Empire State Manufacturing Survey

- Manufacturing activity declined in New York State, according to the October survey. The general business conditions index fell eight points to -9.1.

- The new orders index was unchanged at 3.7, indicating a slight increase in orders

- The index for number of employees was little changed at 7.7, pointing to a modest increase in employment levels, and the average workweek index climbed to 3.3, signaling a slight increase in hours worked. After falling significantly over the prior three months, the prices paid index rose nine points to 48.6. The prices received index held steady at 22.9.

- The index for future business conditions fell ten points to -1.8, indicating that firms do not expect conditions to improve over the next six months. The indexes for future new orders and shipments remained depressed, though employment is expected to continue to increase.

Bank of America CEO Says Consumers Are in Good Shape But the bank socked away funds to prepare for a possible recession

The company’s data show that spending growth remains strong in terms of both amounts and number of transactions. Americans are spending in particular on travel and entertainment, which tend to be discretionary items. Deposit balances remain higher than prepandemic levels by multiple times and delinquencies remain low. (…)

Mr. Moynihan’s remarks Monday stand in contrast to other big-bank CEOs, namely JPMorgan Chase & Co.’s Jamie Dimon, who reiterated his belief Friday that an economic “hurricane” is coming. JPMorgan executives said consumers will deplete the extra money in their checking accounts around the middle of next year.

Despite Mr. Moynihan’s optimism, there were some notes of caution. Spending growth, while still high, slowed to 10% in September, versus 12% for the year so far, according to the bank’s metrics. (…)

![]() Use of credit cards (blue) tends to increase when real income growth (black) weakens. The fact that revolving credit rises faster than actual spending (red) is not a sign of a healthy consumer.

Use of credit cards (blue) tends to increase when real income growth (black) weakens. The fact that revolving credit rises faster than actual spending (red) is not a sign of a healthy consumer.

In fact, banks are tightening credit standards…

Microsoft becomes latest tech firm to cut staff. (Axios)

MAKE YOUR BETS!

First, the lay of the lands from Haver Analytics:

The 6-month change in Haver’s aggregation of policy rates in advanced economies topped 2% in September. That’s the fastest pace of interest rate tightening in our aggregation’s history, which kicks off in the early 1980s.

Policy rates in advanced economies

One of the factors that is further tightening global monetary conditions is the ongoing appreciation in the US dollar. As our final chart this week suggests an appreciation in the trade-weighted value of the US dollar typically accompanies weaker growth in emerging economies.

Still, the strength of the dollar remains impressive – indeed arguably too impressive – relative to those EM growth fundamentals. This suggests that other factors (e.g. rising risk aversion) have been playing a big role in driving the dollar up.

The US dollar versus EM growth surprises

The latest recession probability models by Bloomberg economists Anna Wong and Eliza Winger forecast a higher recession probability across all timeframes, with the 12-month estimate of a downturn by October 2023 hitting 100%, up from 65% for the comparable period in the previous update. (…)

While the chance of a recession within 12 months has reached 100% under the model, the odds of a recession hitting sooner are also up. The model forecasts the likelihood of a recession within 11 months at 73%, up from 30%, and the 10-month probability rose to 25% from 0%. (…)

A separate Bloomberg survey of 42 economists predicts the probability of a recession over the next 12 months now stands at 60%, up from 50% a month earlier.

- Economists Now Expect a Recession, Job Losses by Next Year Majority think Federal Reserve will start cutting rates in late 2023 or early 2024

On average, economists put the probability of a recession in the next 12 months at 63%, up from 49% in July’s survey. It is the first time the [WSJ] survey pegged the probability above 50% since July 2020, in the wake of the last short but sharp recession.

Their forecasts for 2023 are increasingly gloomy. Economists now expect gross domestic product to contract in the first two quarters of the year, a downgrade from the last quarterly survey, whereby they penciled in mild growth.

On average, the economists now predict GDP will contract at a 0.2% annual rate in the first quarter of 2023 and shrink 0.1% in the second quarter. In July’s survey, they expected a 0.8% growth rate in the first quarter and 1% growth in the second. (…)

Economists believe that nonfarm payrolls will decline by 34,000 a month on average in the second quarter and 38,000 in the third quarter. According to the last survey, they expected employers to add about 65,000 jobs a month in those two quarters. (…)

Some 58.9% of economists said they think the Fed will raise interest rates too much and cause unnecessary economic weakness, up from 45.6% in July. (…)

Of the economists who see a greater than 50% chance of a recession in the next year, their average expectation for the length of a recession was eight months. The average postwar recession lasted 10.2 months.

