US Companies Add Fewest Jobs Since Early 2021, New ADP Data Show

US companies increased headcount at a relatively sluggish pace in August, according to a revamped private report that suggests hiring is downshifting in an economy buffeted by high inflation and rising interest rates.

Businesses’ payrolls rose 132,000 this month, the smallest gain since the start of 2021, after a nearly 270,000 increase in July, according to newly compiled data from ADP Research Institute in collaboration with Stanford Digital Economy Lab. The latest report released Wednesday reflects updated methodology and includes historical jobs data on a monthly and weekly basis for the last 12 years. (…)

The figures, which are based on payroll transactions of more than 25 million US workers, offer a supplementary view of labor market conditions ahead of the government’s monthly jobs report. (…)

The government’s monthly jobs report Friday is anticipated to show US private payrolls climbing about 300,000 in August, according to the median estimate in a Bloomberg survey of economists. (…)

The report also includes fresh insights into wage growth. Those who changed jobs experienced a 16.1% pay increase from August 2021, more than twice the 7.6% gain for those who stayed at their job. (…)

Here’s the Atlanta Fed chart on switchers vs stayers:

![]()

- The ADP data under the new methodology show a strong correlation with BLS private payrolls over the full sample (+0.90 since 2010, mom sa), however, the relationship has broken down over the last year (correlation = -0.07).

- The ADP measure has also understated private payroll growth by 97k on average over the last year, including by 203k in July (+268k vs. +471k in the official measure). Accordingly, we view today’s report as an incrementally negative signal for August job growth but have left our forecast for nonfarm payrolls unchanged at +350k (mom sa). (Goldman Sachs)

Data: ADP and St. Louis Fed; Chart: Kavya Beheraj/Axios

MANUFACTURING PMIs

The eurozone manufacturing sector continued to contract midway through the third quarter. Output fell at a similar pace to that seen in July, which was the strongest since May 2020, while new orders declined sharply once again. Weak demand conditions were a major drag on goods producers in August, reflecting deteriorating purchasing power across Europe amid high inflation. Manufacturers subsequently cut their buying activity back further in response to the darkening economic outlook, although the reduced need for inputs helped lower the strain on suppliers.

Meanwhile, there were further signs of price pressures coming further down from their peak as rates of input cost and output charge inflation slowed to 19- and 16-month lows respectively.

The S&P Global Eurozone Manufacturing PMI® fell to 49.6 in August, down from 49.8 and further beneath the 50.0 mark that separates growth from contraction. Overall, this was the lowest reading since June 2020 and signalled a second successive deterioration in manufacturing operating conditions.

Of the monitored euro area countries, only three recorded Manufacturing PMIs in growth territory during August, although this masked declines in both output and new orders in each case.

Netherlands was the top performer, followed by Ireland, although both saw the rate of expansion slow to a 22-month low. The only other country to see a PMI above 50.0 was France. Elsewhere, sharper downturns were seen in Germany, Austria, Greece and Italy, with the latter seeing the strongest manufacturing downturn in August.

Eurozone manufacturing output fell, marking a third successive monthly decline. The reduction was solid overall and broadly similar to that seen in July, which was the quickest since May 2020. According to survey respondents, production volumes fell due to lower incoming new orders, although some continued to report material shortages. Demand for euro area goods fell sharply again in August and marked a fourth consecutive reduction. High prices, overstocked customers and reports of order postponements due to economic uncertainty were mentioned by manufacturers. New export sales* also fell, with the decline accelerating to the fastest since June 2020.

With production requirements falling, eurozone manufacturing firms reduced their input purchasing in August. The drop was of a similar strength to that seen in July (which was the fastest in just over two years). Amid falling input demand, the strain on suppliers continued to ease, as evidenced by the seasonally adjusted Suppliers’ Delivery Times Index rising for a fifth month in a row to its highest since October 2020. That said, vendor performance continued to worsen overall as transportation issues and shortages of certain materials persisted.

Manufacturing inventory levels rose further during August. In fact, despite lower production, stocks of finished goods increased at the fastest rate on record due to a lack of incoming new work. Meanwhile, pre-production inventories rose at one of the fastest rates since data collection began (in 1997) amid timelier input deliveries and lower output.

Latest survey data signalled a further cooling of inflationary pressures as both input cost and output prices rose at their softest rates in 19 and 16 months respectively. Nevertheless, both increases remained historically sharp overall.

Elsewhere, capacity pressures were reduced again in August, as signalled by a third straight fall in backlogs of work. The rate of depletion quickened and was the fastest in just over two years. Employment meanwhile rose, albeit to the weakest extent in a year-and-a-half.

Finally, business confidence edged up slightly from July’s 26-month low but it remained at a historically subdued level.

UK manufacturing downturn deepens as demand from domestic and overseas markets fall sharply

(…) August saw intakes of new work contract at the quickest pace for 27 months, amid reports of weaker inflows from both domestic and overseas markets. There was also mention of clients postponing, rescheduling or cancelling agreements in light of rising economic uncertainties, recession warnings and component shortages.

Foreign demand suffered its steepest retrenchment since May 2020, with order intakes from key markets such as the US, the EU and China all decreasing.

China: Power cuts weigh on manufacturing sector performance in August

China’s manufacturing sector saw a slight deterioration in overall business conditions during August, as power cuts and temporary factory closures weighed on output and sales. Production rose at the softest pace for three months, while intakes of new work fell for the first time since May. Subdued demand conditions led firms to cut back slightly on their purchasing activity and inventory levels, while workforce numbers fell modestly. Lower prices for some raw materials, notably metals and chemicals, led to the first fall in input costs since May 2020, which led firms to cut their output charges for the fourth month in a row.

The headline seasonally adjusted Purchasing Managers’ Index™ (PMI™) fell from 50.4 in July to 49.5 in August, to signal the first deterioration in operating conditions since May. That said, the rate of decline was only marginal.

Contributing to the sub-50.0 PMI reading was a renewed fall in total new business at Chinese manufacturers. Though only slight, it marked the first drop in sales for three months. Panellists commented that generally subdued market conditions, power cuts and lingering COVID -19 impacts had all dampened overall sales. Foreign demand also fell back into contraction, with new export business decreasing modestly.

Production growth meanwhile eased to a marginal pace that was the softest seen for three months. While there were reports that output was still recovering from pandemic-related disruption, power supply issues and temporary factory closures due to the recent heatwave had constrained overall growth.

Staffing levels at Chinese manufacturers fell for the fifth month in a row, as a number of firms mentioned company downsizing policies due to lower intakes of new work. The rate of job shedding eased from July, however, and was only modest. At the same time, backlogs of work were stable in August, following two months of decline. According to panel members, disruption to power supplies and production schedules had limited their ability to process and complete outstanding business.

Muted customer demand impacted buying activity, which fell for the first time in three months, albeit only slightly. At the same time, firms readjusted their inventory levels and registered mild drops in stocks of both post- and preproduction goods.

Vendor performance deteriorated for the second month in a row, albeit at a marginal rate. Power cuts at suppliers and lingering COVID-19 disruption were cited as key factors weighing on vendor capacity and lead times in August.

Average input costs fell for the first time since May 2020 during August. Though modest, the rate of reduction was the quickest seen since the start of 2016. Firms often stated that lower prices for some raw materials had helped to pull down expenses, with metals and chemicals mentioned in particular. Efforts to boost competitiveness and attract sales meant that savings were partially passed onto clients, with selling prices falling at the quickest rate since May.

Although Chinese manufacturing firms were generally confident that output would rise over the next year, the level of sentiment was unchanged from July and below the historical trend. Panellists stated that concerns over how long the pandemic will disrupt operations, a deteriorating global economic outlook and sluggish demand conditions all weighed on their projections for the year ahead.

Japan: Further falls in manufacturing output and new orders in August

The Japanese manufacturing sector registered a slower improvement in operating conditions midway through the third quarter of 2022, according to August data. However, the headline figure masked weaknesses in two key components that make up the reading, as both output and new orders fell for the second successive month. Moreover, the rates of decline quickened from July, with the contraction in new orders the sharpest recorded in nearly two years.

In a further sign that near-term activity will remain depressed, the level of outstanding business fell for the first time in one-and-a-half years amid the lack of incoming orders. That said, a benefit from weakened demand conditions was that pressure on supply chains eased, leading to the lowest instances of delivery delays since July 2021 and the softest rise in input prices since last December.

At 51.5 in August, the headline au Jibun Bank Japan Manufacturing Purchasing Managers’ Index™ (PMI) dipped from 52.1 in July, indicating a softer improvement in the health of the sector that was the joint-weakest since February 2021.

The lower reading of the headline index was partly the result of a sharper decrease in new orders. Sales fell for the second month running, and at the sharpest rate since October 2020. Firms commented that orders were dampened by a rise in COVID-19 cases, as well as weaker domestic and global economic conditions. Export orders also fell at a steeper rate that was the fastest for three months amid weaker demand across the Asia-Pacific region, most notably in China and South Korea. (…)

August data signalled that high raw material prices placed sustained pressure on average cost burdens at Japanese goods producers as input prices rose for the twenty-seventh month running. That said, the rate of inflation slowed from July and was the softest recorded since last December. In line with this trend the rate of output price inflation also eased, to a five-month low. Firms often commented that lower raw material costs, notably for oil, had been passed on to customers.

In response to weaker operating conditions, buying activity fell for the first time in 11 months midway through the third quarter amid production cutbacks at Japanese manufacturers. Firms also noted ongoing difficulties in sourcing and receiving inputs had softened slightly, as supplier delivery times lengthened to the smallest degree for just over a year. As a result of lower production requirements and sales, businesses chose to build inventories of both pre- and postproduction inventories.

Business confidence regarding activity over the coming year was unchanged from July in the latest survey period, meaning the overall degree of positive sentiment remained strong overall. Firms cited hopes that the end of global price and supply issues would encourage new product launches and boost output. However, there was growing concern about the strength of current demand.

- Taiwan, South Korea

ECB: We Now Expect a 75bp Hike in September and upgrade our forecast for the terminal rate to 1.75% in February 2023

Eurozone jobless rate falls to record low From 6.7 per cent in June to an all-time low of 6.6 per cent in July.

Lessons from the Past: Can the 1970s Help Inform the Future Path of Monetary Policy? A post that looks to the 1970s to draw some useful parallels between then and now.

This is the conclusion of the Atlanta Fed paper:

The fiscal response to the onset of the pandemic was quite forceful—$5 trillion by most counts—and at least on par with significant wartime spending. As these transfers and disbursements hit households’ wallets and businesses’ ledgers, money growth surged higher than 25 percent—peaking well above, though not as sustained as, the high money-growth periods during the 1970s. And we’ve seen a sharp surge in inflation that has gone well beyond pandemic-related supply constraints and shipping bottlenecks that affected certain production inputs such as computer chips. As of July 2022, roughly three-quarters of consumers’ market basket rose at rates in excess of 3 percent (and two-thirds of the market basket increased at rates north of 5 percent). These levels are on par with those we saw during the Great Inflation of the 1970s.

The Committee has begun an aggressive campaign to squelch this inflation threat, hiking rates in each of the last four meetings by a cumulative 2 percentage points along with implementing plans to reduce the size of the Federal Reserve’s balance sheet. It has also indicated that more policy tightening is to come. If history is any guide, at least in broad strokes, it will take some time before recent policy actions begin to affect inflation.

And here, it appears that the FOMC is very attuned to the lessons from the Great Inflation period. In a recent speech at Jackson Hole, Chair Powell noted, “Our monetary policy deliberations and decisions build on what we have learned about inflation dynamics both from the high and volatile inflation of the 1970s and 1980s, and from the low and stable inflation of the past quarter-century.” Perhaps more importantly, he emphasized, “Restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy.”

BTW, QT is really getting in high gear this month.

(The Market Ear)

(The Market Ear)

- Gavekal says that this could materially drain liquidity from U.S. financial markets.

For markets then, accelerated QT coming on top of further interest rate increases at a time when the US Treasury has finished reducing its cash balance will amplify the liquidity squeeze already under way. Moreover, US

commercial banks are tightening their lending standards, and so are unlikely to offset this liquidity drain. This is likely to weigh on US equity prices, and as real borrowing costs rise and choke off demand, it will increase the probability of a near-term US recession

Investors in the $23 trillion U.S. Treasury market are slicing up orders and switching to more easily traded issues, adapting to navigate periodic illiquidity that looks to get worse as the U.S. Federal Reserve reduces the size of its bond portfolio. (…)

The Treasuries market is the world’s largest bond market and serves as a global benchmark for a swathe of other asset classes, making its price gyrations especially worrying. (…) Piper Sandler estimated last month the market to be “the most illiquid it has been over the past 20 years, except of course for the Great Financial Crisis.” (…)

Some investors said mounting fears of a recession could convince the Fed to slow or stall quantitative tightening. If it keeps tightening, many see no immediate end to the liquidity problems. (…)

FED UP!

