Greg Ip:

(…) AI disruption makes news almost daily. On Thursday, payments company Block said it was laying off 4,000 employees, 40% of its workforce, because AI has “changed what it means to build and run a company,” founder Jack Dorsey told shareholders. “Within the next year, I believe the majority of companies will reach the same conclusion.”

Is this just the beginning? No one should dismiss any scenario, even the most dystopian, with high conviction. Certainly not journalists, whose way of life is in AI’s crosshairs.

But I keep stumbling over one small problem with the doomsday vision: It requires a breakdown in how the market economy functions. Nothing like it has happened in the U.S. before, and there is no evidence it is happening now. (…)

The AI doomers claim this time is different. AI is happening faster and does far more than past technological revolutions. It could one day exceed human intelligence. (…)

If such a revolution were upon us, we should see some sign of it. We don’t, at least not yet. The ranks of software developers, widely assumed to be acutely vulnerable to AI, are up 5% in January from a year earlier, a pace largely consistent with the past 23 years. (…)

The number of computer programmers, who assist developers in ensuring code runs properly, was down slightly in the last year, in line with a secular decline in place for decades. Neither trend shifted much after ChatGPT’s arrival in late 2022. Competition from AI isn’t forcing computer scientists to take pay cuts, either. In 2024, the median young computer science graduate earned 63% more than the typical young graduate, up from 47% in 2009, data from Connor O’Brien at the Institute for Progress shows.

Meanwhile, business spending on software leapt 11% in the fourth quarter of last year from a year earlier, the fastest in nearly three years. Bessen sees this as evidence that software demand is elastic, meaning as the price per unit of performance falls, demand rises more.

This, Bessen notes, is in line with previous technological advances that drive prices down and demand up enough to offset direct job displacement. His examples include textile manufacturing in the 19th century, and the spread of ATMs in the 1980s.

My favorite example: As the number of bookkeepers shrank with the introduction of spreadsheet software in the early 1980s, the number of accountants and financial analysts newly empowered by Lotus 1-2-3 and Excel rose even more.

A study by Erik Brynjolfsson of Stanford University and two co-authors has found early signs of an AI impact: employment of 22- to 25-year-olds in the most AI-exposed occupations such as software developers and customer service agents fell 6% in the three years after the introduction of ChatGPT while that of older workers and workers in unexposed occupations rose.

But some critics say the drop could be explained by other factors, such as rising interest rates, that predate ChatGPT. Job postings for software developers jumped in the wake of the pandemic, then started to fall in early 2022, according to Indeed Hiring Lab.

Perhaps the advanced AI tools only now coming to market will change behavior in a way their predecessors didn’t. The doomsday scenario envisions businesses ditching legacy systems and consumers turning over many of their tasks to AI “agents” almost overnight.

In reality, businesses are risk-averse and consumers creatures of habit. Radiologists were supposed to lose their jobs to offshoring, and then to AI. They didn’t, because patients and providers like having humans around to explain their medical images. Since Google Translate launched in 2006, the number of human translator and interpreter employees in the U.S. has risen 73%.

Assume, though, that AI does destroy more jobs than it creates. Could the spillovers sink the entire economy? Almost certainly not. The money employers or consumers save as AI eliminates jobs doesn’t disappear; it gets spent on something else. This is why a sector can be in recession while the overall economy grows.

China’s entry into the World Trade Organization in 2001 cost the U.S. hundreds of thousands of manufacturing jobs in the following years. Oil and gas production jobs fell by a quarter after oil prices collapsed in 2014. And amid a spasm of bricks-and-mortar bankruptcies driven in part by e-commerce, retail employment fell by a quarter-million between 2017 and late 2019. In all three episodes, overall employment grew.

The real risk:

Imagine a recession starts for some other reason. Employers could respond with AI-driven job cuts they were contemplating anyway, deepening the downturn.

Another possibility: Tech investment gets ahead of demand, precipitating a bust. Tech workers lost jobs in droves after 2001, not because the internet had made them obsolete, but because the internet-stock bubble had burst.

