U.S. Durable Goods Orders Disappoint in March

Manufacturers’ orders for durable goods rose 0.5% in March (25.0% y/y) after falling 0.9% during February due to winter storms, revised from -1.1%. A 2.4% jump had been expected in the Action Economics Forecast Survey.

Last month’s disappointment owed largely to a 1.7% decline (+62.5% y/y) in transportation orders as it followed a 2.0% February weakening. A 5.5% increase (26.6% y/y) in motor vehicle & parts bookings was offset by a 38.2% falloff in aircraft & parts orders.

Orders for nondefense capital goods excluding aircraft improved 0.9% last month (11.6% y/y) as it followed a 0.8% February weakening.

In the major categories of the report, primary metals orders rose 1.2% (15.1% y/y) while fabricated metals orders strengthened 3.6% (16.6% y/y). Machinery orders rose 1.0% (9.7% y/y) while computer & electronic product orders edged 0.5% higher (10.1% y/y) following two months of decline. These increases were offset by a 1.5% falloff (+7.4% y/y) in orders for electrical equipment and appliances.

Shipments of durable goods increased 2.5% (10.0% y/y) following a 3.6% decline. Shipments of core capital goods rose 1.3% (10.4% y/y). Shipments of transportation products rebounded 4.8% (11.7% y/y) as auto and aircraft shipments improved. Shipments excluding transportation rebounded 1.5% (9.3% y/y) after and reversed February’s weakening.

Unfilled orders for durable goods improved 0.4% (-3.3% y/y) last month after a 0.9% increase. Order backlogs, excluding transportation, rose 1.2% (7.7% y/y) for a second consecutive month.

Inventories of durable goods jumped 1.0% (1.7% y/y) in March, the strongest increase since July 2018. Excluding transportation, inventories increased 0.8% (0.3% y/y) and have been rising for seven consecutive months. (…) (Haver)

But Non-def ex-air orders are up 10.1% YoY in Q1, +9.6% over Q1’19. March ‘21 is up 8.7% over March ‘19.

- Flexport: Trans-Pacific deteriorating, brace for shipping ‘tsunami’ US importers face even more extreme delays ahead as container capacity maxes out

(…) “It’s not getting better. It’s getting worse,” he told American Shipper in an interview on Monday.

“What I’m seeing is unprecedented. We are seeing a tsunami of freight,” he reported.

“For the month of May, everything on the trans-Pacific is basically sold out. We had one client who needed something loaded in May that was extremely urgent and who was ready to pay $15,000 per container. I couldn’t get it loaded — and we are a growing company that ships a lot of TEUs [twenty-foot equivalent units]. Price doesn’t always even matter anymore.” (…)

He noted that January trans-Pacific imports were up 10% versus 2019 (comparisons to 2020 numbers are skewed by COVID) and 13.5% in February, then jumped 51% in March. “So, we’re now at 1.5 times pre-pandemic levels.”

With imports far outpacing retail sales growth, he attributed volumes to inventory restocking. “The restocking is actually affecting the trade even more than growth in demand. That tells me that this will last even longer. Let’s say U.S. consumer demand slows down in Q3 and Q4. That’s not expected, but even if it does, [capacity availability and rates] shouldn’t improve quickly, simply because of the huge restocking demand.” (…)

As a result of the backlog and restocking demand, he thinks “prices will remain high and shipping will probably remain difficult for the rest of this year. And then after that, you have the peak for Chinese New Year in 2022.” (…)

“Buckle up. The month of May will be the worst people have ever seen,” he predicted. Because some shippers will have to wait in line behind the growing backlog in Asia, he expects “what’s going to happen soon is that some importers won’t even be able to get on the boat. For them, it will almost feel like trade is coming to a halt.” (…)

U.S. Home Prices Continued to Climb in February Home-price growth accelerated to new 15-year high, according to Case-Shiller index

The S&P CoreLogic Case-Shiller National Home Price Index, which measures average home prices in major metropolitan areas across the nation, rose 12% in the year that ended in February, up from an 11.2% annual rate the prior month. February marked the highest annual rate of price growth since February 2006.

The Case-Shiller 10-city index gained 11.7% over the year ended in February, compared with a 10.9% increase in January. The 20-city index rose 11.9%, after an annual gain of 11.1% in January. Price growth accelerated in 19 of the 20 cities. (…)

A separate measure of home-price growth by the Federal Housing Finance Agency also released Tuesday found a 12.2% increase in home prices in February from a year earlier, a record in data going back to 1991.

Also on Tuesday, the Commerce Department reported that the homeownership rate inched higher to 65.6% in the first quarter, up from 65.3% a year earlier and slightly down from 65.8% in the fourth quarter. For households headed by someone under 35 years old, a key source of homebuying demand, the homeownership rate rose to 38.1% from 37.3% a year earlier.

(…) According to the MBA, purchase activity is up 34% year-over-year unadjusted. (…) Activity is still above year-ago levels, but accelerating home-price growth and low inventory has led to a decline in purchase applications in four of the last five weeks. (…)

Confidence in U.S. Economy Approaches Pre-Pandemic Level Consumers’ outlook on the economy has increased for four straight months as vaccination totals rise, businesses more fully reopen

The consumer confidence index increased to 121.7 in April from a revised 109.0 in March, the Conference Board said Tuesday. Recent improvements led the index to a more than one-year high, with the indicator approaching the pre-pandemic level of 132.6 in February 2020. (…)

The present situation index, which reflects consumers’ assessment of current business and labor market conditions, surged to 139.6 in April from 110.1 in March. This improvement suggests that the economic recovery strengthened further at the beginning of the second quarter, Ms. Franco said.

The expectations index, which gauges short-term outlook for income, business and labor market conditions, also increased, albeit to a lesser degree, to 109.8 in April from 108.3 the prior month. (…)

Recent data points to an uptick in spending from higher-income households after months pulling back even though top earners weren’t eligible for the latest round of stimulus payments. Until March, the increase in spending was mainly driven by low-income consumers, he said. (…)

Haver Analytics has more:

The share of respondents planning to buy a new home held steady at 2.4%, which came after a jump from 1.0% in February. Those planning to buy a major appliance fell to 49.8% and reversed the March increase to 53.6%.

Confidence of individuals in all age brackets improved sharply to roughly twelve-month highs.

Via Axios:

Morning Consult’s “Tracking the Return to Normal” series reveals all-time highs in consumer comfort across activities including dining, entertainment, sports and more.

- 60% of the public now feels comfortable dining out, a record high for the series that began record-keeping in March 2020.

- 53% of Americans feel comfortable going on vacation, a record since tracking began in April 2020.

Progress may be stalling out, according to the data. Though Morning Consult’s surveys on vaccine skepticism have declined for four straight weeks in the United States, progress has stalled, with 34% of respondents saying they won’t get vaccinated.

- And while 46% of respondents say they are ready to go out to a restaurant now, 17% say they will not be ready for two to three months and another 12% say it will be six months or more before they are comfortable dining in a restaurant.

Biden to Propose $1.8 Trillion Families Plan, Tax Increases In a prime-time address to Congress on Wednesday, President Biden plans to lay out a $1.8 trillion proposal that includes new spending on child care, education and paid leave and extensions of some tax breaks.

(…) The proposal he plans to unveil Wednesday follows a $1.9 trillion Covid-19 relief law and comes as he is also promoting a $2.3 trillion infrastructure package that includes new spending on bridges, roads and broadband internet. (…)

The White House said the proposal includes $1 trillion in new spending over 10 years and $800 billion in tax cuts, largely extensions of breaks created or expanded in this year’s Covid-19 relief law. Mr. Biden will call for a universal preschool program for 3- and 4-year-olds and two years of tuition-free community college for all Americans, including the young immigrants known as Dreamers, who were brought to the U.S. as children and have lived in the country illegally. Those programs would be available to Americans at all income levels, officials said, and would be funded in partnership with states.

Mr. Biden’s proposal would provide money to make child care more affordable for low- and middle-income families and boost federal funding to child-care providers. And it would establish a national paid-leave program for those needing time to care for a child or loved one or to recover from illness, among other reasons. That would provide 12 weeks of leave by the 10th year of the program, and workers would receive up to $4,000 a month, with a minimum of two-thirds of wages replaced. (…)

To pay for the new programs, the administration proposes raising the top income-tax rate to 39.6% from 37%. For households making more than $1 million, Mr. Biden would also raise the top rate on capital-gains and dividends to 39.6% from 20%. Including existing payroll and investment taxes—each 3.8%—the top rates on wages and capital gains would reach 43.4%, up from 23.8%. (…)

Mr. Biden would also adjust how capital gains are taxed at death. Unrealized gains would be treated as sold and taxable, with an exemption of $1 million a person, in addition to the existing exclusion of up to $500,000 for a married couple’s primary residence. Under current law, heirs only owe capital-gains taxes on gains after the original owner’s death and only when they sell. This is separate from the estate tax, which the plan wouldn’t change. (…)

Mr. Biden would permanently extend the expanded tax credit for child care and the expanded earned-income tax credit for childless workers. He would also make the child tax credit permanently fully refundable, which means low-income households could get the money even if they don’t have earned income.

