U.S. Inflation Is Highest in 13 Years as Prices Surge 5% Consumer prices continued to rise rapidly in May as the economic recovery picked up, reflecting a surge in demand along with shortages of labor and materials.

(…) The core-price index, which excludes the often-volatile categories of food and energy, jumped 3.8% in May from the year before—the largest increase for that reading since June 1992.

Consumers are seeing higher prices for many of their purchases, particularly big-ticket items such as vehicles. Prices for used cars and trucks leapt 7.3% from the previous month, driving one-third of the rise in the overall index. The indexes for furniture, airline fares and apparel also rose sharply in May. (…)

Overall prices jumped at a 9.7% annualized rate over the three months ended in May. On a month-to-month basis, overall prices rose a seasonally adjusted 0.6% and core prices rose 0.7%. (…)

Compared with two years ago, overall prices rose a more muted 2.5% in May. (…)

“The inflation pressure we’re seeing is significant,” General Mills Inc. Chief Executive Jeff Harmening said at a recent investor conference. “It’s probably higher than we’ve seen in the last decade.”

He and his peers point to transportation, commodity and labor costs all increasing at the same time. They expect the trend to continue for at least the rest of this year. As a result, General Mills, Campbell Soup Co. , Unilever PLC, J.M. Smucker Co. and other big food companies are raising prices. Some increases are already visible on supermarket shelves, and more are coming this summer. (…)

Chipotle Mexican Grill Inc. recently raised its menu prices by roughly 4% across many markets to help cover the costs of wage increases as well as higher commodity prices, Jack Hartung, chief financial officer, said at an investor conference earlier this week.

Some 48% of small businesses indicated that they raised average selling prices in May, the highest share since 1981, according to a survey conducted by the National Federation of Independent Business, a trade association. (…)

More data and comments:

- The Cleveland Fed’s Median CPI rose 0.3% in May and is up at a 2.7% annualized rate in the last 4 months. The more restrictive 16% Trimmed-Mean CPI was up 0.4% for the second month in a row: +4.9% annualized, +3.7% over the last 4 months.

- The Atlanta Fed’s sticky-price consumer price index (CPI)—a weighted basket of items that change price relatively slowly—increased 4.5 percent (on an annualized basis) in May, following a 5.5 percent increase in April. On a year-over-year basis, the series is up 2.7 percent. On a core basis (excluding food and energy), the sticky-price index increased 4.3 percent (annualized) in May, and its 12-month percent change was 2.6 percent. The flexible cut of the CPI—a weighted basket of items that change price relatively frequently—increased 18.7 percent (annualized) in May, and is up 12.4 percent on a year-over-year basis.

")

But take the base effect out: 3-m annualized: Core-Sticky CPI: +4.6%; Core Flexible CPI: +33.7%:

")