Today, the sums being plowed into data centers far exceed the revenue AI is currently generating. A bust that brings down the economy isn’t my baseline. But at least it has a precedent, unlike the AI apocalypse that preoccupies folks now.

The other real risk, God forbids:

America’s Bills Will Come Due As the federal debt keeps ballooning, options are narrowing to avert a crisis.

The first law of holes: When you’re in one, stop digging. The Trump administration didn’t get this memo.

Despite America’s large and deepening budget deficit, President Trump has endorsed Defense Secretary Pete Hegseth’s request for a $500 billion increase in annual appropriations for the 2027 military budget. Administration officials are reportedly at odds about how to spend this money.

Led by Office of Management and Budget Director Russell Vought, the Trump administration may propose substantial cuts in domestic discretionary spending for fiscal 2027. It might seem like this would offset the increase in Pentagon spending, but the administration tried this same strategy in 2026 to little effect. Congress rejected most of the administration’s proposed reductions in domestic spending for fiscal 2026. (…)

There’s no reason to believe next year’s proposed cuts will fare any better. It would take significant domestic reductions to pay for an extra half-trillion in defense spending, but it’s clear neither party is willing to take the heat for domestic spending cuts of this size. Either Congress will reject Mr. Hegseth’s push to remake the Pentagon’s budget, or the federal budget deficit will increase.

The latter is unacceptable, because the fiscal status quo already is unacceptable. Earlier this month, the Congressional Budget Office issued its budget projections for the next decade. The federal deficit, pegged at $1.9 trillion for 2026, will rise to $3.1 trillion in 2036. The federal debt, which now stands at more than $30 trillion, will soar to $56 trillion—from 100% of gross domestic product to 120%. (…)

This year, interest payments on the federal debt will total more than $1 trillion, which is larger than the defense budget. Ten years from now, these payments will more than double, to a level close to discretionary spending for defense and domestic programs combined. By then, about two-thirds of federal borrowing will go toward interest payments. And it will only get worse after that.

The last time the U.S. had a balanced federal budget was 25 years ago. Since then, presidents and lawmakers of both parties have acted without regard for the country’s long-term fiscal health.

You might ask: So what? Deficit hawks have been predicting doom for decades, and it never happens. Why should the future be any different?

Because this can’t go on indefinitely. At some point, potential lenders to the U.S. will develop serious doubts about our capacity to repay what we borrow. They will demand higher interest rates to compensate them for the risk, triggering an economic slowdown that will reduce revenue, exacerbate the fiscal crisis, and create a vicious circle. We don’t know when this will happen, but economics and history tell us that it will. As the late economist and presidential adviser Herb Stein famously said, “If something cannot go on forever, it will stop.” (…)

(…) the path to fiscal responsibility must begin now, in the 2027 budget. To the extent that Congress and the administration can’t agree on spending cuts large enough to finance a large increase in defense spending, they should fill the gap with an across-the-board income surtax. They shouldn’t enact spending for defense—or any other item—that raises the budget deficit above the baseline. Nor should they enact new tax cuts that raise the deficit. This is what it means to stop digging.

Majorities of Americans don’t have much trust in AI and think companies are investing too much in it. Most Americans say AI will decrease the availability of jobs. More say it will have a negative effect on the economy than say it will have a positive effect. Most Americans have used artificial intelligence (AI), but only one-quarter use it regularly.

What you need to know about Americans’ views on artificial intelligence, as of the February 13 – 16, 2026 Economist / YouGov Poll.

A majority (58%) of Americans say they do not trust AI much or don’t trust it at all. About one-third (35%) trust it a fair amount or a great deal

Nearly two-thirds (63%) of Americans think AI will lead to a decrease in the number of jobs available in the U.S. Only 7% say it will increase the number of jobs and 12% say it will not affect jobs’ availability. These shares have not significantly changed since this question was asked in September 2025

A majority (54%) of Americans think companies are investing too much in AI. 22% of Americans say companies are investing the right amount and 4% think they are investing too little.

Did you miss Fear the Fear?