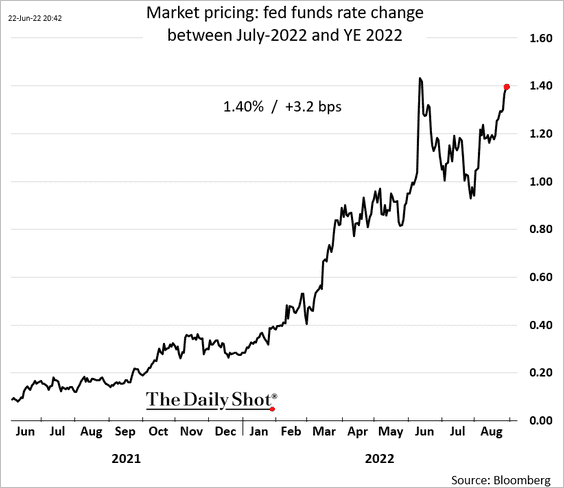

- The market now expects the Fed to increase rates by another 140 bps before the end of the year.

Fed’s Mester sees benchmark rate above 4% and no cuts at least through 2023

Fed’s Mester sees benchmark rate above 4% and no cuts at least through 2023- And yesterday we read that John Williams’ views are that FF rates of 4%+ are also most likely

Jeremy Grantham Warns ‘Super Bubble’ in Stocks Has Yet to Burst GMO’s co-founder says overvalued equities, bonds and housing will collide with high rates and inflation to cause more pain.

(…) Grantham predicted around the start of the year that benchmark stocks would plunge almost 50% in a historic collapse. (…) “You had a typical bear market rally the other day and people were saying, ‘Oh, it’s a new bull market,” Grantham said in an interview. “That is nonsense.” (…)

While rising inflation drove declines in the first half of the year, falling corporate profit margins will cause the next round of losses, he said.

“My bet is that we’re going to have a fairly tough time of it economically and financially before this is washed through the system,’’ Grantham said. “What I don’t know is: Does that get out of hand like it did in the ‘30s, is it pretty well contained as it was in 2000 or is it somewhere in the middle?”

HOUSING INFLATION

Our proprietary survey work suggests that a 6-7% mortgage rate is a particularly sensitive entry point for homebuyers, where most would downgrade or even completely abandon their search. We believe home ownership costs as a share of median income will average 34% until 2025, up from 25% in 4Q21.

As prospective buyers delay or abandon their home searches, there will be an increase in demand for both single family and multifamily rentals, placing upward pressure on rent growth, and further fueling the sticky inflation spiral. Existing lease data already suggests that rent growth should continue to accelerate through 2024. Incremental demand from abandoned home searches could drive rental rates even higher. (KKR)

China Locks Down Megacity Chengdu as Covid Zero Intensifies

U.S. officials order Nvidia to halt sales of top AI chips to China

Chip designer Nvidia Corp (NVDA.O) said on Wednesday that U.S. officials told it to stop exporting two top computing chips for artificial intelligence work to China, a move that could cripple Chinese firms’ ability to carry out advanced work like image recognition and hamper Nvidia’s business in the country.

The announcement signals a major escalation of the U.S. crackdown on China’s technological capabilities as tensions bubble over the fate of Taiwan, where chips for Nvidia and almost every other major chip firm are manufactured.

Nvidia shares fell 6.6% after hours. The company said the ban, which affects its A100 and H100 chips designed to speed up machine learning tasks, could interfere with completion of developing the H100, the flagship chip it announced this year.

Shares of rival Advanced Micro Devices Inc (AMD.O) fell 3.7% after hours. An AMD spokesman told Reuters it had received new license requirements that will stop its MI250 artificial intelligence chips from being exported to China but it believes its MI100 chips will not be affected. AMD said it does not believe the new rules will have a material impact on its business.

Nvidia said U.S. officials told it the new rule “will address the risk that products may be used in, or diverted to, a ‘military end use’ or ‘military end user’ in China.”

The U.S. Department of Commerce would not say what new criteria it has laid out for AI chips that can no longer be shipped to China but said it is reviewing its China-related policies and practices to “keep advanced technologies out of the wrong hands. (…)

SURVEY SAYS!

- Labor unions are the most popular they’ve been in about a half-century, according to a new Gallup poll, Axios’ Kate Marino writes. About 71% of Americans say they approve of unions, up from 64% pre-pandemic and a low point of 48% in 2009, Gallup found.

Americans 67 – 29 percent think the nation’s democracy is in danger of collapse. This is a 9-point increase from Quinnipiac University’s January 12, 2022 poll when it was 58 – 37 percent.

“In a rare moment of agreement, Americans coalesce around an ominous concern. Democracy, the bedrock of the nation, is in peril,”