For the year as a whole, they expect the economy to grow 0.4% in 2023, through the fourth quarter compared with the fourth quarter of the prior year. In 2024, they see the economy growing 1.8%. (…)

They predict the unemployment rate, which was 3.5% in September, will rise to 3.7% in December and 4.3% in June 2023. Economists’ average forecast for the jobless rate at the end of next year is 4.7%, and they expect it to stay broadly at that level through 2024. (…)

Economists expect home prices to decline 2.2% in 2023, measured by the U.S. Federal Housing Finance Agency’s seasonally adjusted purchase-only house price index. That would mark the first such decline since 2011. (…)

Economists on average expect the Fed to lift the federal-funds rate to 4.267% in December, which implies at least one more increase of 0.5 point that month. They see the federal-funds rate peaking at 4.551% in June next year. (…)

Some 30% of economists expect the central bank to lower rates in the fourth quarter of 2023, and 28.3% expect the next rate cut in the first quarter of 2024.

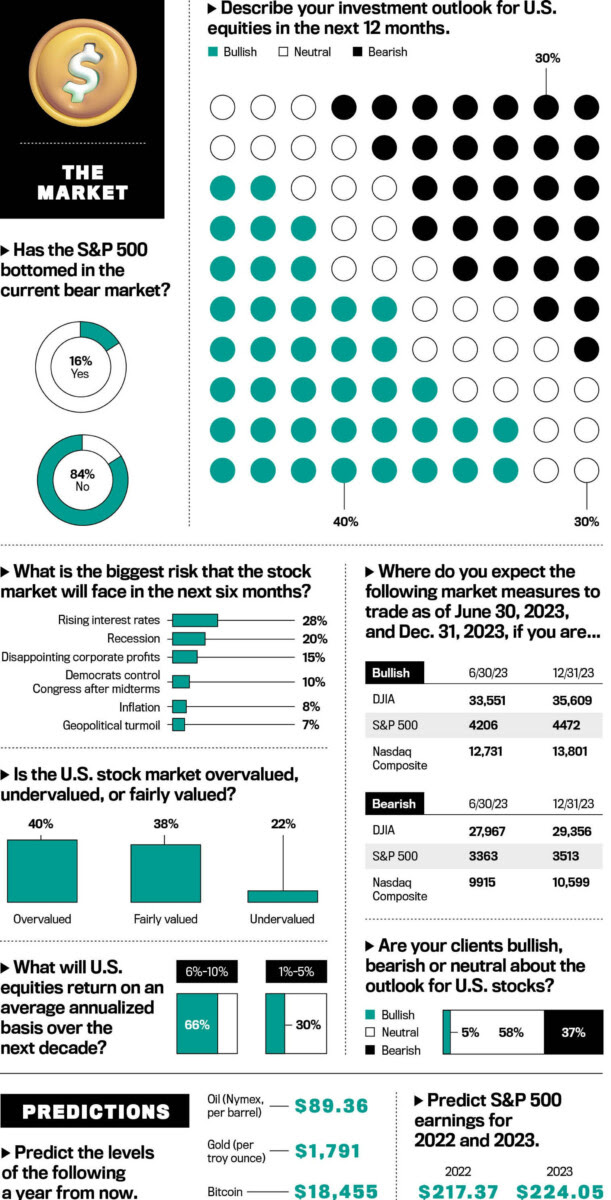

Patience in a volatile market like this year’s is a tall order. But it is the recipe for long-term success espoused by institutional investors in Barron’s latest Big Money poll. Big Money respondents are relatively negative about the near-term trajectory for financial markets, but optimistic about opportunities over the longer term, given the most attractive entry points in years for both stocks and bonds.

Our latest survey finds 40% of money managers bullish about the outlook for stocks over the next 12 months, and 30% bearish. The bullish cohort has increased from 33% since the spring edition of the poll, which found a plurality of managers neutral, but the bearish contingent has also grown from 22%. (…)

Kolanovic, who has been Wall Street’s most vocal bull this year, cut the size of his equity overweight and bond underweight allocations, citing increasing risks from central bank policies and geopolitics. (…)

Kolanovic, voted the No. 1 equity-linked strategist in last year’s Institutional Investor survey, hasn’t had much success with his bullish calls so far in 2022. Over the summer he maintained that the US stock market was poised for a gradual recovery in 2022 and that the S&P 500 would likely end the year unchanged, repeatedly urging investors to buy the dip. (…)

“We expect the global expansion to continue to display resilience through the middle of next year given an unwind of adverse supply shocks, a material slowing in inflation, and a healthy private sector,” he said.