But, resisting pleas from Democrats in Congress, Mr. Biden’s plan stops short of making permanent the Covid-19 relief law’s temporary child tax credit expansion to $3,000 a child and $3,600 for those under age 6. Instead, he would extend that break through 2025. (…)

- Biden to sign executive order to raise federal minimum wage US president’s move to lift pay to $15-an-hour also ramps up pressure on businesses

EQUITY RISK PREMIUM: NOMINAL VS REAL YIELDS

In yesterday’s Market Watch:

“Stock valuations are elevated right now, and a lot of good news is priced in,” says Jeffrey Buchbinder, equity strategist at LPL Financial, to clients in a note. “However, we believe valuations are quite reasonable when considering interest rates are low and we expect inflation to remain largely contained.”

Bloomberg’s David Wilson posted this other viewpoint from Morgan Stanley:

Stock investors stand to receive too little return for the level of risk they take, according to Mike Wilson, chief U.S. equity strategist at Morgan Stanley. Wilson drew the conclusion in a report Monday that compared an earnings-based yield on the S&P 500 Index with an inflation gauge: the 10-year breakeven rate, or the gap in yield between fixed-rate and inflation-indexed Treasury notes. The resulting equity risk premium narrowed this month to 2.06 percentage points, the smallest since May 2000, according to data compiled by Bloomberg. “There’s low probability that it will” fall further, Wilson wrote.

To help you understand the difference:

Mind the gaps (Nordea):

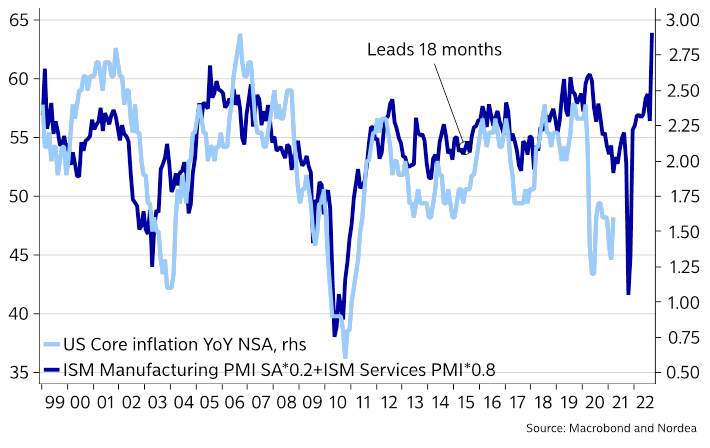

Core inflation to prove much more sticky than the Fed anticipates

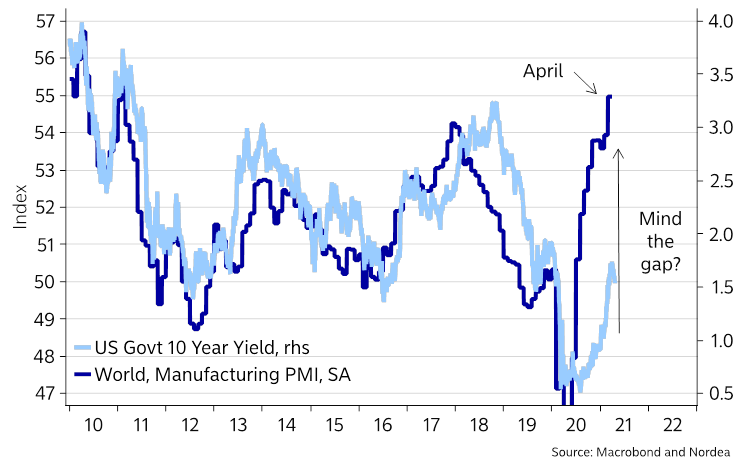

Mind the gap between long bond yields and the Global Manufacturing PMI?

Markit has more charts:

")

")

The above looks like a margin squeeze to me…

These are diffusion indices but goods prices are up big time and broadly:

")

- DoorDash shakes up fees in search for profit Leader in US food delivery market, having recorded a $312m loss on $970m of revenue in Q4’20, hopes restaurants will pay 30% commission

According to the FT, restaurants would be able to choose from three new tiers of commission — 15&, 25% or 30% — with different levels of service, depending on whether they wanted to focus on “profitability or growth”.

In today’s Globe and Mail:

Deliveries are another source of inflation. U.S.-based restaurant chain Chipotle Mexican Grill Inc. has twice raised prices on its delivery menu over the past year. And like many others, MTY has raised prices for orders placed on delivery apps, such as Uber Eats, to account for costs imposed by those parties.

“It’s mostly up to the franchisees to decide what the price difference is going to be for their stores,” Mr. Lefebvre told analysts. “We try to talk to our franchisees that a 15-per-cent price difference is reasonable, but some of them will go lower than that because we want to be more attractive to customers.”