Who better to ask whether AI is killing the jobs market than our robot overlords themselves? In a week when AI doom-mongering has dominated headlines, the answer may surprise you. James Smith weighs up the evidence and explains why, for now at least, the drivers of employment look more traditional.

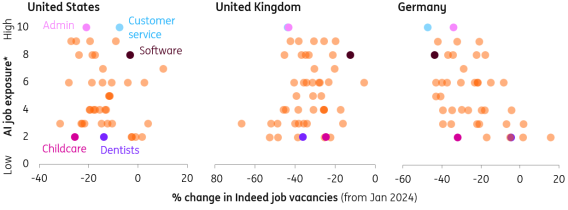

Here’s what I did: I took vacancy data from hiring agency Indeed, covering roughly 50 different sectors. Then I asked my trusty AI assistant/manager/grim reaper (delete as appropriate) to score them between one and 10 depending on how exposed the sector is to AI job losses.

It did a reasonable job at identifying its victims. Unsurprisingly, software was an 8/10. IT design/documentation was a nine, though surprisingly so was driving (can you tell AI lives in California?). Customer service is a solid 10/10. AI has clearly never had the pleasure of using the automated phone line of its utilities provider…

Still, it gives us something to play with. But when I then mapped these against the change in vacancies since the start of 2024, there couldn’t be less of a relationship. That’s true whether you look at the US, UK, France and largely Germany too (though squint carefully and there are hints of a trend line). And before you accuse me of cherry-picking the wrong time window, the results are basically the same whatever horizon you pick.

No obvious sign that AI-exposed sectors have seen vacancies drop faster

“AI exposure” based on asking an AI chatbot to rank each sector from one (not exposed to AI at all) to 10 (extremely exposed to AI job losses). Don’t take the results too literally…

Source: Macrobond/Indeed, ING

Obviously, this is a bit of simplistic Friday fun and definitely shouldn’t be used to justify a sell-off in the US stock market, unlike *ahem* certain other articles this week.

But it chimes with what the data is telling us more broadly. The Indeed data also shows a surprise spike in UK and US software vacancies over the past year, a time when broader job openings fell. Data from Challenger, a company that tracks job cut announcements, reckons that fewer than one in 10 layoffs since last April were down to AI. And even then, I wonder whether this is a convenient scapegoat masking more conventional motivations for reducing staff.

Strikingly, data monitored by the St Louis Fed shows that just 12% of American workers were using GenAI on a daily basis in their job, as of November, barely higher than a year earlier.

OK, so what about rising youth unemployment? US 18-24 joblessness is up more than a percentage point since early 2024 – and by three if you ignore a suspiciously large drop in January. It has reached new highs in the UK, too.

Tempting as it is to blame this on an AI-induced hiring drought among graduates, there is a simpler explanation. In both the US and Britain, the appetite to hire has fallen dramatically, even if there’s not much desire to fire, either. That is true across the vast majority of sectors. And in that environment, young people are always going to be disproportionately affected. That’s why the unemployment rate for those age groups tends to swing more wildly – up and down – than the national average.

Compounding those challenges in the UK, last year’s payroll tax and minimum wage hikes hit consumer services particularly hard – and those sectors tend to be more heavily represented by younger workers.

Wanted: Software engineers

Source: Macrobond, ING

The simple message here is that the drivers of the jobs market right now are more traditional. (…)

Now this:

AI and the Data Center Backlash

(…) “Many Americans are also concerned that energy demand from AI data centers could unfairly drive up their electric utility bills,” Mr. Trump said. “We’re telling the major tech companies that they have the obligation to provide for their own power needs.” This may soon become a political and business necessity.

A report this week by real-estate brokerage CBRE Group showed that data-center construction slowed late last year amid permitting headaches and delays connecting to the grid. Many states are threatening to impose restrictions on data centers unless they build their own power sources. (…)

Now something will have to give, but it needn’t be reliable power or America’s AI ambitions. (…)

The U.S. can’t afford to lose to China in the race for AI, and Americans shouldn’t have to pay for the cost of tech companies’ green virtue signaling.

