industrial Materials Price Index from the Foundation for International Business and Economic Research (FIBER) eased 0.2% last week. It was the fourth consecutive weekly decline and pulled prices 7.1% below the peak in the second week of March.

Prices in the metals group have been under extreme pressure, tumbling 17.0% during the last four weeks. This decline was led by a 23.9% four-week decline in steel scrap prices. The price of zinc, which is used in batteries, fell 19.6% during the last four weeks while aluminum prices were down 13.9% in the last four weeks. Copper scrap prices fell 10.0% in the last four weeks, while tin and lead prices also fell sharply.

Prices in the miscellaneous group also have been under pressure and fell 1.0% last week (-10.0% y/y), led by a 5.6% decline in framing lumber prices. They have fallen by roughly one-half during the last year. Natural rubber prices eased 0.1% last week and have weakened 6.5% during the last four weeks.

Offsetting these weekly declines was a 4.3% increase in prices in the crude oil & benzene group, which have risen by one-quarter during the last year. Crude oil costs alone rose 6.4% last week and were up by roughly three-quarters y/y. The per barrel price of crude oil of $111.75 compared to the $115.64 per barrel high in the second week of March. The price of the petro-chemical benzene rose 10.2% last week and stood 10.8% higher y/y. Excluding crude oil, industrial commodity prices eased 0.5% last week and have fallen 7.3% during the last ten weeks.

Textile group prices recently have trended sideways, near thirty-year highs. Cotton prices increased 2.6% last week and rose 81.4% y/y. The cost of burlap, used for sacks, bags and gardening, eased 0.2% last week and remained near its record high.

Bloomberg: “Financial conditions have tightened at the fastest pace this far into a hiking cycle since at least 1987. The financial conditions index, as tracked by Goldman Sachs Group Inc., has fallen 1% since the first rate increase two months ago. The pace of tightening at this stage exceeds all previous five hiking cycles, data compiled by Bloomberg show.”

Germany Warns Falling Euro Could Push Inflation Even Higher The comments add pressure on the European Central Bank to reverse its negative rate policy despite concerns about a recession.

- Lagarde Signals That July Is Likely Liftoff Date for ECB Rates

- Bank of England’s Pill sees need for further interest rate rises

Business leaders warn that three-decade era of globalisation is ending

The world’s car buyers are ready to go electric

52% of respondents to EY’s annual Mobility Consumer Index who are looking to buy a car want an EV, according to the survey of 13,000 people in 18 countries.

- That’s a leap of 22 percentage points in two years, and the first time that EV interest exceeded 50%, the company said.

Consumer interest in electric vehicles has hit a global tipping point, with more than half of car buyers saying they want their next car to be an EV, new research from Ernst & Young shows.

- Yes, but: Americans still aren’t as enthusiastic as consumers in Europe and Asia.

Data: EY Mobility Consumer Index; Chart: Axios Visuals

- …. and EVs are shoving aside real volumes of oil

Electric vehicles displaced roughly 1.5 million barrels per day of oil last year, new analysis shows, an amount slated to grow as EV sales keep rising, Ben Geman writes in Axios Generate. (…)

- The amount EVs have displaced doubled over the last six years, BloombergNEF said.

Reproduced from BloombergNEF; Note: Includes a small number of fuel-cell vehicles; Chart: Axios Visuals

- “Two- and three-wheeled EVs accounted for 67% of the oil demand avoided in 2021,” the report notes, citing rapid adoption in Asia.

- Buses were next at 16%, followed by passenger vehicles at 13%, though BloombergNEF adds that they’re the fastest-growing segment.

BloombergNEF said last year’s displaced oil demand amounts to roughly one-fifth of Russia’s pre-invasion exports.

TECHNICALS WATCH

My favorite technical analysis firm’s most valued indicators still reflect an

unhealthy and still-deteriorating market

condition.

Biden Says U.S. Would Intervene Militarily if China Invaded Taiwan President Biden said the U.S. would get involved militarily to defend Taiwan if China tries to take it by force, issuing a stark warning to Beijing during his first trip to Asia as commander in chief.

![]() The White House rowed back the comments, saying he simply meant the US would give military equipment to Taiwan, not send troops to defend it. China was angry and warned him not to send the wrong message.

The White House rowed back the comments, saying he simply meant the US would give military equipment to Taiwan, not send troops to defend it. China was angry and warned him not to send the wrong message.

![]() Biden also said he’ll review Trump-era tariffs on Chinese imports.

Biden also said he’ll review Trump-era tariffs on Chinese imports.

Meaning review and cut.

(

(

{kind=link}