-

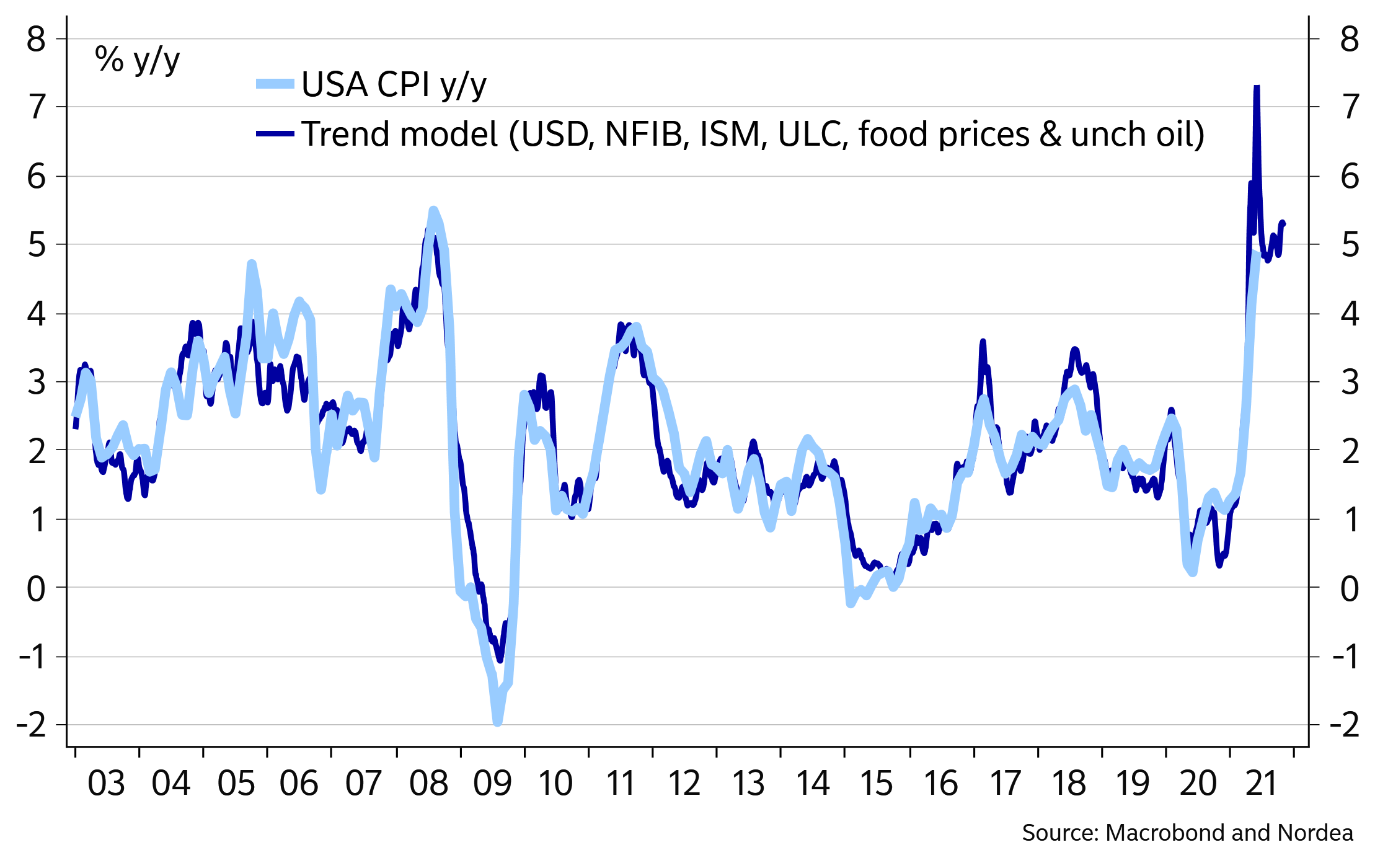

Another US CPI SHOCKER … or the market says not (Nordea)

As we have pointed to for quite some time, the upside risks to CPI remain for now and May CPI at 5.0% and core 3.8% were once again above economist consensus. But the whisper expectations were probably more in line and as long as the Fed doesn’t care, who does? Well, the market action in bonds clearly indicates that the bulk of investors that went short too late has to care. But what about inflation?

Used car prices increased an additional 7.2% m/m and there is probably more to come in June. Core CPI should surpass 4% y/y in June. We also continue to believe that the CPI effects from the combination of extremely low inventories and supply chain disruptions, and for that matter plenty of consumer money on the sideline, will be with us for longer than the consensus and the Fed seems to think.

US headline CPI y/y is about to peak but should stay at high level

That said, y/y CPI should drop back during July and August as base effects from oil prices and some other stuff drop out, which temporarily could make the transitory crowd cheer. It wouldn’t ease our inflation worries, however, since rents (with a 40% weight in core CPI) should take over as a primary driver in the autumn, probably pushing y/y core CPI to a new high in early 2022.

Rents should become the next CPI SHOCKER

Wouldn’t the Fed just simply also call the inventory and rent effects transitory as well? They could, but the Fed would then effectively have killed the CPI by rendering basically all components as “not being inflation”. We don’t think that is a particularly good idea and at some point the Fed should agree.

- Inflation Rate Climb Adds Impetus to Fed Policy Shift Central bankers are set to begin talking about easing bond purchases as soaring prices test patience

(…) “The intensity of the current inflation and the current bottlenecks in supply chains and labor markets is greater than I had anticipated,” said former Fed Vice Chairman Donald Kohn, adding that he still shares the central bank’s belief that the inflation pickup is temporary. “But it also could be that the underlying demand-supply balance will not correct as readily or as comfortably as the Fed and I had expected earlier. It’s got my inflation antenna quivering.” (…)

Julia Coronado, a former Fed economist and president of MacroPolicy Perspectives LLC, said she doesn’t think recent inflation data call for the Fed to change course.

“These price pressures are very narrowly focused on things that seem like they will be obviously transitory,” Ms. Coronado said. “Think about this: We are at the most intense moment. It will not get more intense than this. We are reopening. We are blasting stimulus into the economy with a fire hose. We’ve got monetary policy at maximum stimulation.”

