Inflation Eased to 7.1% in November U.S. consumer prices rose last month at the slowest 12-month pace since December 2021, closing out a year in which inflation hit the highest level in four decades.

(…) down sharply from 7.7% in October. The pace built on a trend of moderating price increases since June’s 9.1% peak, but it remained well above the 2.1% average rate in the three years before the pandemic.

Core CPI, which excludes volatile energy and food prices, rose 6% in November from a year ago, easing from a 6.3% gain in October. September’s 6.6% increase was the biggest jump since August 1982. (…)

The CPI increased 0.1% in November from the prior month, compared with 0.4% in October. Core CPI rose 0.2% in November, down from 0.3% in October and 0.6% in August and September. (…)

November’s one-month gain in core CPI translates to 2.4% on an annualized basis. (…)

Used-car prices—a big driver of inflation last year—fell for the fifth straight month, slipping in November to their lowest level since September 2021. They are still up more than 40% from before the pandemic. Many travel-related prices declined in November as well, with airline fares down 3% from October, and car and truck rental prices dropping 2.4%. (…)

However, grocery prices picked up 0.5% in November from the prior month, accelerating slightly from October’s pace (…).

November’s CPI report offered possible signs wage pressures could be easing. Services price increases, excluding housing and health insurance, contributed less to core inflation in November compared with the prior two months. (…)

This WSJ positive narrative rightly reflects the main numbers in this CPI report. There are caveats, however:

- Declining core goods prices (-0.5% after -0.4%) was expected as supply chains normalize and demand slows amid high retail and wholesale inventories. Core goods prices are now up 3.7% YoY suggesting that retail sales are at best flat in real terms (Thanksgiving sales were reported up 3.5%). Most housing related goods are deflating. BTW, yesterday Amazon sent to my inbox 54 pages of “Very Merry Deals” claiming 20-65% off! Seems like a first for AMZN.

- Services inflation ex energy rose 0.4% MoM (+6.8% YoY), a 40-year high. Rent of primary residence showed no signs of slowing, jumping another 0.8% (+7.9%).

- Health insurance dropped 4.3% MoM, shaving 0.4% off monthly for the second consecutive month. Recall that the BLS has a peculiar way to measure these costs. This quirk is now understating this element.

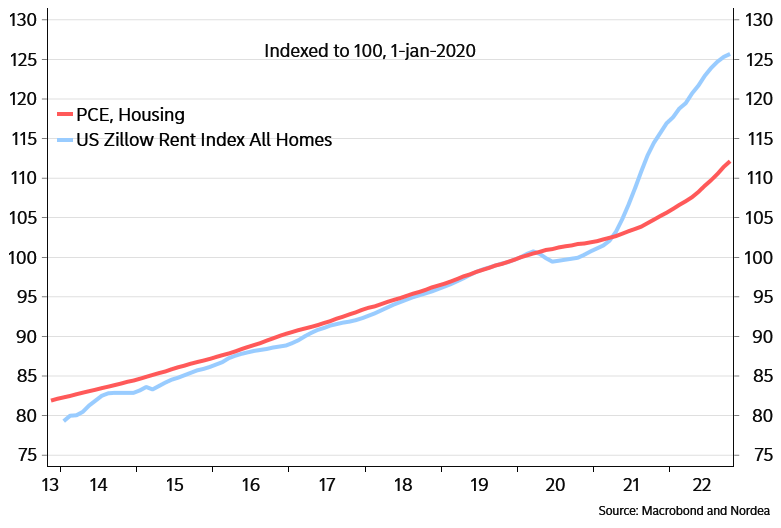

- This YoY chart is universally used to “prove” that rental costs are about to ease considerably under the weight of “new” leases (about 8% of all leases yearly).

But it’s not quite as simple. One, as Nordea says, “rental price growth have slowed down, but the impact of past increases will still continue to push the housing component in CPI and PCE higher for a long time given the way it is computed”.

The housing component in PCE has a lot to catch up before it is in line with new lease prices

Two, as explained in my recent rent rants (here, here and here), rental costs are much more correlated with wages which have yet to show signs of a meaningful slowdown

My guess is that the FOMC will focus on core services inflation, up 6.4% annualized in the last 4 months and 5.5% in the last 2, particularly after the surprise jump in wages in the last 2 months.

Maybe the FOMC doves will get Mr. Powell to focus on core-services ex-rent which he qualified as “may be the most important category for understanding the future evolution of core inflation” in his Nov. 30 Brookings speech as Bloomberg reports:

This spending category covers a wide range of services from health care and education to haircuts and hospitality. This is the largest of our three categories, constituting more than half of the core PCE index. (…)

Services prices excluding energy services and rents rose just 0.1% last month, after logging increases of 0.4% in October and 0.8% in September, according to Bloomberg calculations based on data published Tuesday by the Labor Department.

Mr. Powell would surely retort, as he has several times, that one month does not make a trend, and that the last 3-m trend of +5.3% is nowhere near comfortable.

From a consumer spending viewpoint, my CPI-Essentials series was up 0.35% in November after 0.84% and 0.4% in the previous two months. That is 6.5% a.r. and still +8.5% YoY, substantially above wage increases.

CPI-Essentials vs Wages

Deloitte CFO Survey:

- How do you regard the current and future status of the following economies?

- How do you regard U.S. equity markets valuations?

- Risk appetite: Is this a good time to be taking greater risks?

- Compared to three months ago, how do you feel now about the financial prospects for your company?

- Compared to the past 12 months, how do you expect key metrics to change over the next 12 months?

