Consumer Demand Snaps Back. Factories Can’t Keep Up. Snarled supply chains, labor shortage thwart full reopening; ‘everyone was caught flat-footed’

(…) Without restaurants to visit and trips to take, Americans bought out stocks of cars, appliances, furniture and power tools. Manufacturers have been trying to catch up ever since. Nearly a year since initial coronavirus lockdowns in the U.S., barbells, kitchen mixers, mattresses and webcams are still hard to find. A global shortage of semiconductors has forced many car makers to cut production in recent weeks. (…)

Consumer spending on long-lasting goods in the U.S. rose 6.4% last year but domestic production of those goods fell 8.4%, according to federal data, leading to shortages and higher prices.

(…) companies are placing supersize orders to compensate for the extra time it takes to procure supplies from factories and freight operators constrained by global efforts to contain the coronavirus. That’s exacerbating the strain on supply chains. (…)

“The global supply chain is not as strong as people thought,” Mr. Pin said. (…) “The entire supply chain was stressed in 2020 and is still in a bad spot,” founder Bill Henniger said. “The machinery, workforce and facilities are all running 24 hours a day.” (…)

Stanley’s tools business reported a 57% increase in profit for the fourth quarter on a 25% increase in sales, partly fueled by its ability to boost prices. Sales of electric sanders so far during the first quarter of 2021 are fourfold higher than the same time last year. (…)

Mr. Greenblatt said finding steel in the U.S. to increase his production has been a challenge. Prices for steel, copper and other industrial commodities are at the highest point in years. That is putting pressure on profit margins for Marlin and other manufacturers. (…)

The reduction in domestic production of specialty metals including stainless steel is even more acute. By the end of the year, just three companies in the U.S. will supply stainless steel. (…)

Domestic steel prices have risen more than 160% since last August, leaving steel consumers in a quandary – whether to absorb or pass along the increased cost.

“We’ll be lucky if we break even at this price,” said Stuart Speyer, president at Tennessee-based Tennsco. Steel costs for the manufacturer of lockers, bookcases and cabinets are up 98% in the past six months.

Whirlpool last month said increased steel costs would shave 150 basis points from its profit this year. Farm equipment maker AGCO and crane maker Terex have announced price increases to offset material costs. (…)

U.S. steel prices are 68% higher than the global market price and almost double China’s, even with prices in both China and Europe up over 80% from their pandemic-induced lows.

The price gap is so wide that even with a 25% tariff, it would be cheaper to import than buy from domestic mills. The United States imported 18% of its steel needs last year.

Logistical challenges, like container shortages, and thin overseas supply are keeping imports in check. But some distributors expect imports to pick up by June if the domestic market remains tight. (…)

- European manufacturers hit by surge in price of resins used to make plastic Extra costs may be passed to supermarkets and consumers, if prices remain elevated at 6-year highs

How AIT hesitancy can turn into JPOWs taper tantrum

It is very easy to defend an average inflation targeting regime as long as you are not overshooting. BUT (!) will it be as easy when core inflation prints around 2.75% by summer? We doubt it, which is why a taper tantrum 2.0 is a clear risk. (…)

There are reasons to be more structurally upbeat on inflation this time around compared to earlier reflationary cycles. China’s output prices are rising, supply chains have been disturbed, freight rates are elevated, but more importantly the policy mix has changed. Mechanisms that ensured a transfer of freshly printed USD to households/corporates were put in place through most of 2020, not least due to direct transfers of money but also due to publicly backed credit programmes. QE is not inflationary unless the USD or EUR actually reach the real economy, which actually happened in 2020. Bidenomics may further reflate this story, with even bigger direct cheques in store for the average American household.

(…) As long as bond yields rise for the right reasons, then they will be allowed to go higher. In other words, if spreads remain compressed, equity multiples (forward P/Es) increase and inflation expectations increase, then higher bond yields will be accepted. So far so good; of course the cocktail of higher long bonds yields, higher multiples and lower spreads will not last forever, but it may continue in a peaceful way until the re-opening actually happens, and therefore the Fed may be stuck behind the curve, if they actually want to prevent a tightening of financial conditions. (…)

The Fed keeps repeating that the “appropriate monetary policy will likely aim to achieve inflation moderately above 2% for some time”, but we are not any wiser on what exactly that means after the FOMC minutes this week. This is the KEY question for 2021 and it will be tested as early as in Q2. Will the Fed for example accept core inflation overshooting by e.g. 0.5-0.75% point? (…)

