Producer Prices Rose 6% in January

That increase in the producer-price index, which generally reflects supply conditions in the economy, was slower than December’s 6.5% gain, the Labor Department said Thursday. And it was down markedly from the 11.7% rise in March 2022, the recent peak.

The PPI increased 0.7% in January from the prior month, compared with a revised 0.2% drop in December, and significantly faster than the 0.2% average monthly rise in the year before the pandemic. (…)

The January report showed goods prices rose from a month earlier, largely reflecting energy products. Good prices had decreased in December. Services prices rose at the same monthly rate as in December.

The so-called core price index—which excludes the often-volatile categories of food, energy and supplier margins—climbed 0.6% in January from a month earlier, after gaining a revised 0.2% in December. On a 12-month basis, core PPI rose 4.5%, a cooling from a revised 4.7% gain in December.

Other data:

- PPI-Core Goods rose 0.6% (7.3% a.r.) after +0.1% in December and +1.6% a.r. in the second half of 2022.

- Core processed goods declined 0.2%, the 6th consecutive decline.

- PPI-Services rose 0.4%, roughly in line with the previous months.

BTW:

- Based on the recent CPI and PPI data, Goldman Sachs now estimates that the core PCE price index rose 0.55% in January (+4.50% YoY). That would be another shocker. Core PCE inflation was +0.3% in December and +0.2% on average in Oct-Nov.. GS adds a 3rd 25bp rate hike in June for a peak funds rate of 5.25-5.5%.

- “We now have oil crossing $100/bbl in late 4Q23.” (GS)

- James Bullard said he would have favored a half-point rate increase at the last meeting and that he would support moving as quickly as possible to raise rates to just below 5.5%. “I don’t see much merit in delaying our approach to that level.”

- Loretta Mester also saw a compelling

case for a 50-bp hike then. The Cleveland chief predicts the Fed will bump

its benchmark above 5% “and hold it there for some

time.”

Note that both Bullard and Mester are known hawks that are non-voters this year.

Jobless Claims Remain Nearly Steady Worker filings for unemployment benefits remained historically low last week, a sign of continued tightness in the labor market.

Initial jobless claims, a proxy for layoffs, decreased by 1,000 to a seasonally adjusted 194,000 last week, the Labor Department said Thursday. Weekly claims have remained below the 2019 prepandemic average of about 220,000 since the start of the year.

The four week moving average of weekly claims, which smooths out volatility, rose slightly to 189,500. (…)

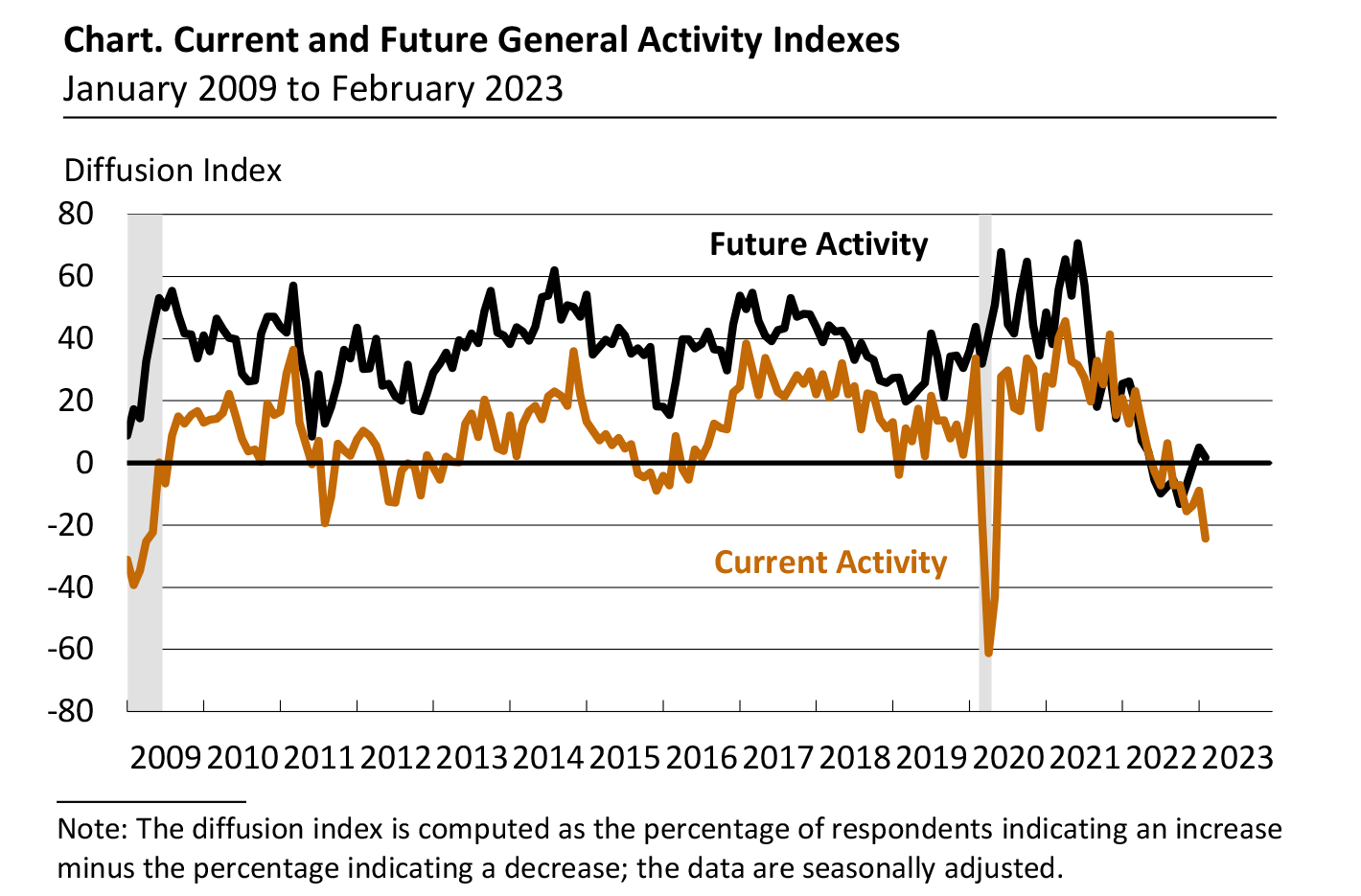

Philadelphia Fed manufacturing gauge plunges unexpectedly

The Philadelphia Federal Reserve’s monthly manufacturing index plunged to -24.3 this month from -8.9 in January, belying expectations among economists for a third straight monthly improvement. The median estimate in a Reuters survey of economists was for -7.4, and the reading was more than twice as weak as the lowest estimate in the poll.

Meanwhile, the survey’s two measures of prices, those paid by producers and those they charge their customers – both closely watched inflation indicators – showed margins were slimming. The prices paid index edged up to 26.5 from 24.5 to mark its first increase since April 2022, while the prices received index fell by 50% to 14.9, the lowest reading since February 2021.

In a special question, firms said they expect to impose 4.5% price increases for their own products in the year ahead, down from 4.8% when asked the same question in November and also lower than the 7.0% price increases they’d realized over the last year.

For U.S. consumers overall, producers in the survey estimated prices would increase 4.0% over the next 12 months, down from 5.0% in the November survey, and their expectations for longer-run consumer inflation over a 10-year horizon dropped to 3.0% from 4.0%.

Wage increases were also expected to be lower at 4.8% in the year ahead, down from 5.0% in the November survey.

- The [NY] Empire manufacturing index increased by 27.1pt to -5.8 in February, above consensus expectations for a smaller increase. The underlying composition was mixed, as the new orders (+23.3pt to -7.8) and shipments (+22.5pt to +0.1) components increased while the employment component declined into contractionary territory (-9.4pt to -6.6). Both the prices paid (+12.0pt to +45.0) and prices received (+9.6t to +28.4) components increased. The six months-ahead business conditions index increased 6.7pt to +14.7.

")

NY Business Leaders Survey

Activity continued to decline in the region’s service sector, though at a slower pace than last month, according to firms responding to the Federal Reserve Bank of New York’s February 2023 Business Leaders Survey.

The survey’s headline business activity index climbed nine points to -12.8. The business climate index came in at -34.9, suggesting the business climate remains much worse than normal. There was a small rise in employment, and wage growth steepened. The pace of input price increases and selling price increases picked up somewhat. Looking ahead, firms expect conditions to improve modestly over the next six months.

Business activity declined in the region’s service sector for a fifth consecutive month, according to the February survey. The headline business activity index rose nine points but remained negative at -12.8. Twenty-seven percent of respondents reported that conditions improved over the month and forty percent said that conditions worsened. The business climate index moved up seven points to -34.9, suggesting that the business climate remains much worse than normal.