Mark Carney, a veteran central banker who led the Bank of England from 2013 to 2020 and the Bank of Canada from 2008 to 2013, said he sees growing evidence that the tightness in the U.S. labor market and related price pressures could extend beyond the short term.

“The prospect of inflation being above target for longer than the makeup of the past undershoot—I think the balance of risks is headed in that direction at this stage,” Mr. Carney said in a Brookings Institution event Monday.

(…) On Thursday, when news broke that U.S. inflation climbed to 5% in May for the first time since 2008, yields on the key 10-year Treasury note moved in the opposite direction — falling to a three-month low of around 1.43%. And while bond-market gauges of expected inflation edged upward, they remained well short of this year’s high reached in May. (…)

In a report to clients after the May data came out, JPMorgan Chase & Co. economist Daniel Silver agreed that the drivers of higher inflation are still mostly temporary — but added that “there is some firming taking place away from these factors as well,” pointing in particular to increases in rents. (…)

Policy makers –- perhaps especially Vice Chairman Richard Clarida — are well aware that the bond market does not give a completely clear reading of expectations, even among investors. It can be muddied by trader positioning, liquidity and other issues. [including the Fed’s own manipulations].

- John Authers: What’s Scarier Than the Inflation Scare? Markets Investors are displaying extreme confidence in the Fed’s ability to keep prices under control.

(…) This chart from Dario Perkins of TS Lombard in London illustrates the extremity of the bond market nicely. It maps 10-year yields on the vertical scale, against core inflation. Usually, and unsurprisingly, higher inflation tends to mean higher bond yields. The current yield looks like a historic outlier. Arguably, bond yields have never been this tolerant of high inflation. As Perkins suggests in his title, bond markets are putting an awful lot of trust in central banks not to let inflation get going (which would damage longer-term bond returns):

- Much of it is extreme inflation in reopening sectors

- Commodity prices have already begun to turn over

- Wages are still well under control

- Cheap Dollars Attract Foreign Investors to Treasurys The cheapest dollars in years are spurring a rise in foreign investment in U.S. government bonds at the same time that pension funds are boosting their holdings—and that demand pickup could weigh on Treasury rates.

(…) There is a good case that these inflation numbers will reduce before long. I would summarize the three main supports as follows:

(…) Suffice it to say that both bond and stock markets look very confident, probably too confident, that they are right.

The WSJ Dollar Index, which measures the greenback against a basket of currencies, is down 2.9% this quarter so far and hovering close to the lowest level in about five months. The price of hedging dollars through forward rates also was the cheapest in at least six years last week and remains close by, according to analysis from Deutsche Bank. (…)

A 5-year debt sale on May 26 received the most bids from overseas investors since August at over 64%. A 7-year issuance in the same week saw the most since January. The latest data from the U.S. Treasury Department showed that major foreign investors upped their holdings of longer-maturity U.S. government bonds in March. (…)

Cash holdings have ballooned during Covid-19 lockdowns, with deposits at commercial banks in the U.S. sitting at a record $17.1 trillion, according to the Federal Reserve of St. Louis. Assets in money-market funds total $4.6 trillion, according to the Investment Company Institute, which is close to record levels. (…)

Forward rates, which are used to lock in an exchange rate at a certain point in the future and reduce the risk of currency fluctuations, are priced based on money-market rates and the difference between yields in the two currencies’ domestic short-term debt markets. The smaller the gap, the cheaper the trade—and that is just what has happened as the U.S. rates have come down.

“If you take a 10-year U.S. Treasury and you hedge with a three-month forward, the yield you get is around 0.9%,” said Althea Spinozzi, a fixed-income strategist at Saxo Bank.

That is higher than all European government bonds of the same maturity. Italy’s 10-year bond yield was 0.755% on Thursday. Japan’s equivalent bond yielded 0.659%. (…)

“We think the selloff in dollar rates will be slower and more gradual once we hit 2% for the 10-year. That is where we expect this to start kicking in, with flows from European and Japanese investors,” he said.

Another source of money flowing into Treasurys has been pension funds. Strong rallies in riskier assets, like stocks, in recent months helped to close the shortfall many funds have between the value of their assets and their liabilities, allowing them to move cash into safer assets, like bonds.

U.S. pension funds shifted nearly $90 billion of funds out of stocks and into fixed income during the first quarter of this year, $41 billion of which went into Treasurys, according to analysts at Bank of America. (…)

The Global Logistics Logjam Shifts to Shenzhen From Suez As Western economies roar back to life, a fresh wave of Covid-19 clusters in Asia—where vaccination campaigns remain in their early stages—is creating new bottlenecks in the global supply chain.