Alas, the WSJ Editorial Board gives no clues how to solve this thorny dilemma other than suggest that hyperscalers need to deal with all the popular backlash, regulations, the shortages and the costs, including tariffs. During the midterms.

The FT’s Gillian Tett today reminds us that:

Jensen Huang, head of Nvidia, for example, told the FT last year that China could “win the AI race” with the US because its “power is free”. Elon Musk says that “based on current trends, China will far exceed the rest of the world in AI compute” because it will have three times America’s electricity output by late 2026.

And OpenAI has called for government action. “The US leads the world in developing AI [but] keeping that edge requires far more electricity than the US can currently provide,” it declared in a memo last year. “Electrons are the new oil.” (…)

It will be hard to shield voters from a looming energy squeeze, even if Trump does bully the tech companies into building their own generators. To cite one issue: since many data centres use diesel generators as a backup, “price increases of 20 to 50 per cent could be expected in the tight global diesel market” soon, according to Philip Verleger, an energy economist.

Another enormous problem is electricity transmission. China has raced to build high-voltage lines in recent years. But America has not. This cannot be fixed by the private sector or states without federal action because lines typically cross state borders.

However, there has hitherto been very little done — either by Democratic or Republican presidents. “In 2008, a new [transmission] project typically had to wait less than two years to get connected. But by 2024, it was over 4.5 years,” notes Heather Boushey, former economic adviser in the Biden White House.

Worse still, Trump is waging ideological war on renewable energy. Yes, China is using fossil fuels to expand its grid (including, lamentably, coal). But as Kyle Chan, an energy expert at Brookings, notes: “Over half of China’s [recent] electricity growth during [the last decade] has come from clean energy sources, such as wind, solar and hydropower.” These are fast and cheap to install — even before noting the climate change benefits.

But Trump’s “drill, baby, drill” mantra makes him reluctant to embrace renewables even as a complementary power source, let alone as a replacement for fossil fuels. Indeed last summer the energy department terminated a planned $4.9bn loan guarantee for an 800-mile “Grain Belt Express” power line intended to take wind power from Kansas to Illinois and Indiana. This is mad.

So can America close the gap with China? Some White House officials tell me it can, by using federal powers to install transmission lines and forcing Big Tech to pay for huge energy investments.

David Victor, a professor at UC San Diego, thinks more innovation will also help. “The really big [future] story in energy will be energy-saving innovation for the chips,” he says. “Many of the scenarios for rapacious energy growth for data centres are quite frothy [since] many of these projects will not be needed, especially if the AI bubble bursts.”

One hopes so. But unless — or until — this occurs, the saga will be yet more evidence of why joined-up, proactive, pragmatic policies can outperform a governance system plagued by polarisation and excess financialisation.

Future US historians may well weep. But right now, tech investors should ponder the grubby real-world problems of power — in both a political and literal sense.

US utilities generated a record amount of energy from renewable sources last year, even as the Trump administration implemented a range of policies to stymie green energy.

Some 1,162 terrawatt-hours of the country’s electricity was generated from renewable sources in 2025, a 10% increase over the prior year, according to federal data released this week. That represents 26% of all US electricity made — enough to power about 108 million US homes for a year. (…)

That stands in contrast to the Trump administration slashing incentives for wind and solar while gutting clean air regulations in a bid to help fossil fuels. The economics of renewables, though, have helped them generate a greater share of energy. (…)

“Even though there’s plenty of hurdles for renewables coming out of DC, we’re coming out of four years where there weren’t a lot of hurdles.” (…)

While it was a good year for renewables, the surge in energy demand from data centers, electric vehicles and industry also boosted power generated from fossil fuels. That includes a 13% increase in electricity generated from coal. The Trump administration has also supported fossil fuel production and use with grants and orders to delay plant closures. (…)

Even without subsidies, renewable installations are now cheaper to build than alternatives in most scenarios, according to Lazard.

That’s reflected in the pipeline for future US energy installations. Nearly 80% of the power plant capacity planned to be added over roughly the next decade is tied to renewable sources, according to filings with federal regulators and grid operators compiled by Cleanview.co, an energy data company.