The bank’s monthly global fund manager survey “screams macro capitulation, investor capitulation, start of policy capitulation,” strategists led by Michael Hartnett wrote in a note on Tuesday. They expect stocks to bottom in the first half of 2023 after the Federal Reserve finally pivots away from raising interest rates.

“Market liquidity has deteriorated significantly,” the strategists said, noting that investors have 6.3% of their portfolios in cash, the highest since April 2001, and that a net 49% of participants are underweight equities.

Nearly a record number of those surveyed said they expect a weaker economy in the next 12 months, while 79% forecast inflation will drop in the same period, according to the survey of 326 fund managers with $971 billion under management, which was conducted from Oct. 7 to Oct. 13.

As the earnings season gains traction, 83% of investors expect global profits to worsen over the next 12 months. A net 91% said global corporate profits are unlikely to rise 10% or more in the next year — the most since the global financial crisis — a sign that suggests further downside to S&P 500 earnings estimates, according to the strategists.

Global equities have rallied in recent days amid support from technical levels, changes in UK government policies and a focus on earnings. Hartnett and his team described the rally after a US inflation print last week as a “bear hug.” (…)

Can we learn anything from the dates above?

- July 2000: the S&P 500 peaked in August 2000.

- March 2001: down 24%, the S&P 500 rallied 8% in 2 months before resuming its downtrend.

- October 2001: down 30% from August 2000, another 8% rally over 5 months before cratering to 815 in September, down 46% since August 2000.

- March 2003: The actual low.

- December 2008: the S&P 500 was down 41%. Another 26% drop occurred before the March 2009 low.

- June 2012: Rising market.

- October 2016: Rising market.

- April 2020: Near pandemic low.

Answer: not a dependable contrarian signal.

Bank of Canada Sees Worst Drop in Business Outlook Since 2020

Sentiment among Canadian firms fell the most since the beginning of the pandemic, with inflation expectations among consumers and businesses showing few signs of abating, Bank of Canada surveys show.

The central bank’s business outlook indicator fell to 1.69 in the third quarter, from 4.87 previously. While still positive, that’s the largest deterioration in the confidence of Canadian firms since the second quarter of 2020.

“Many firms expect slower sales growth as interest rates rise and demand growth shifts closer to pre-pandemic levels,” policymakers said Monday in the quarterly business outlook survey. Respondents noted that while they see their input and output prices easing, expectations of overall inflation remain elevated. More than three quarters of firms say inflation will stay higher than 3%, the top of the central bank’s control band. (…)

Most businesses and consumers think a recession is likely within the next 12 months, triggered by large increases in interest rates and high prices that reduces consumption. The two groups also see inflation remaining elevated over the next one or two years before returning to the central bank’s target in the long term.

While both have similar inflation expectations and views on the probability of a recession, they diverge on wages.

The average expected wage increase among businesses has receded, with nearly half not seeing abnormally high wage growth beyond the next 12 months. But consumer expectations for wage growth have increased, with 40% of workers now seeing pay gains of more than 4% over the next year.

With firms expecting demand to slow and resisting large wage increases, consumers said their wages weren’t keeping up with inflation and believed they wouldn’t catch up, resulting in spending cuts and changes in shopping habits. Consumers also see shrinking real wages as the main trigger of a recession.

Most firms said rate hikes aren’t yet holding back their investment plans. But fewer businesses are planning to hire, and some in information technology, engineering and trades are constrained by supply of skilled workers. (…)

U.S. could sell oil from reserve this week. (Reuters)

China:

For three days in a row on Oct 10-12, the People’s Daily published three articles emphasizing the importance for China to stick with the “dynamic zero-Covid policy”, sending the clearest signal yet that zero-Covid policy will not be abandoned anytime soon. Our latest high-frequency tracker shows that cities with high-/mid-risk districts now account for 40% of the national GDP, implying continued pressure on consumption and services in October. (GS)

No recession cover in sovereign bonds (BlackRock)

Recession fears are roiling markets. Investors traditionally take cover in sovereign bonds, but we see this recession playbook as obsolete. Why? First, central banks are hiking rates to try to tame inflation, causing recessions. Second, we don’t see them cutting rates like they typically do in recessions due to persistent inflation. Third, we expect investors to demand more compensation for the risk of holding government bonds amid high debt loads. Result: We stay underweight Treasuries.

In the Great Moderation, a period of steady growth and inflation, central banks would have eased policy on signs of contracting growth. That era is over. Now central banks are set to induce recessions by overtightening policy. In this supply driven recession, high inflation and rising rates may break the fragile equilibrium where investors tolerated surging debt loads and forwent a higher term premium, or compensation for the risk of holding long-term bonds.

The UK offers a glimpse of this. Long-missing bond vigilantes are back as markets question UK macro policy credibility. And financial dislocations have accelerated and amplified the move. The difference between 10-year and two-year gilt yields (orange line in chart) has surged. Yet yield curve moves of German bunds (pink) and Treasuries (yellow) show a muted response not yet pricing in a higher term premium.

We see long-term yields rising across developed markets. Why? Policy, inflation and debt. Central banks in the new regime face a sharper trade-off between growth and inflation than in the past. Yet their forecasts, as well as the International Monetary Fund’s update last week, aren’t acknowledging that the cost of bringing inflation down to targets is triggering recession, in our view. We think central banks will eventually halt rate hikes.

But they won’t have done enough to get inflation all the way back down to target, implying they won’t be able to start easing policy, in our view. Higher policy rates and inflation create a ripe environment for investors to demand higher term premia for long-term bonds.

All of this underscores why the old recession safe-haven playbook doesn’t apply. That’s no mere musing: We see it playing out in the UK in real time. The energy crisis had already put the UK on the brink of recession. The Bank of England (BoE) could exacerbate the pain by hiking rates even more than originally expected to offset fiscal stimulus. Backlash to the planned stimulus has sparked a gilts selloff and led to the finance minister’s resignation.

The BoE’s two-week buying of long-term bonds helped briefly drag down yields, but they spiked anew as the program ended last week. While the government has trimmed its tax cut plans, they have already dented UK fiscal credibility and would still add to the debt build-up during the Covid-19 shock. In this environment, bond vigilantes are back and heralding term premium’s return.

The upshot: We’re broadly underweight government bonds. U.S. bond returns are the most positively correlated to stocks in two decades on a 90-day rolling basis. We expect that correlation to stay positive, erasing bonds’ role as portfolio diversifiers.

We don’t think long-term yields reflect the likely persistence of inflation and higher term premia coming as a result. Higher short-term rates also make the long end less attractive because investors can get decent returns in short-dated bonds with less interest rate risk. We stay underweight U.S. Treasuries. Policy rates would need to hold steady or fall for Treasury returns to flip positive, we find.

Blinken Says China Wants to Seize Taiwan on ‘Much Faster Timeline’

China has made a decision to seize Taiwan on a “much faster timeline” than previously thought, Secretary of State Antony Blinken said on Monday, shortly after China’s leader reiterated his intent to take the island by force if necessary. (…)

“If peaceful means didn’t work, then it would employ coercive means,” he said. “And possibly, if coercive means don’t work, then maybe forceful means to achieve its objectives. And that is what is profoundly disrupting the status quo and creating tremendous tensions.” (…)

Chinese President Xi Jinping used a widely-watched speech on Sunday to say the “wheels of history are rolling on towards China’s reunification” with Taiwan. While peaceful means were preferable, Xi added, “we reserve the option of taking all measures necessary.” (…)

(…) “China’s international influence, appeal and power to shape the world has significantly increased,” Xi said in Beijing on Sunday in a wide-ranging speech to open the weeklong party congress. Still, he warned of a more unstable international environment, saying China must be prepared for “strong winds and high waves and even dangerous storms.” (…)

Fleshing out his “common prosperity” slogan, Xi adopted tougher language on tackling income inequality, calling to “regulate income distribution and regulate the mechanism behind the accumulation of wealth.” In his 2017 congress speech, Xi only called to “promote a more orderly and reasonable income distribution” and “adjust excessively high incomes.” (…)

Xi also emphasized calls for “self-reliance” in technology, using the phrase at least twice compared with no references in his last congress speech in 2017. (…)