(…) Some ships have had to wait up to two weeks to take on cargo at Yantian, with roughly 160,000 containers waiting to be loaded, according to brokers. The price of shipping a 40-foot container to the West Coast of the U.S. has jumped to $6,341, according to the Freightos Baltic Index—up 63% since the start of the year and more than three times the price a year earlier.

Yantian handled nearly 50% more freight last year than the Port of Los Angeles—the busiest American container port—and in the first quarter of this year it saw container volume surge by 45% from a year earlier. Activity at the port, which handles more than 13 million containers a year, is now at 30% of normal levels and the delays could persist for several weeks, says Hua Joo Tan, a Singapore-based analyst at Liner Research Services.

Lars Mikael Jensen, head of network for A.P. Moller-Maersk A/S, the Danish shipping giant, said the backlog in Shenzhen would be felt globally, affecting goods sold at Walmart Inc. and Home Depot Inc., companies that have established logistics bases around the port. (…)

The blockage of the Suez Canal lasted a week and it took 10 days to clear the backlog, he said.

“Here there is no end in sight. The Chinese will keep everything closed until they are certain Covid won’t spread,” he said. (…)

At King Yuan Electronics Co. , one of [Taiwan]’s largest chip testing and packaging companies, more than 200 employees have tested positive for the virus this month, while another 2,000 workers have been placed in quarantine—cutting the company’s revenue this month by roughly a third.

Meanwhile, other semiconductor companies nearby have been grappling with their own workplace outbreaks, according to officials in Taiwan’s Miaoli county, where the recent clusters have been concentrated.

Taiwan Semiconductor Manufacturing Co. , which alone accounts for 92% of the output of the world’s most sophisticated chips, says it has not yet been impacted, but the outbreak is happening next door to its headquarters in Hsinchu, Taiwan. (…)

All told, the Malaysia Semiconductor Industry Association says the lockdown will reduce output by between 15% and 40%.

“It will disrupt the supply chain, somewhere, somehow,” said Wong Siew Hai, the group’s president. (…)

While shipping prices to the U.S. have surged, Mr. Zhu says most of his clients, including Amazon.com Inc. vendors and some American importers, are paying up.

“Last year, many clients delayed shipping in the hope that the cost could come down. But that’s no longer the case,” said Mr. Zhu. “Most do not seem to care about prices anymore.” (…)

Old Steel Plants Stay Idle Despite Surging Prices Two of the nation’s largest steelmakers are keeping older mills closed, passing up a chance to sell more metal at record prices, because of the high cost of restarting and the threats to their survival from rivals’ new plants.

(…) The new mills are still months or years away from operating, but steel demand received an unexpected boost last year from supercharged purchases of cars, appliances and machinery during the pandemic. Supply-chain problems have since drained inventories of steel. Wait times for some deliveries from U.S. producers have stretched up to six months, according to steel users. Some customers said they are receiving partial shipments.

“This is the hardest time in the history of our company to procure metal,” said Jonathan Ulbrich, vice president of Ulbrich Stainless Steels & Special Metals Inc., a stainless-steel processor and distributor in Connecticut that has been in business since the 1920s.

(…) assembling the workforce, raw materials and transportation needed to rehabilitate idled blast furnaces is too expensive.

“That capacity is not coming back, and people need to stop talking about that capacity,” he said. (…)

While the U.S. is the world’s most-expensive steel market, steel prices are high overseas at the moment too, discouraging buyers in the U.S. from pursuing imports. Spot-market prices for hot-rolled coiled steel in Southeast Asia are $900 a metric ton, and the cost of a shipping container has more than doubled since the start of the year.

Imports, which typically make up about a quarter of the finished steel consumed in the U.S. annually, last year accounted for 18%, the lowest share since 2003, according to the American Iron and Steel Institute. So far this year, imports have been running at about the same rate, the trade group said. U.S. tariffs, high prices and growing demand for steel in foreign markets are holding down import volumes. (…)

(…) Demand is so frenzied that U.S. mills have stopped taking orders from customers in recent weeks, according to Dan DeMare, director of sales at Heidtman Steel Products Inc. DeMare said the mills may not begin taking new orders until late summer so that they can clear backlogs.

In a global economy already shaken by supply shortages and inflation worries, the mills’ moves may signal more delivery snags and even higher prices for a commodity key to a wide swath of industries. Across the world, about 500 pounds of it is used per person each year, in everything from paper clips and automobiles to skyscrapers and toasters. (…)

Carl Harris, who has spent 36 years building homes, said he’s looking at two-month delays on refrigerators, ranges and dishwashers. Delivery times that are normally two to three weeks are now as much as half a year in many parts of the country, he said.

