Market Stress Snarls Trading in U.S. Treasurys Making deals now is as hard as in early days of Covid-19, traders say

The markets for the world’s safest and most liquid assets, the government bonds issued by the U.S. and other rich countries, came under immense stress on Wednesday following a week of worries about the health of global banks.

Liquidity, the capacity to trade quickly at quoted prices, has fallen sharply in two of the keystone markets, those for U.S. Treasurys and German bunds, traders said. Difficulties including wider price spreads and slower executions are now spreading to many other markets, they said, including those for derivatives that firms and traders use to lock in prices and hedge risks weeks and months ahead of time, such as options, futures and swaps. (…)

Trading was frenetic. Trading volumes in the Treasury market Wednesday appeared to be about twice typical levels, said Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets.

But the spreads quoted in markets for Treasurys and derivatives tied to other government bonds, reflecting the gap between quoted prices to buy and sell, were far wider on Wednesday than they were last week, traders said, typically a sign of market anxiety.

The ICE BofA Move Index, a measure of volatility in the bond market, rose to the highest levels in at least three years, surpassing levels recorded during the March 2020 market crash.

The ease of buying and selling Treasurys makes them the bedrock of Wall Street trading, used to park money or as collateral on loans. When the market breaks down, the resulting turmoil can rapidly spread to other assets, hitting everything from stocks to currencies—as well as, eventually, the rates for mortgages and other loans.

Investors generally agreed that fear of economic distress was driving down interest-rate expectations and pushing investors to dump riskier assets in favor of safer ones, following the U.S. bank and Credit Suisse routs. (…)

One driver of the unruly trading: the significant change over the past week in the outlooks for global growth and inflation, reflecting concerns that the U.S. bank mess and trouble in Europe might signal a sharp slowdown ahead. (…)

“Markets operate on greed and fear,” Mr. Bass said. “Fear is overriding greed right now.” (…)

Some traders said that the market moves were some of the wildest they had seen in their careers. Government bond prices have logged swings not recorded in decades, when Paul Volcker was chairman of the Federal Reserve. (…)

Quantitative investment strategies also helped fuel the price swings.

After enjoying a record-breaking year betting bond prices would fall, algorithmic money managers that ride market trends are racing to close out their short positions, or purchasing securities previously borrowed and sold in a bid to benefit from falling prices.

Computer-driven funds such as commodity trading advisers, or CTAs, took large bearish positions in the Treasury market in recent weeks, according to Société Générale SA. Then bonds rallied and yields dropped, wrong-footing some traders and adding to the price swings. (…)

Monetary Tightening and U.S. Bank Fragility in 2023: Mark-to-Market Losses and Uninsured Depositor Runs?

This March 13 paper (post SVB) is from 4 researchers at USC, Northwestern, Columbia and Stanford universities.

The short of it is that the U.S. banking system is “a lot more fragile than commonly assumed”:

Even if only half of uninsured depositors decide to withdraw, almost 190 banks are at a potential risk of impairment to insured depositors, with potentially $300 billion of insured deposits at risk. If uninsured deposit withdrawals cause even small fire sales, substantially more banks are at risk. Overall, these calculations suggest that recent declines in bank asset values very significantly increased the fragility of the US banking system to uninsured depositor runs.

Post the GFC, the Fed’s QE policies brought real long-term rates substantially below normal, often driving them below zero. Its narrative of “lower-for-longer” and “transitory inflation” in 2021 convinced many investors that the Fed was in control and that bonds were relatively safe investments even if earning little in real terms.

Demand for bonds exploded in 2021 and nobody should be surprised that most financial institutions yearned for yields.

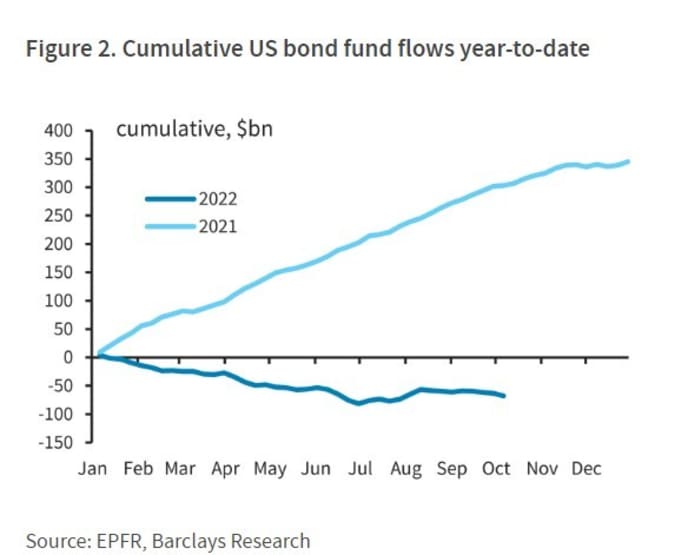

US Bond Mutual Fund Flows

Obviously, some went too far and are now facing losses if forced to sell to meet withdrawals.

So, what does the Fed do?

- Backstop depositors to prevent more bank runs.

- Provide low cost liquidity if needed.

- Set policies so that LT rates decline to restore bond portfolio values.

- A new QE. Really?

- First, stop QT.

- Anything else? If not…

- …Bring inflation down, i.e. recession, soon.

“The usage of the Fed’s Bank Term Funding Program is likely to be big,” strategists led by Nikolaos Panigirtzoglou in London wrote in a client note Wednesday. While the largest banks are unlikely to tap the program, the maximum usage envisaged for the facility is close to $2 trillion, which is the par amount of bonds held by US banks outside the five biggest, they said. (…)

The Federal Reserve may need to end its quantitative-tightening program early to preserve the amount of bank reserves in the financial system while also maintaining its hawkish signaling on interest rates, according to Citigroup Inc. (…)

“Their new BTFP facility is QE in another name – assets will grow on the Fed balance sheet which will increase reserves,” Citi strategists Jabaz Mathai, Jason Williams and Alejandra Vazquez Plata wrote in a note to clients on Monday. “Although technically they are not buying securities, reserves will grow.” (…)

The strategists see three options for the Fed. One would be stopping QT early or reducing the monthly amount of bonds it allows to roll off, to ensure reserves are relatively stable for the rest of the year.

Another choice would be to lower the maximum amount each money-market fund is allowed to park at the Fed’s reverse repurchase agreement facility from $160 billion, while allowing QT to run in the background.

A third possible route, according to Citigroup, is that the Fed stops hiking but continues its balance-sheet unwind, forcing money funds to extend the weighted average maturity of their holdings and pulling cash out of the RRP as they buy longer maturities. The strategists see this as unlikely since the Fed has shown it’s more comfortable tightening economic conditions via short-end rates. (…)

Bank Failures, Market Turmoil Fuel Bets on a Pause in Fed Rate Increases Interest-rate futures markets indicate a 50% chance of no increase at the central bank’s next meeting.

(…) “A pause now would send the wrong signal about the seriousness of the Fed’s inflation resolve,” said Michael Feroli, chief U.S. economist at JPMorgan Chase. It could also fuel fears that the Fed is hesitant to raise rates but quick to cut them, he said, because of concerns about financial stability—something economists refer to as “financial dominance.” (…)

- Big ECB Hike Called Into Doubt by Credit Suisse A half-point increase once seen as a sure thing has been thrown into question.

- Swiss central bank throws financial lifeline to Credit Suisse after shares pummelled Swiss regulators pledged a liquidity lifeline to Credit Suisse in an unprecedented move by a central bank after the flagship Swiss lender’s shares tumbled as much as 30% on Wednesday. ($54B)

- Large U.S. banks view Credit Suisse exposure as manageable -sources Bankers were more concerned about contagion or unexpected effects of the Swiss lender’s troubles that are not yet understood

Economy Shows Signs of Cooling as Bank Troubles Spread A drop in retail sales and an easing of inflation pressures last month shows the economy may be cooling after a hot start to the year.

(…) Spending fell at stores, online and in restaurants by a seasonally adjusted 0.4% in February, the Commerce Department said Wednesday, following a 3.2% jump in January.

A separate report Wednesday showed a measure of supplier inflation cooled last month. The producer-price index, which generally reflects supply conditions across the economy, fell 0.1% in February from the prior month, the Labor Department said. On a 12-month basis, producer prices rose 4.6% in February, slowing from January’s downwardly revised 5.7% gain. (…)

Over the past year retail sales have advanced 5.4%. (…)

In reality, retail sales were fairly strong last month. The 2.2% MoM drop in Food Services (still up 15.3% YoY!), quite normal after January’s huge 5.6% jump, masks the continued demand for goods (blue bar), up another 0.5% following January’s +2.3%.

On a YoY basis, total sales are up 5.4% and control sales 7.1%. Goods inflation (35% CPI-Durables + 65% CPI-Nondurables) was 3.5% in February, down from 4.4% in January and 4.7% in December. It peaked at 14.6% in March 2022.

U.S. Producer Prices Dropped in February

The producer-price index, which generally reflects supply conditions across the economy, fell 0.1% in February from the prior month, compared with a downwardly revised 0.3% increase in January, the Labor Department said Wednesday. That compared with a 0.2% average monthly rise in the two years before the pandemic.

The so-called core price index—which excludes the often-volatile categories of food, energy and supplier margins—climbed 0.2% in February from a month earlier, compared with a downwardly revised 0.5% in January.

On a 12-month basis, prices rose 4.6% in February, slowing from January’s downwardly revised 5.7% gain. Last month’s rise was down sharply from the 11.7% peak in March 2022, and was the lowest reading since March 2021. Core PPI increased 4.4% from a year earlier, the same pace as January’s revised gain. (…)

Not as good as it seems:

- Core PPI is up 4.2% annualized in the last 2 months from 3.6% in the previous 2 months.

- Core PPI-Goods is up 0.3% in February after 0.6% in January. Last 2 months: +5.5% a.r. vs 2.4% in the previous two.

- Total PPI-Services declined 0.1% in both January and February but only because retail margins and transportation and warehousing costs dropped. Excluding these items, PPI-Services rose 0.3% in February after 0.6% in January. Last 2 months: +5.6% a.r. vs 4.9% in the previous two.

JPMorgan Joins Those Saying Cash in Bond Gains The Fed may still raise rates, casting doubts on a recent rally.

ALL FED, AGAIN!

Still needing to fight inflation, it now has to mind the financial system its own policies drove into a bad pickle. The economy remains too strong, requiring more tightening, but financial markets need more liquidity while long rates must come down.

Good luck!

BTW: Empire State Manufacturing Survey: Activity Continues to Contract

Manufacturing activity continued to decline in New York State, according to the March survey. The general business conditions index fell nineteen points to -24.6, continuing the see-saw pattern of ups and downs within negative territory seen in recent months.

The new orders index fell fourteen points to -21.7, indicating that orders declined substantially, and the shipments index fell fourteen points to -13.4, pointing to a decline in shipments.

The index for number of employees fell four points to -10.1, its second consecutive negative reading, indicating that employment levels continued to decline. The average workweek index fell six points to -18.5, its lowest level since early in the pandemic, indicating that hours worked shrank for a fourth consecutive month.

Input prices and selling prices increased at a somewhat slower pace than last month: the prices paid index fell three points to 41.9, and the prices received index moved

down six points to 22.9.