Weekly Unemployment Claims Down 12K, Lower Than Expected

In the week ending July 8, the advance figure for seasonally adjusted initial claims was 237,000, a decrease of 12,000 from the previous week’s revised level. The previous week’s level was revised up by 1,000 from 248,000 to 249,000. The 4-week moving average was 246,750, a decrease of 6,750 from the previous week’s revised average. The previous week’s average was revised up by 250 from 253,250 to 253,500.

The dashed line below is where claims were pre-pandemic:

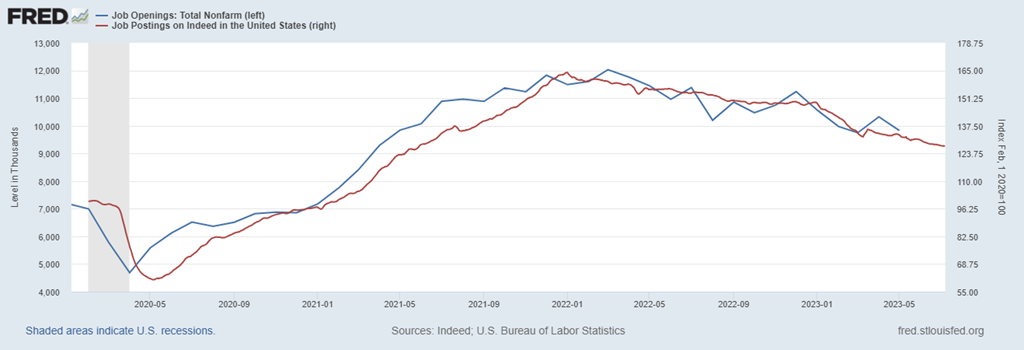

Job openings are slowly declining but remain well above 2019 levels:

Producer Price Index: June Headline Cools to 0.1%, Lowest Since August 2020

The Producer Price Index for final demand increased 0.1 percent in June, seasonally adjusted, the U.S. Bureau of Labor Statistics reported today. Final demand prices declined 0.4 percent in May and edged up 0.1 percent in April. (See table A.) On an unadjusted basis, the index for final demand advanced 0.1 percent for the 12 months ended in June.

In June, the increase in final demand prices can be traced to a 0.2-percent rise in the index for final demand services. Prices for final demand goods were unchanged.

The index for final demand less foods, energy, and trade services moved up 0.1 percent in June after no change in May. For the 12 months ended in June, prices for final demand less foods, energy, and trade services advanced 2.6 percent.

The YoY chart looks really good with PPI-Goods deflating 4.1% and PPI-Services slowing to 2.2%.

But the base effect is masking the reality that producer prices actually remain 16–22% above 2019 levels, not really deflating:

![]() Matt Klein (The Overshoot) makes the surprising observation that

Matt Klein (The Overshoot) makes the surprising observation that

Despite accounting for a small share of the overall CPI, movements in the price index for “full service meals and snacks” tend to track the broader price index remarkably well. (…) Dining out is a discretionary purchase that is sensitive to economic conditions, while the input costs are a mix of local rents, taxes, and wages, as well as equipment and groceries.

CPI-Food-away-from-home has perfectly matched total CPI between 1953 and 2008. That’s 55 years!

After the GFC, restaurant prices rose consistently faster than total CPI, partly because of food and energy costs but mainly because of rising wages (black).

Looked at on a YoY basis, the recent decline in total CPI (now +3.1%) has not been matched by restaurant prices (+7.7%). There were similar dislocations in 2015, in 2019 and in 2020 and they were all closed by total CPI eventually reaching up to CPI-Food-away-from-home.

On a MoM basis, restaurant prices are still rising in the 5% range:

However surprising and upsetting, a 99.9% correlation over 55 years cannot be simply dismissed, can it?

Maybe we can stop watching used car prices, airline fares and rent…

BTW:

Wage Growth Tracker Was 5.6 Percent in June

The Atlanta Fed’s Wage Growth Tracker was 5.6 percent in June, down from the 6.0 percent reading in May. For people who changed jobs, the Tracker in June was 6.1 percent, down from 6.8 percent in May. For those not changing jobs, the Tracker was 5.5 percent, compared to the 5.8 percent reading in May.

Recession Watch: realistic optimism

(…) Recent data suggest that, on balance, the global economy remains resilient to higher rates, while the direction of travel seems consistent with a steady slowdown in the macroeconomic cycle, albeit without encountering a global recession that many, including Fathom, expected — at least not this year. (…)

The resilience in investment growth has a parallel with that of consumption, where excess savings accumulated during the pandemic have helped cushion consumers from the higher cost of living that has subsequently ensued. In 2020 and 2021, US corporates boosted their coffers bringing forward borrowing intentions, as highlighted by a large spike in corporate bond issuance. The current issuance levels are likely weaker than the trend, though not by much and the UK in Q1 2023 posted the strongest quarter in corporate issuance since the pandemic. This suggests, again, that the economy remains resilient and it is still going through a process of unwinding some of the pandemic dynamics.

Healthy levels of investment and issuance, often overlooked, are also important indicators of market liquidity as signals of credit expansion and willingness to take risks. Investors tend to overly focus on shifts in central bank balance sheets and rate decisions, while forgetting about changes in these private sources of liquidity. If central bank actions were all that mattered liquidity would be a countercyclical indicator. However, liquidity as gauged by the Fathom liquidity indicator (FLiq) is, like investment, strongly procyclical and currently signalling a rebound. (…)

{kind=link}

It’s never a good time to have a recession but this time would be particularly bad. Federal interest payments are up 70% from 2019 eating 1% more of the U.S. GDP pie.

(CBO)

(CBO)

Individuals have been smart fixing their mortgage rate at the lows:

This shows the surge in the percent of loans under 3%, and also under 4%, starting in early 2020 as mortgage rates declined sharply during the pandemic. Currently 23.3% of loans are under 3%, 61.3% are under 4%, and 81.2% are under 5%. (CalculatedRisk)