The lag means Harris can’t install the appliances package to market the two-bedroom empty-nester home in Newton, just outside Wichita, Kansas, even though the rest of the house is ready. He said other builders in the area are also having trouble getting plumbing fixtures, which have to be in place before a certificate of occupancy is issued. (…)

It’s also getting more expensive to drill in the shale patch as rising prices for steel, cement and other supplies and services lead to higher costs for explorers, according to Citigroup Inc. Steel prices for the drill pipe used in new wells could rise about 50% in 2021, Citigroup said.

Executives at Ford Motor Co. said on a first-quarter conference call that the company has seen commodity prices increase primarily for aluminum, steel and precious metals. It expects to see about a $2.5 billion increase in commodities from the second through fourth quarters, “so that’s going to hit us as we go through the rest of the year,” said John T. Lawler, Ford’s chief financial officer. (…)

U.S. steelmakers are expected to bring on about 4.6 million annual tons of production capacity by the end of 2022, an increase of about 4% from current levels. (…)

Oil demand to surpass pre-pandemic levels by end of 2022, says IEA Consumption expected to rebound by 5.4m barrels a day this year

(…) “In 2022 there is scope for the 24-member OPEC+ group, led by Saudi Arabia and Russia, to ramp up crude supply by 1.4 million barrels per day (bpd) above its July 2021-March 2022 target,” it said in its monthly oil report. (…)

Meeting the restored demand is “unlikely to be a problem”, the IEA said, forecasting that OPEC+ will still have 6.9 million bpd of effective spare capacity after July and that Iran’s talks with world powers could free its oil supply from U.S. sanctions.

“If sanctions on Iran are lifted, an additional 1.4 million bpd could be brought to market in relatively short order.” (…)

ECB to Keep Monetary Stimulus in Place Central bank upgraded its economic outlook for the eurozone

(…) The ECB said in a statement that it would keep its key interest rate at minus 0.5% and continue to buy eurozone debt under an emergency €1.85 trillion bond-buying program, equivalent to $2.2 trillion, through at least March 2022. It said it would buy those bonds at a “significantly higher pace” than during the first months of this year, repeating a pledge made in March. (…)

Ms. Lagarde said ECB officials had not yet discussed scaling down their bond purchases, saying such considerations were premature. In contrast, Federal Reserve officials have recently signaled they are getting ready to think about paring central bank stimulus at a policy meeting on June 15-16. (…)

The ECB said Thursday that it expects the eurozone economy to grow by 4.6% this year and 4.7% next year, compared with forecasts of 4% and 4.1% growth respectively in March. It expects inflation to reach 1.9% this year and 1.5% next year, up from earlier forecasts of 1.5% and 1.2% respectively.

Analysts said the ECB would likely need to shift course in the coming months and unveil plans to scale back its bond purchases to prevent the economy from overheating. That could happen after policy meetings in September or December, they said. (…)

Nordea also has a great comment on that:

- MC Easy Bee is starting to sound like a broken record

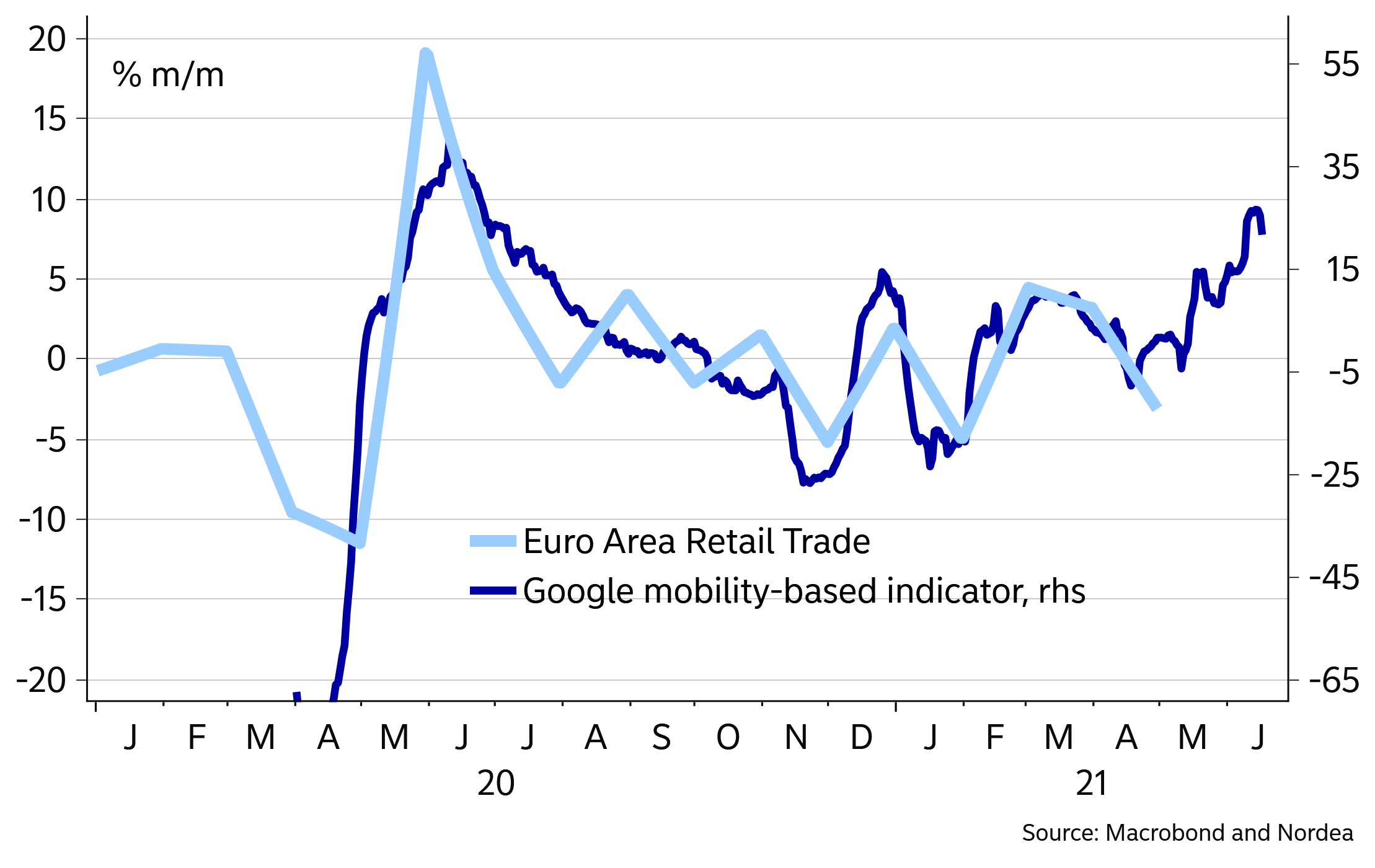

As widely expected, nothing new came out of MC Easy Bee this week. The press conference could be summed up as unsurprisingly dovish. No changes to the PEPP plans yet. The inflation forecast was nudged higher, but we still find it too low. When COVID-19 problems are mostly behind us this autumn, we think the language will change and that MC Easy Bee will become much more comfortable with higher long-end yields. The ECB hawks will be back with a vengeance in September.

There has been some soft data in early Q2, retail sales and German industrial production being examples. We wouldn’t worry about the data softness. Google mobility data has actually been a good guide to the short-term gyrations in hard Euro-area data and currently it points to strong growth in both May and June.