No matter whether the Fed actually takes the decision to taper purchases (or decide to sound “hesitant” on accepting too much inflation overshooting), the mere risk of it happening will influence markets into Q2, and several of our leading indicators have already started to warn of peakish key figure momentum by the middle of this year, with potential new setbacks into 2022, not least as the impulse from higher rates and energy prices will dampen momentum 9-12 months from now. (…)

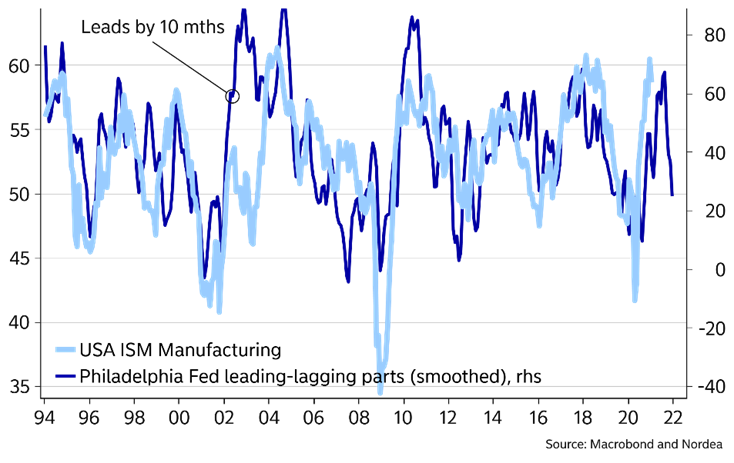

Some trouble brewing during H2-2021 according to our Philly Fed subcomponent indicator

BTW, FYI, simple exercise assuming CPI and Core CPI rise 0.2% MoM throughout 2021: CPI reaches +3.3% YoY in May and retreats to +2.5% in December; Core CPI reaches +2.5% in May and retreats to +2.2% in December. Get ready to hear the word “transitory” ad nauseam.

Nordea continues:

All of the above will furthermore be unfolding amidst talking points such as a “roaring 20s” and “cracks in secular stagnation”. And the US curve isn’t that steep, so why not just keep your steepeners on and hope for the best? That’s what we would do.

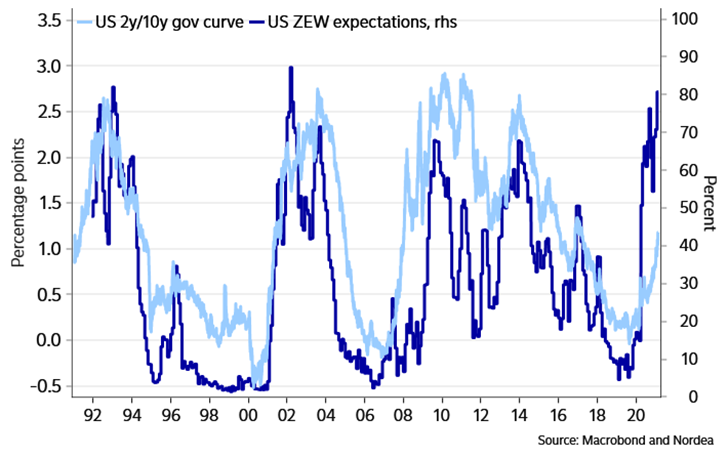

US curve lagging behind sentiment survey indicators

If for instance the Fed manages to tighten policy by a cumulative 225bps as they did in the last tightening cycle, why shouldn’t the curve look at least as steep as during that cycle? (AIT and MMT-like politics if anything suggest even more risk premiums today than back then, we believe). The last time we had US ZEW expectations at today’s stellar levels – in 2002, the curve traded at 170bps and was on track for a move to 275bps(!).

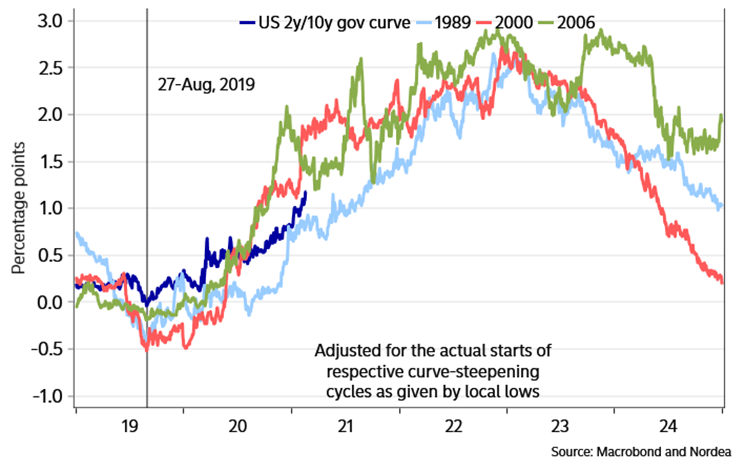

Not even half-way there, given previous big steepening trends

- Mind the gap between the PMI and the US10YR. The gap is impressive. The 10-year US Treasury Yield has further to rise.2. Tactical turning point: manufacturing is reaccelerating. Without central bank intervention, the 10y Treasury yield would be close to 3%. (The Market Ear)

And while Nordea is “clearly on the US outperformance side of the [EUR/USD] bet over the coming 6-9 months”…

In the longer run, we are not too upbeat on the dollar. Did you for instance notice that the CNY’s share of global swift payments rose to its highest share since 2016 in January? And what if China is successful in its DC/EP roll-out (which we will hear much more about around the Winter Olympics of 2022)? We actually see four reasons why the dollar smile could move to the dollar’s detriment over the coming decade: i) Biden “bananafying” the Fed, ii) China’s DC/EP and the weaponisation of the dollar, iii) energy politics, iv) regulation and taxes. You can read more on the dollar smile and its future here.

John Authers: How Much Do Central Banks Fear the Bond Toddler? So far, it looks like they will give the market what it wants.

(…) Markets are looking for a parental response. Central banks have said they are going to leave rates lower for longer this time. Do they really mean it? If yields go up half a percentage point in short order (the monetary equivalent of threatening to scream until you’re sick), will central banks relent at the risk of an even bigger tantrum next time, or opt to draw the disciplinary line, and put up with the screaming?

We’ve had two skirmishes between central bankers and markets already this week, with another to follow Tuesday as Federal Reserve Chairman Jerome Powell testifies to Congress. So far, it looks as though all of them will opt for giving the market what it wants, and risking spoiling the child. (…)

[Monday, Christine Lagarde] told the European parliament that the ECB was would maintain “favorable financing conditions” throughout the pandemic period. “Banks use those yields as a reference when setting the price of their loans to households and firms,” Lagarde said. “Accordingly, the ECB is closely monitoring the evolution of longer-term nominal bond yields.”

(…) That leads to the widespread presumption that Powell will have to say something to pacify the markets when he talks to Congress (…).

There is a rotation going on within the market, but it isn’t affecting the overall level of equities. While this continues to be true, the Fed won’t be too alarmed. It is when bond yields have risen too much for the stock market that they will also have risen too much for the Fed. So the chance of any fresh policy action or new money that hasn’t already been announced is very low.

CONSUMER WATCH

Sales have bounced back from the April low, but will likely be down around 7% year-over-year in February. The weather has impacted sales this month. The Wards forecast of 15.6 million SAAR, would be down about 6% from January.

- A Different Early-Bird Special: Have Vaccine, Will Travel People over 65 have been among the first in line to receive Covid-19 vaccinations. And they are leading a wave in new travel bookings.

-

*ROYAL CARIBBEAN NEW BOOKINGS +30% THIS YEAR VS. NOV.-DEC.: CFO

CHINA WATCH

The Market Growth Services sector Index is now at a 42 month high, although the manufacturing sector Index remains some way behind.

The Sales Growth Index backs up the buoyancy of business confidence, with data relating to actual revenues as opposed to beliefs about the future. Both Manufacturing and Services Indexes show very positive numbers well above the 50 “no growth” line.

Unlike in the USA, where price movements are starting to look suspiciously like turning into renewed inflation, prices appear more under control in China, and indeed in the manufacturing sector are actually falling as production is ramped up.

However, the Jobs Index does not suggest that recruitment levels are back to pre Covid levels in the manufacturing sector. As in the USA, it appears that the experience of Covid has left many companies still very cautious and as yet reluctant to recruit. However in the Services sector the Jobs Index is now at an 80 month high, reflecting the recovery to positive levels of the Sales and Market Growth Indexes.

ISRAEL WATCH

A new WATCH given Israel’s huge lead in vaccination, perhaps offering clues for the ROW.

-

Israel’s stores, gyms, hotels to reopen Sunday

- Israelis saving record one third of disposable income

(…) The rise in the rate of saving, despite the high level of unemployment in the Israeli economy, which reached 18% in January, is a probably a result of two parallel forces. One is the money that the government distributed to all citizens indiscriminately last year, because it was unable to distinguish between those in need of aid and those who were not. The other is the lockdowns, which reduced private consumption by more than 9% in 2020. (…)

The Central Bureau of Statistics figures show that net saving by households in Israel in 2020 rose to a record 31.2% of disposable income. For the sake of comparison, in 2019, the rate of private saving was 21.3% of disposable income. Elsewhere in the world, saving rates were lower. In Canada, for example, the rate of saving as a proportion of disposable income was 15% in 2020 and 6.7% in 2019, and in the US the figures were 13.7% and 7.5%. (…)

- Housing sales in Israel hit 20-year high in 2020 In 2020 there were 107,100 housing deals, while of the highest numbers in recent years. 62,000 of the deals were in the second half of the year, the highest number of homes sold in a six month period for 20 years

- Demand in Israel doubles for houses with gardens

-

Home price rise in Israel becomes a leap

(…) Between the end of that lockdown [April] and last November, home prices rose by 3.6%, giving an annualized rate of increase of 6%, much of which, as mentioned, occurred starting from the second lockdown. (…)

The housing prices index, which is separate from the CPI, continued to rise in the period November-December, in comparison with October-November, climbing by 0.9%, after rising 1%% the previous month. Housing prices have risen 4% over the past 12 months.

The prices of new homes rose by 0.5% in November-December, in comparison with October-November, and have risen by 3.1% over the past 12 months.

Tech Stocks Drop Amid Rising Bond Yields The Nasdaq Composite declines as rising government-bond yields prompted concern that technology shares are looking too expensive.

Market divergence continues

The benchmark 10-year Treasury yield rose to 1.37%, a fresh one-year high, showing investors remain bullish on the economy and a recovery in inflation. (…) Along with the jump in bond yields, oil jumped by nearly 4%, gold and silver rose and commodities rose to their highest in almost eight years, as investors continued to buy assets that will benefit from reduced COVID-19 cases and a growing economy.

Data: FactSet; Chart: Axios Visuals

-

The stock market’s highest flyers remain under pressure this morning. Futures for the tech-heavy Nasdaq 100 dropped 1.5%, after the index slumped 2.6% in trading yesterday on a selloff in some of the hottest pandemic buys such as Peloton Interactive Inc. which sank 10%. Tesla Inc. shares are set to tumble again at the open with futures trading well south of $700. CEO Elon Musk’s bet on Bitcoin also took a hit with the cryptocurrency dropping significantly again this morning. (Bloomberg)

Yellen Favors Higher Company Tax, Signals Capital Gains Worth a Look

Treasury Secretary Janet Yellen said President Joe Biden favors boosting taxes on companies, and signaled openness to considering raising rates on capital gains, while steering clear of a wealth levy.

“A wealth tax has been discussed but is not something President Biden” favors, Yellen said at a virtual conference on Monday hosted by the New York Times. She said such a tax would have significant implementation problems.

The administration is looking to boost the corporate tax to 28%, Yellen said. The Treasury chief said last week that revenue measures would be needed to help pay for Biden’s planned longer-term economic reconstruction program to help address concerns about debt sustainability.

Yellen also said that a hike in the capital-gains tax might be something “worth considering.” Asked about a financial-transactions tax, she said, “One would have to examine closely what effect it would have” on ordinary investors. (…)

Yellen separately signaled the Biden administration supports research into the viability of a digital dollar. “Too many Americans don’t have access to easy payments systems and banking accounts, and I think this is something that a digital dollar, a central bank digital currency, could help with,” she said.

- Treasury Secretary Janet Yellen said “people should be aware” of bitcoin’s extreme volatility, saying it’s “an extremely inefficient way to conduct transactions” and calling the amount of energy needed to mine bitcoin “staggering.” (New York Times)

COVID-19

- In the U.S., the latest vaccination rate is 1,365,820 doses per day, on average. At this rate, it will take an estimated 10 months to cover 75% of the population with a two-dose vaccine. (…) So far, 44.1 million have received at least one dose. At least 19.4 million people have completed the two-dose vaccination regimen. Globally, the latest vaccination rate is 6,242,182 doses per day, on average. At this rate, it will take an estimated 5 years to cover 75% of the population with a two-dose vaccine. (Bloomberg)

- The vaccines are working

Long-term care facilities have been responsible for 35% of all coronavirus deaths in the U.S., despite accounting for less than 1% of the population. (Axios)

Data: The COVID Tracking Project. Chart: Michelle McGhee, Andrew Witherspoon/Axios