Divided Fed Inclined to Stand Pat Federal Reserve officials, lacking a strong consensus for action a week before their next policy meeting, are leaning toward waiting until late in the year before raising short-term interest rates.

(…) Fed governor Lael Brainard—who has been an outspoken voice in the camp of those who want to wait—called for “prudence” in raising rates in a speech in Chicago on Monday. (…)

Strong China data relieve pressure for stimulus

(…) Industrial production, a gauge of the crucial manufacturing sector, grew 6.3 per cent annually in August, the fastest pace since March. Retail sales growth accelerated to 10.2 per cent from 9.8 per cent in September, led by auto sales, which rose 13.1 per cent. (…)

-

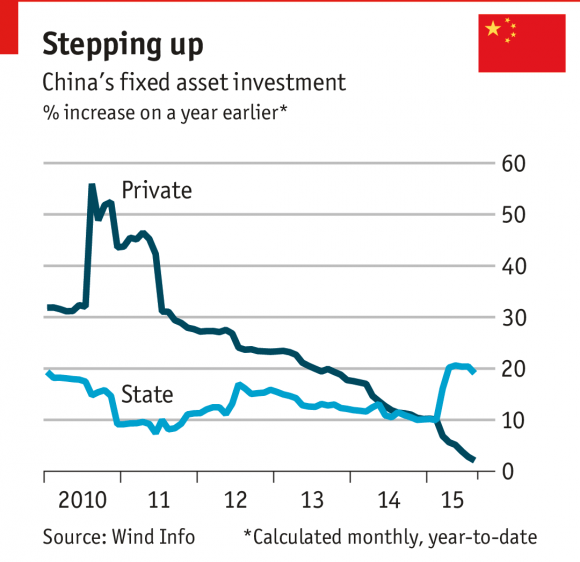

State at play: China’s economy

The government is playing an outsized role: state-led investment is up nearly 20% this year, while private investment is flat. It might seem unsurprising that the government is driving growth in China, but it marks a change. Previously, the private sector was much keener than the state on investing. The government is worried and is trying to spur businesses to spend cash; it has opened more infrastructure projects to them and promised financial support. Breaking up state-owned enterprises would be a bigger catalyst—but also a last resort. So long as growth holds up, don’t count on it. (The Economist)

Meanwhile, slowly but surely

The PBoC has been guiding the renminbi lower. (The Daily Shot)

IEA Cuts Global Oil Demand Forecast The International Energy Agency sharply cut its forecast for global oil demand for this year and the next amid what it called “wobbling” Asian demand.

(…) In its closely watched monthly report, the IEA, which advises oil-consuming countries on their energy policies, downgraded its global oil demand predictions by about 100,000 barrels a day for this year—still growing by 1.3 million barrels a day. It also reduced the forecasts by about 200,000 barrels a day in 2017, with consumption increasing more slowly at 1.2 million barrels a day.

“Recent pillars of demand growth—China and India—are wobbling,” the agency said. “After more than a year with oil hovering around $50 a barrel, the stimulus from cheaper fuel is fading.”

The IEA said that in China, ongoing economic slowdown and reports of heavy flooding dented industrial oil use and transport fuel demand. But it also cited a decline of oil demand in Europe as a factor. (…)

Since May, however, the IEA estimates that the U.S. had shut in 460,000 barrels a day of high-cost production, while the low-cost oil fields of Saudi Arabia have pumped out an extra 400,000 barrels a day.

The Paris-based agency said Saudi Arabia’s output fell by 50,000 barrels a day in August to 10.6 million barrels a day. By contrast, it said U.S. crude production stood at 8.7 million barrels a day in June.

Overall, OPEC’s crude output edged up by about 20,000 barrels a day to 33.47 million barrels a day in August as Middle-East producers kept their taps open to near record rates, according to the IEA. By contrast, OPEC itself says its production fell slightly last month.

Kuwait kept its output stable at 2.91 million barrels a day in August while the United Arab Emirates increased it by 20,000 barrels a day to 3.09 million barrels a day—their highest output ever.

The IEA said inventories in industrialised nations had “smashed through” the 3.1bn barrels mark reported in July to levels “never seen before”. The amount of crude processed by refiners is also growing at its lowest rate in a decade. (…)

The IEA had previously forecast the market to show no surplus in the latter half of this year and had expected a big stock drawdown in the third quarter. (…)

Europe’s Profit Warning

(…) Predictions of pan-European earnings rising 13 percent next year — the consensus view of analysts, according to Bloomberg — may end up being disappointed. If so, that’s another setback for Europe, where profit hasn’t recovered yet from the financial crisis. Earnings per share have fallen 40 percent over the last decade for European equities, versus a rise of more than 30 percent in the U.S.

It’s true that the commodity rout has stabilized and that emerging markets, a source of revenue for top European companies, have recovered. That’s why earnings upgrades in August outpaced downgrades for the first time in 15 months, according to UBS. But gambling that things can’t get any worse often proves a losing bet when it comes to the euro zone. Since 2011, consensus European earnings forecasts have been cut 7 to 15 percent every calendar year, according to UBS figures.

Meanwhile,

In the funding markets, the US LIBOR is grinding higher. (The Daily Shot)