EARNINGS WATCH

Refinitiv looks at revisions:

Generally speaking, analyst estimates peaked in Q2 2022 and have since then have rapidly declined across all three indices. Russell 2000 has seen the largest decline year-to-date (-20.0%) in comparison to a -6.6% decline for the Russell 1000 and a -7.3% decline for the Russell 3000.

2023 EPS Estimate for Russell 1000/2000/3000

Exhibit 1 highlights the view amongst analysts that large-cap companies who typically have higher profitability, pricing power, margins, and scalability will be able to better navigate an uncertain 2023 riddled with recession worries than its smaller-cap counterparts. (…)

Exhibit 3 shows the 2023 EPS estimate in blue for all three regions and we can see that year-to-date, estimates have only declined in the S&P 500 (-5.9%) while actually increasing for the S&P/TSX (+4.7%) and STOXX 600 (+9.8%).

While this conforms to the market consensus view, if we strip out Energy, we see a vastly different picture which shows that estimates have declined significantly year-to-date for the S&P 500 and STOXX 600.

The S&P 500 has seen its 2023 EPS estimate ex. Energy decline 23.8% YTD, while the STOXX 600 has seen an even larger decline of 29.1% over the same period. The S&P/TSX has remained resilient, only declining 2.4%.

Exhibit 3: 2023 EPS Estimate for S&P 500, S&P/TSX & STOXX 600

CHIP WAR

US to Add More Than 30 Chinese Companies to Trade Blacklist The Biden administration plans to put more than 30 Chinese companies on a trade blacklist.

(…) Yangtze Memory, based in Wuhan, is the country’s largest 3D NAND semiconductor maker, producing memory chips that go into smartphones and other computing devices in competition with the likes of Samsung Electronics Co. (…)

US officials imposed the latest chip restrictions by explaining they are necessary to stop China from becoming more of an economic and military menace. The Biden administration wants to ensure the country’s chipmakers don’t secure the capability to make advanced semiconductors that would bolster China’s military.

China has sharply criticized the US moves, arguing that the American government is trying to stop its rise. This week, China filed a dispute with the World Trade Organization trying to overturn US-imposed trade controls, arguing they will disrupt global trade.

China readying $143 billion package for its chip firms in face of U.S. curbs

China readying $143 billion package for its chip firms in face of U.S. curbs

China is working on a more than 1 trillion yuan ($143 billion) support package for its semiconductor industry, three sources said, in a major step towards self sufficiency in chips and to counter U.S. moves aimed at slowing its technological advances.

Beijing plans to roll out what will be one of its biggest fiscal incentive packages, allocated over five years, mainly as subsidies and tax credits to bolster semiconductor production and research activities at home, said the sources. (…)

The plan could be implemented as soon as the first quarter of next year, said two of the sources who declined to be named as they were not authorised to speak to media.

The majority of the financial assistance would be used to subsidise the purchases of domestic semiconductor equipment by Chinese firms, mainly semiconductor fabrication plants, or fabs, they said.

Such companies would be entitled to a 20% subsidy on the cost of purchases, the three sources said. (…)

With the incentive package, Beijing aims to step up support for Chinese chip firms to build, expand or modernise domestic facilities for fabrication, assembly, packaging, and research and development, the sources said.

Beijing’s latest plan also includes preferential tax policies for the country’s semiconductor industry, they said. (…)

Xi’s call for China to “win the battle” in core technologies could signal an overhaul in Beijing’s approach to advancing its tech industry, with more state-led spending and intervention to counter U.S. pressures, analysts have said. (…)

This all out race to produce chips will not end well…

China Gives Up Counting All Covid Cases After Mass Tests End China will stop releasing comprehensive data on new Covid cases.

- China to Hold Meeting on Economic Targets Despite Covid

- Xi’s China-Arab summit success in Riyadh raises temperatures in Iran

Iranian President Ebrahim Raisi has “seriously demanded compensation” for his country over last week’s meetings between Arab leaders and Chinese President Xi Jinping in Riyadh.

In a meeting with Chinese Vice-Premier Hu Chunhua in Tehran on Tuesday, Raisi said some of the positions raised during Xi’s meetings with leaders from around the region “caused dissatisfaction and complaints of the nation and the government”.

The statement from the Iranian presidential office did not give details of what compensation may be sought. Nor did it refer to Friday’s declaration by China and the Gulf Cooperation Council (GCC), which is known to have angered Tehran.

- Vladimir Putin and Xi Jinping to hold talks on New Year’s Eve – Vedomosti (via @LiveSquawk)

Binance withdrawals hit $1.9 bln in 24 hours, data firm says

(…) Binance in a November blog post shared details of digital-asset wallet addresses with tokens worth about $69 billion.

Last week, the exchange released a proof of reserves report. The document, based on a snapshot review by accounting firm Mazars, showed the exchange having sufficient crypto assets to balance its total platform liabilities.

The report also acknowledged limitations as it didn’t amount to a full financial audit that would give a clearer picture of Binance’s overall health.

“We are working collaboratively with Mazars to share all relevant financial information with them so that they can verify the accuracy of all the data we have shared as well as our process for extracting the data,” the spokesperson said. “We are working on getting the next update for additional tokens published as soon as possible.” (…)

Frankly, I would not care to know that they have “sufficient crypto assets to balance its total platform liabilities”. I would want to know if they have enough liquid dollar assets to meet redemptions. Their “as soon as possible” is very worrisome…

BTW: ““We allege that Sam Bankman-Fried built a house of cards on a foundation of deception while telling investors that it was one of the safest buildings in crypto” (SEC Chair Gary Gensler in a statement yesterday.)