Amanda Levin, director of policy analysis at the Natural Resources Defense Council, said the pace of green energy construction may actually accelerate as utilities race to beat deadlines for expiring federal incentives.

The government estimates that 93% of new generation capacity expected to be added to the grid this year will come from wind, solar and batteries. That sets renewables up to generate an increasingly large percentage of all US power. Wood Mackenzie expects renewables, including hydroelectric power, to account for nearly one in three US electrons by 2030.

“The only technologies to be deployed today at scale and at cost are wind, solar and battery storage,” Levin said. “No matter what Trump tries to do, he’s not going to see this resurgence of fossil fuels.”

Anthropic said it wouldn’t back down in a dispute with the Defense Department over artificial-intelligence guardrails, complicating efforts to reach a compromise ahead of a Friday deadline.

In a Tuesday meeting at the Pentagon, Defense Secretary Pete Hegseth gave Anthropic Chief Executive Dario Amodei until 5:01 p.m. Friday to agree to the military’s right to use the technology in all lawful cases. If Anthropic declines, Hegseth has threatened to invoke the Defense Production Act to make the company do what the military wants, or to designate the company a supply-chain risk, impairing its ability to work with other government contractors.

Anthropic has refused to accept the military’s proposal and doesn’t let users deploy its Claude models in scenarios involving mass domestic surveillance or autonomous weapons.

Amodei reiterated the company’s red lines in a public statement Thursday. “We cannot in good conscience accede to their request,” he said. The company said the military’s latest proposal would effectively undo those guardrails. (…)

Designating the company a supply-chain risk and invoking the Defense Production Act would be a nearly unprecedented escalation against a U.S. company, AI and security experts said. The threats “are inherently contradictory: one labels us a security risk; the other labels Claude as essential to national security,” Amodei said in his statement.

The threats have highlighted the Pentagon’s dependence on Anthropic. It was the only company with approval for use in classified settings before the Defense Department agreed to approve Elon Musk’s xAI, which agreed to the Pentagon’s use of its AI in all lawful scenarios.

Google and ChatGPT maker OpenAI are also used by the Pentagon in unclassified settings and talking to the Defense Department about potential approval for classified work.

An online petition began circulating late Thursday signed by employees of both companies asking them to take the same approach as Anthropic in negotiations with the Pentagon regarding autonomous weapons and mass surveillance.

As Market Financial Solutions Ltd. hurtled toward collapse in London, the setting was new, but the themes felt familiar.

Like US auto lender Tricolor Holdings, MFS was a nonbank finance firm looking to fill a gap that major banks had ignored or shunned, while tapping those Wall Street giants for the cash to do it. And like auto parts supplier First Brands Group, the banks took comfort in tangible collateral, only for accusations of double-pledging to rattle that assurance.

Even some of the names were the same: Banco Santander SA and Jefferies Financial Group Inc. — both stung by First Brands in recent months — are once again scrambling to recoup whatever money they can from an embattled company. This time, they’re alongside the likes of Apollo Global Management Inc.’s Atlas SP Partners, Barclays Plc, Wells Fargo & Co. and Castlelake LP. (…)

The saga risks becoming the latest multibillion-dollar collapse to saddle major banks with writedowns amid allegations of fraud. As MFS unraveled into a UK form of insolvency Wednesday, some entities within the firm claimed in court filings that they were seeing “serious irregularities” and a “significant shortfall” in their collateral. That contrasted with the company’s Saturday statement blaming an “impasse that has temporarily limited our access to everyday banking facilities.”

While the overall corporate default rate has remained stable despite economic and geopolitical concerns, credit markets have been spooked by a spate of so-called cockroaches, as JPMorgan Chase & Co. boss Jamie Dimon dubbed them last year. He followed that up with a warning this week that he’s starting to see parallels between today’s markets and the era before the 2008 financial crisis. (…)

Titans of finance have waged a war of words this week over the health of corporates more broadly, especially in the world of private credit where Blue Owl Capital Inc.’s decision to halt quarterly withdrawals from one of its retail funds rattled investors and sparked a selloff in the shares of asset managers. A business development company overseen by Apollo lowered its quarterly payout and wrote down its portfolio by about 3%.

Some of the biggest players in private credit, though, have argued that many of the high profile blowups of late involved lending by banks rather than private markets firms.

Others, however, see reasons for the market jitters: Marathon Asset Management Chairman Bruce Richards likened the dangers facing software firms — which have binged on tens of billions of dollars in debt in recent years even as artificial intelligence threatened to eat away large swaths of their business — to “a train coming down the tracks that you could see from some distance.”

“It wasn’t a matter of if, it was just a matter of when,” he said. “The markets have just woken up.”

(…) Investors fear that risks in the software sector, along with problems in private credit — a key funding source for technology firms — may upset the relative calm seen in public debt markets. Just last month, spreads hit multi-decade lows. Earlier this week, UBS Group AG credit strategists said private credit default rates could climb to as high as 15% if AI sparks an “aggressive” disruption among corporate borrowers. (…)

(…) KKR’s FSK fund oversees a $13bn portfolio, mostly of loans made to private-equity-backed midsized companies during a record wave of takeover activity over the past decade. (…)

Private equity firms are sitting on a growing $4tn logjam of unsold deals, according to consultancy Bain & Co, with many facing an unclear path to exit these holdings. Many of these companies have high levels of debt and some are falling into distress.

FSK’s portfolio was hit by large markdowns in the fourth quarter on debt extended to software companies. The fund’s holdings in debt tied to janitorial services groups, and so-called roll-ups of dental clinics, veterinarians groups and defence contractors also saw markdowns.

The vehicle said its net investment income fell to 48 cents a share in the fourth quarter, from 57 cents in the third quarter. (…)

Everyone Else Is Trading Without Us Tariffs have made the U.S. so unpredictable that our usual partners are looking elsewhere to make deals.

Economics 101 teaches that international trade is all about comparative advantage. People specialize in whatever they do best and trade for the rest, which results in everyone getting more of everything. While that theory is still true, it no longer guides global trade. Instead, what’s happening looks more like portfolio theory. Countries are no longer maneuvering to maximize gains. They’re diversifying to minimize losses. The risk they’re hedging against? The U.S.

While trade policy debates fixate on tariff rates and who pays, companies around the world are rerouting capital and effort to bypass the most unpredictable major economy on earth. Are tariffs here for the long haul or a fleeting fancy? Will exemptions be honored going forward? Business and political leaders around the world have to ponder these questions because a factory that takes years to build and pay for can’t be packed up and moved every time the White House discovers a new grievance.

Coercive diplomacy might produce the occasional headline-grabbing concession. But leverage decreases when partners have alternatives. India’s deal with Europe was a direct response to U.S. tariffs on India whipsawing from 26% to 50% and finally back to 18% in less than a year. Europe’s regulatory machine is slow and bureaucratic, but for long-term decisions, slow and predictable is preferable to fast and erratic. When Canadian Prime Minister Mark Carney refers to China as “more predictable” than the U.S., it’s a sign that something has gone deeply wrong with U.S. trade policy.

Domestically, the consensus is cracking. The House voted 219-211 to end tariffs on Canada, with six Republicans crossing the aisle. More than 60% of Americans disapprove of the tariffs. The Supreme Court ruled against the president’s use of emergency powers to justify tariffs, but the White House has been announcing new ones.

Adam Smith understood that protectionism creates perverse incentives. But even he might have underestimated its most expensive cost: the destruction of trust. A factory built in India’s state of Gujarat to serve European markets won’t relocate to Texas if the next administration softens on trade.

The world isn’t deglobalizing. It’s reglobalizing around partners who commit to rules rather than those who wield tariffs like a club. The long-term cost of these tariffs isn’t measured in revenue collected. It’s measured in partnerships formed without us and the rise of a trading system that no longer needs U.S. participation to function.

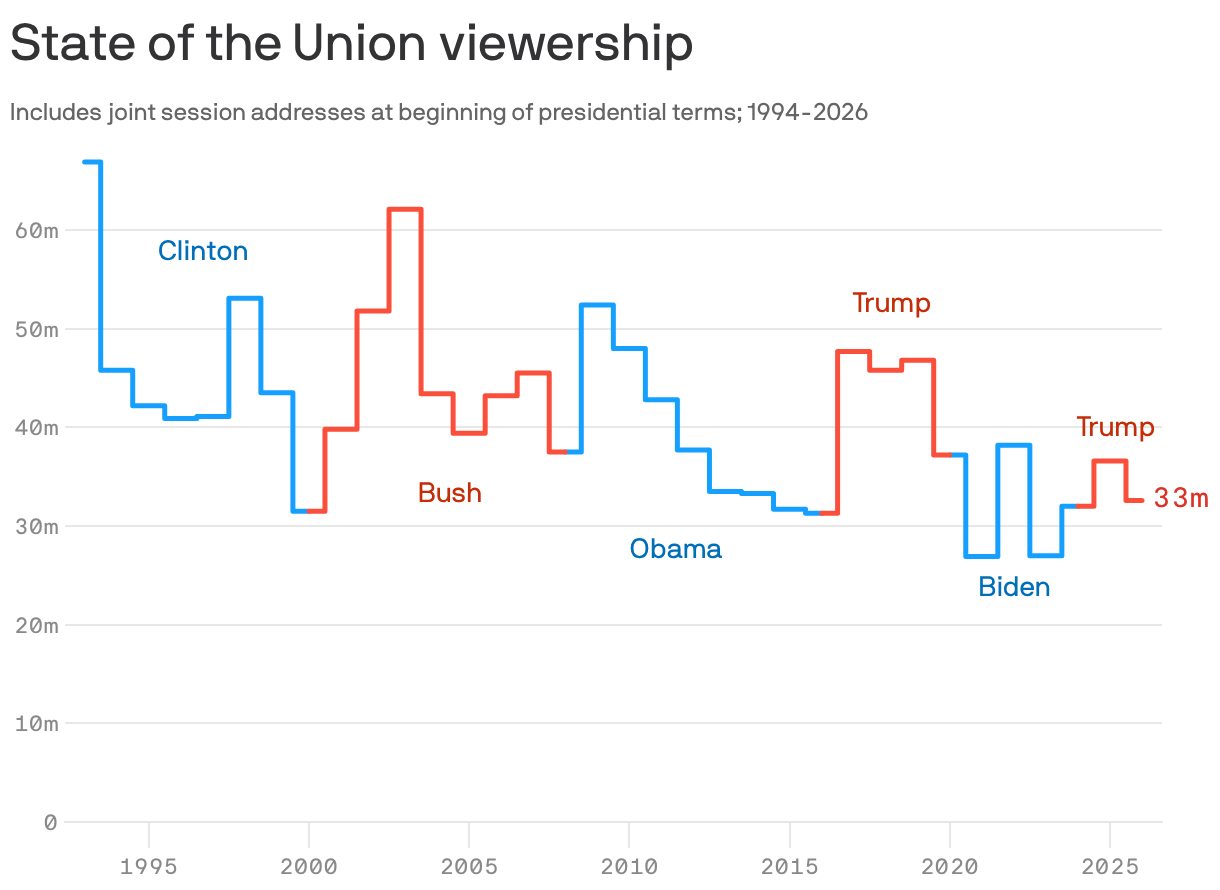

More than 32 million people watched President Trump’s State of the Union address Tuesday night, down from the roughly 36 million that tuned in to last year’s address to a joint session of Congress.

It’s also down significantly from the 45 million that tuned in to his address in 2018 during the second year of his first term.

Data: Nielsen. Chart: Sara Wise/Axios

The vast majority of those that did tune in on live television Tuesday (72%) were people over 55-years-old, per Nielsen.

Axios’ story does not say how many made it through the 108-minute long speech…

In aggregate, companies are reporting earnings that are 5.2% above estimates, which compares to a long-term (since 1994) average surprise factor of 4.4% and the average surprise factor over the prior four quarters of 7.6%.