Trust us, the softness in retail sales is transitory

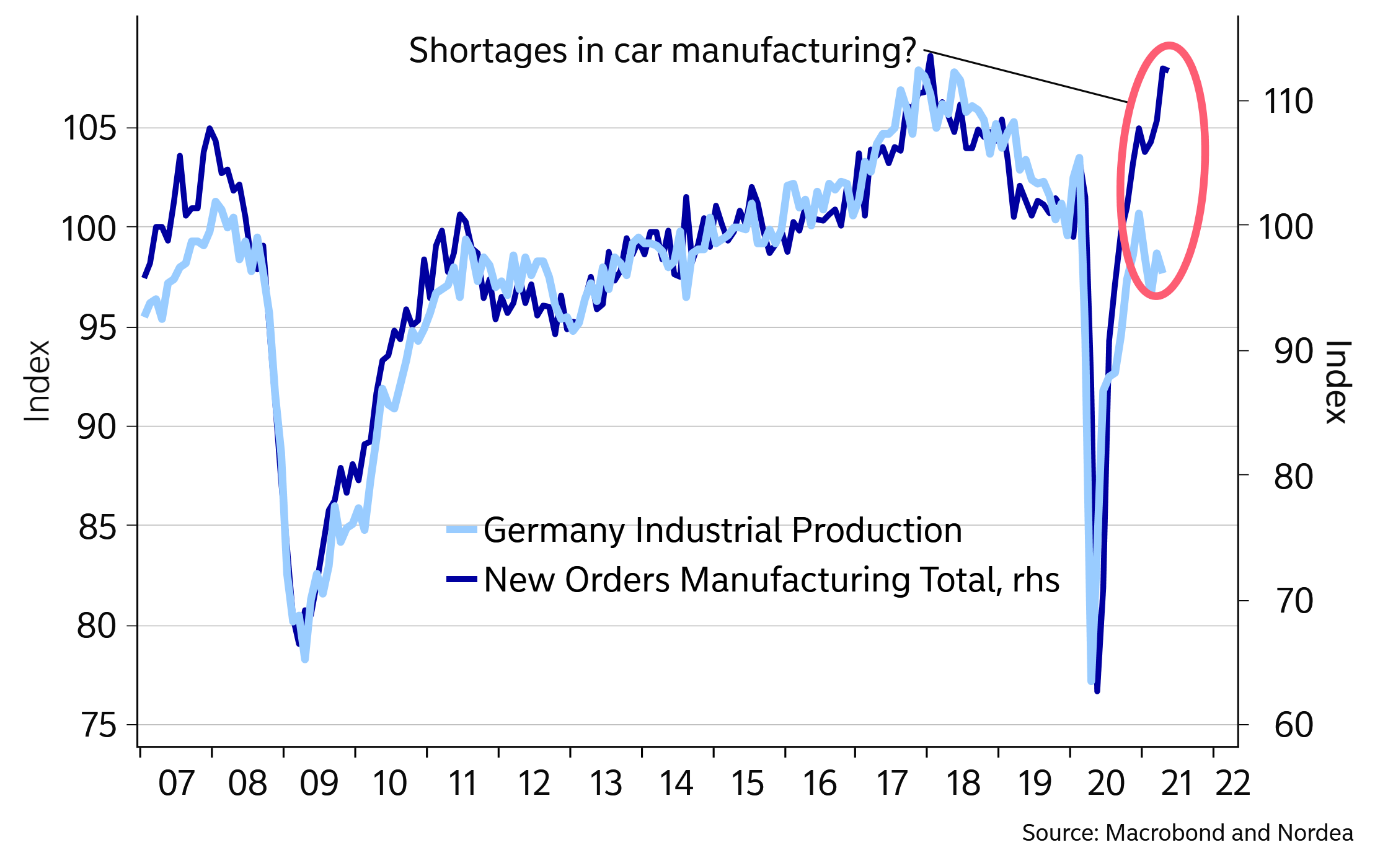

When it comes to the industrial production numbers, it’s obviously not a demand problem since orders have surged. It’s instead seemingly mostly related to the chip shortage weighing on German car production.