The employment index inched up to 5.8, suggesting a small increase in employment levels. The wages index advanced ten points to 56.7, indicating that wage growth remained widespread. The prices paid index edged up three points to 69.0, and the prices received index rose four points to 33.7, pointing to slightly more rapid price increases than last month. Capital spending grew modestly.

Conditions are expected to improve somewhat over the next six months. The index for future business activity climbed to 8.2, its first positive reading since September 2022, while the index for the future business climate moved up twenty-three points to -4.1. Employment is expected to grow in the months ahead, and wage and price increases are expected to remain widespread.

")

(…) Looking at the past twelve months, the median reported change for existing workers was 5 percent among service firms and 6 percent among manufacturers; the average changes were slightly higher. These are considerably steeper increases than seen both prior to the pandemic and in the midst of the pandemic, in April 2021, when we last asked this question. Looking ahead to the next twelve months, the average expected change was projected to slow to just over 3 percent, for both service and manufacturing firms. These increases are roughly in line with what we saw in earlier surveys.

Businesses were also asked how wages and salaries for new hires were seen changing from 2022 to 2023. Here, both service and manufacturing firms estimated an average (and median) increase of about 5 percent. For service firms this is a considerably steeper rise than when we asked these questions during the pandemic (April 2021) and moderately steeper than pre-pandemic (February 2018). In those earlier surveys, this question was asked with respect to the past twelve months, as opposed to the current versus prior calendar year. (…)

Finally, businesses were asked how many job openings they currently have and (in order to scale these numbers to the size of the business) how many people they currently employ.

In both the service-sector and manufacturing surveys, the median respondent reported that job openings represented just over 4 percent of their firm’s total employment. This is down somewhat from about 5 percent in last February’s survey but up considerably from earlier surveys—notably, we have been asking this question at the beginning of the year for more than a decade; prior to 2022, this proportion had never exceeded 3 percent for manufacturers or 2.5 percent for service firms.

- Housing starts decreased by 4.5% to 1,309k in January, below consensus expectations for a 1.9% decrease, from a downwardly revised December level (-2.0pp to -3.4%). The composition was weak, as both single family starts (-4.3%) and the more volatile multi-family starts (-4.9%) decreased. Building permits increased by 0.1%, below consensus expectations for a 1.0% increase. Single family permits continued to decline (-1.8%), while multi-family starts increased (+2.5%).

Americans Have Nearly $1 Trillion in Credit Card Debt The overall balance increased in the final quarter of 2022, breaking a record set in 2019.

The $61 billion increase from the prior quarter was the biggest seen in data going back to 1999, and propelled Americans’ total credit card debt past the previous high of $927 billion, which was set in the fourth quarter of 2019, according to the New York Fed’s Household Debt and Credit Report.

Credit card borrowers aren’t just swiping plastic more than ever — they’re missing payments too, with delinquency rates surpassing pre-pandemic norms. A little over 4% of credit card debt has transitioned to serious delinquency, which means failing to pay for 90 days or more. (…)

Altogether, credit card balances ballooned by $130 billion from December 2021 to December 2022 — the largest annual growth on record. As the Fed continues to hike interest rates, credit card borrowing costs are expected to hit a 40-year high this year.

“It’s triple trouble for credit card borrowers. Balances are up, rates are up and more people are carrying credit card debt,” said Ted Rossman, a senior Bankrate analyst, adding that 46% of credit card holders are carrying debt, up from 39% a year ago.

BofA Says Says Hard Landing to Hit Stocks in Second Half A resilient economy thus far means interest rates will stay higher for longer, the strategists wrote.

Short covering extreme

Nobody has missed the short covering frenzy, but GS puts some numbers to it: “…the short covering in US Tech stocks from Jan 31st to Feb 15th is the second largest in magnitude over any 12-day period in the past decade and ranks in the 99.5th percentile.” (The Market Ear)

GS

![]() Tesla is recalling 362,758 vehicles equipped with its controversial “Full Self-Driving beta” (FSD) software, which federal safety investigators found can occasionally disregard traffic laws. (Axios)

Tesla is recalling 362,758 vehicles equipped with its controversial “Full Self-Driving beta” (FSD) software, which federal safety investigators found can occasionally disregard traffic laws. (Axios)

![]() Let’s hope they don’t self-drive to the service centers all at the same time.

Let’s hope they don’t self-drive to the service centers all at the same time.