Chip shortages behind weak German industrial production

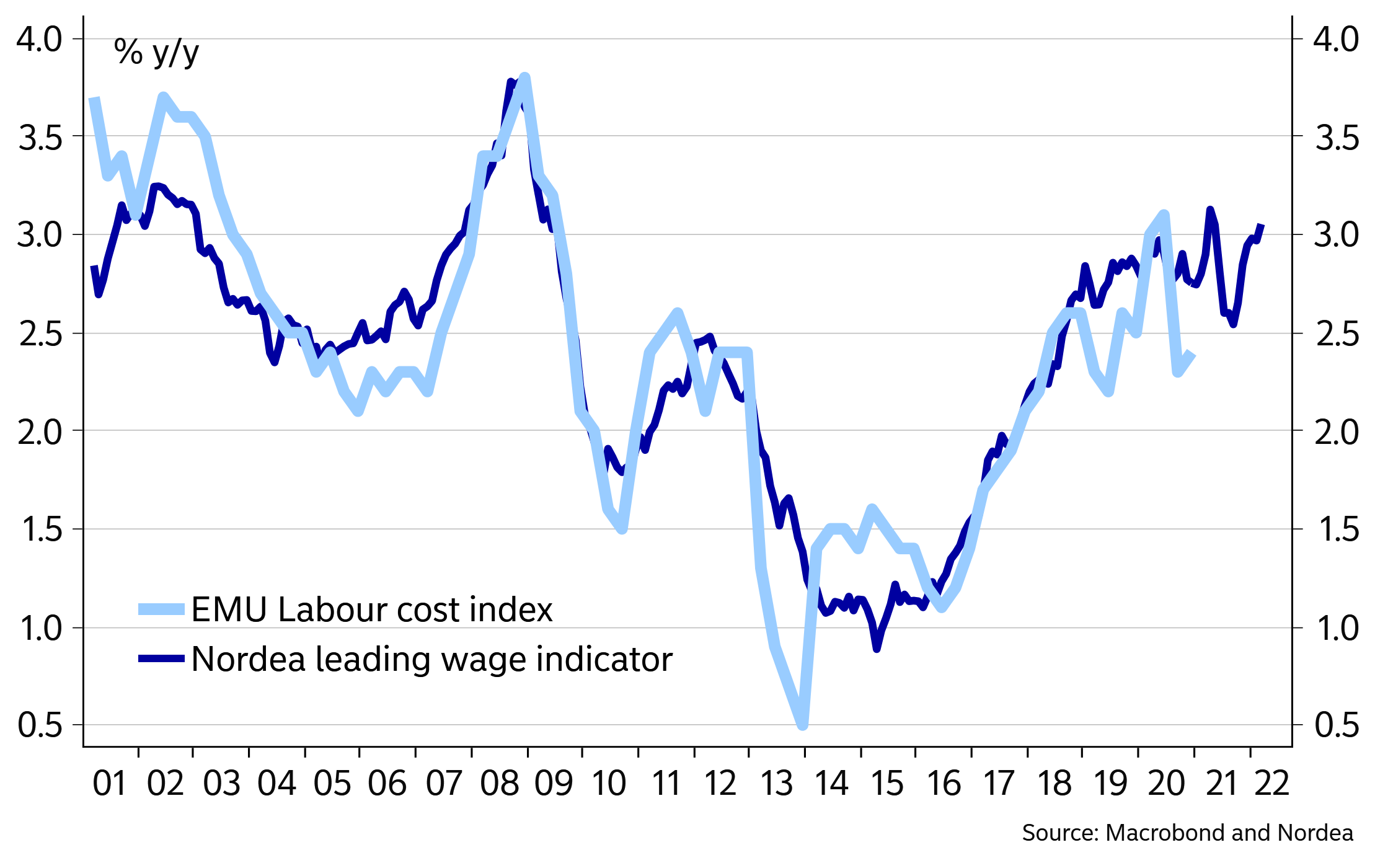

It is also so that the labour market is improving more rapidly than the ECB has feared. Labour shortages are increasing again. Already before the economies have opened up, our wage model for the Euro area is actually indicating a historically quite high wage growth in 2022. Even if it doesn’t sound so now, MC Easy Bee will soon dance to a more upbeat rhythm, and tapering of PEPP is still likely this year.

Euro-area wage pressures on the way up?

All in all, neither Jay-P nor MC Easy Bee are yet ready to abandon the crisis stance, so they are sitting in a tree K-I-S-S-I-N-G. Interestingly, however, it seems that there is a growing consensus amongst former central bankers that it’s time to act. Bank of England’s Haldane is the most recent example, warning about a “dangerous moment” for central banks and that it would be a “bad mistake” not to quell the inflation impulses. Hear, hear, Haldane!

Fewer Young Men Are in the Labor Force. More Are Living at Home

Are young men living at home because they’re not working? Or are they not working because they’re living at home? Hard to say, but either way, the trends are clear: More American males aged 25-34 are living in a parent’s home, and fewer are participating in the labor force. Here are the charts:

More Young Men Are Living at Home

(…) The Conference Board states unequivocally: “A growing percentage of young men without a bachelor’s degree [from 15% in 1995 to 25% this April] are living at home. This trend is contributing to a lower labor force participation.” (…)

“About half of prime age men who are not in the labor force may have a serious health condition that is a barrier to working,” the late Princeton economist Alan Krueger wrote in the Brookings Papers on Economic Activity in 2017.

Added Krueger: “Nearly half of prime age men who are not in the labor force take pain medication on any given day; and in nearly two-thirds of these cases, they take prescription pain medication.”

And yet, the 16-19Y cohort is back at work with a participation rate above its pre-pandemic level and substantially above its May 2019 level.

What Are the Odds? Even Experts Get Tripped Up by Probabilities People tend to rely on anecdotal evidence to make decisions, rather than considering the numbers

(…) According to the research of Ellen Peters, an expert in decision making at the University of Oregon and author of “Innumeracy in the Wild,” the lack of skill can have consequences for your wallet and your health. People who are less numerate adopt fewer healthy behaviors; they are 40% more likely to have a chronic disease; they end up in the hospital or emergency room more often; and they take 20% more prescription drugs, but are less able to follow complex health regimens.

Those who are good with numbers and confident in their ability fare better, Dr. Peters has found. And those who are bad with numbers but feel confident in their ability do the worst. (…)

Speaking of odds: