US in technical recession

So we have technical recession in the US with 2Q GDP contracting at a 0.9% annualised rate after a 1.6% annualised drop in the first quarter. The consensus had been expecting growth of 0.4%. The main reason was a big unwind in inventories which knocked 2 percentage points off the headline growth rate while residential investment contracted 14% annualised (subtracting 0.7pp off headline growth).

We also saw weakness in business capex (non-residential fixed investment fell 0.1%) and consumer spending growth slowed to just 1%. The only good news in this report is the rebound in net trade which contributed +1.4 percentage points to the headline growth rate.

Contributions to US GDP growth

The ”real” pain is still to come

While this is a technical recession, the Fed is correct to say we aren’t in a “real” recession yet since unemployment is still falling and consumers are still spending, but it appears to be only a matter of time. We are hopeful of a decent rebound in 3Q GDP of the order 2% given ongoing improvements in the trade numbers and a rebound in the inventory contribution, but once again this will mask what is happening in domestic demand.

Consumers remain under real pressure as inflation puts the squeeze on spending power while the plunge in equity markets is another factor weighing on sentiment. We are starting to see a drift lower in some of the people movement data such as Google mobility tracking around retail and recreation, OpenTable restaurant dining numbers and also the TSA airport security check numbers. Residential investment is set to become an increasing drag on activity as housebuilders react to falling transactions and a deteriorating outlook while corporate capex is set to slow as companies worry more about recession risks.

FYI:

Taking the “noise” out (ex-trade, ex-inventory), final sales to private domestic purchasers flatlined (actually it was -0.02%). From 2010 to 2019, final sales growth averaged 2.8% annualized and never fell below 0.77%.

Taking the “noise” out (ex-trade, ex-inventory), final sales to private domestic purchasers flatlined (actually it was -0.02%). From 2010 to 2019, final sales growth averaged 2.8% annualized and never fell below 0.77%.

Goods consumption pulled down overall growth by over 1 percentage point. Services spending, however, added 1.8 percentage points.

Personal expenditures data are out today.

Revenue for the tech giant in the latest period increased by 7.2% from a year earlier to $121.2 billion. That was a hair slower than the 7.3% rise in the first quarter, which had marked Amazon’s slowest growth in about two decades.

Amazon’s loss totaled $2 billion in the quarter, compared with a profit of $7.8 billion a year ago. The loss came partly because of the company’s stake in electric-vehicle maker Rivian Automotive Inc., whose valuation has plunged this year, causing Amazon to book a pretax loss of $3.9 billion in the second quarter. Amazon’s North America division, which houses its core online retail business in its biggest market, reported a third consecutive operating loss, though it narrowed from the prior quarter.

Amazon’s net loss defied expectations for a moderate profit in the period, but its revenue grew faster than analysts anticipated, helped in part by the continued strength in cloud-computing and the services it provides to other vendors that sell on its site. Shares were up more than 13% in after-hours trading, hitting their highest point in about three months—though still down sharply from the start of 2022. (…)

“I don’t think you’ll see us hiring at the same pace we did in the last year or the last few years,” he said, but added that the company is still committed to hiring engineering positions, and in its cloud-computing and advertising divisions.

Amazon’s number of employees—which had more than doubled during the pandemic—slid about 6% during the second quarter to 1.52 million.

Mr. Olsavsky also said Amazon has slowed plans to expand its operations through next year, and plans to shift capital expenditures to cloud-computing and away from the company’s retail business. (…)

Revenue for Amazon Web Services, the largest cloud-computing company by market share, grew 33% to $19.7 billion in the second quarter.

Amazon’s advertising business, for which the company recently began breaking out financial data, grew 18% to $8.8 billion in the quarter.

The company said it expects its operating income for the third quarter to be between $0 and $3.5 billion, compared with $4.9 billion in third quarter 2021.

Jessica Lessin at The Information:

Amazon Web Services may be the jewel in Amazon’s crown—but at the moment it is practically the entire crown. Consider this: Without the $5.72 billion in operating income the cloud business contributed to the company’s June quarter, Amazon would have posted a $2.4 billion operating loss. AWS is what’s keeping Amazon from looking like another money-losing internet retailer during the current online shopping slump.

On Thursday, the company revealed that the well-publicized overstaffing and overbuilding issues that plagued its first quarter continued into the second quarter, leading to $4 billion in additional costs related to excess warehouse capacity and workforce inefficiencies. What’s more, much like Jeff Bezos’ jabs at the White House, those costs aren’t going anywhere soon. Amazon expects overcapacity costs of between $2.5 and $3 billion next quarter, CFO Brian Olsavsky told reporters in a call. (…)

Online store sales stagnated during the second quarter, barely budging from the beginning of the year and decreasing 4% from the year-ago quarter to $51 billion. (…)

- Cardboard Boxes Pile Up as Inflation Dents Online Spending

- Best Buy cuts its outlook, joining other retailers as inflation pressures shoppers

The consumer electronics retailer said it now expects same-store sales to decline about 13% for the current three-month period, which ends Saturday. That’s lower than what Best Buy said in May, when it predicted comparable sales would be roughly in line with the 8% decline in the first quarter.

For the 12-month period that ends in late January, Best Buy said it expects same-store sales to decline around 11% compared with the drop of between 3% and 6% that it forecast in May. (…)

With Wednesday’s announcement, Best Buy joins a growing list of retailers including Gap, Adidas, Kohl’s, Target and Walmart that have warned of lower sales or profits as consumers feel pinched by inflation or shift spending to services, such as travel and dining out, rather than goods.

Yet Best Buy said its inventory levels at the end of the second quarter will be approximately flat compared with the year-earlier period. That’s a notable difference from Walmart, Target and Gap, which have a glut of unwanted inventory weighing on profit margins. (…)

Jobless Claims Hold Near Highest Level of the Year New applications for unemployment benefits, a proxy for layoffs, fell to 256,000 last week, near the highest level of the year and a sign that the tight labor market is loosening.

Initial jobless claims, a proxy for layoffs, fell 5,000 to a seasonally adjusted 256,000 in the week ended July 23 from the prior week’s upwardly revised level, the Labor Department said Thursday. The prior week’s reading was revised up by 10,000 and was the highest level of claims since November.

Last week’s claims stood above the 2019 prepandemic weekly average of 218,000, but remained at a level generally consistent with a solid labor market. The four-week moving average for claims, which smooths weekly volatility, inched up to 249,250 last week, an increase of 6,250 from the previous week’s revised average. (…)

This chart shows unemployment claims with the scale set to reflect levels between 2014 and 2019. The horizontal line is the average for that period. The low in claims was in March; they are up 79k or 46% since.

In his Wednesday presser, Mr. Powell blamed seasonal issues for the recent sharp rise in claims but Bespoke disagrees:

(…) jobless claims have been roughly following standard historical seasonal patterns this year. July typically sees a temporary seasonal spike higher, but as we noted last week, that seasonal peak appears to have been put in place a bit later than usual which is rare but not exactly an unprecedented occurrence. While claims will likely get some seasonal tailwinds in the coming weeks (including this week of the year as claims have fallen around 90% of the time historically), the actual level of claims for the current week of the year is now well above comparable weeks for the few years prior to the pandemic. In other words, before or after seasonal adjustment, claims have come off their strongest levels and revisions have not exactly made things any better. (…)

BTW, the BLS did revise last week’s number…by a sizeable +10k…

BTW #2:

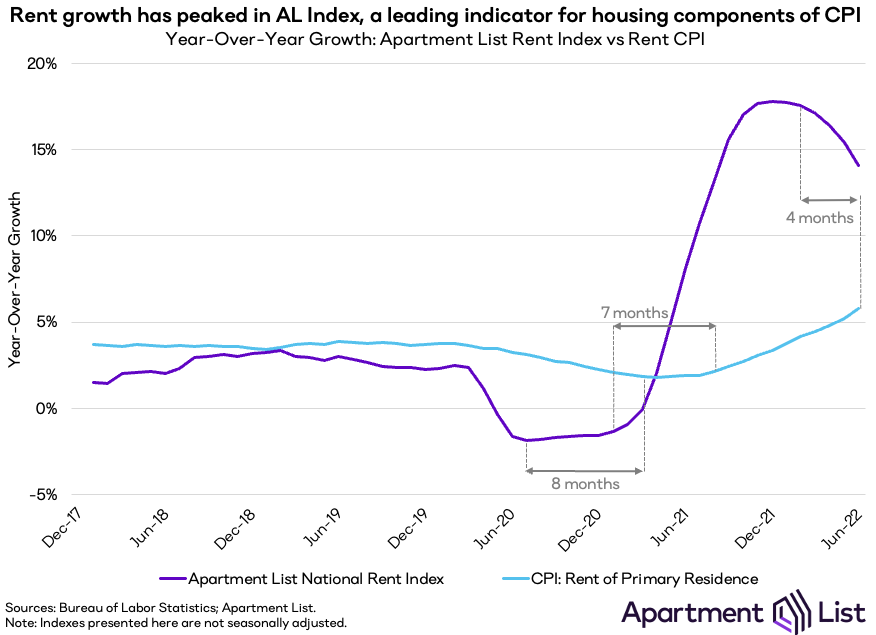

Toronto Apartment Rents Soar 20% to Record Levels With Market Tightening The double-digit price gains reflect a decline in the number of leased listings, which are down 11% from a year ago, according to the report.

-

New York and Singapore tied for the biggest rent increases in the first half as prospective tenants returned to cities.

-

In the USA: “But YoY rent growth is already falling according to our index, and we expect it will peak in the CPI sometime this fall.” (@chris_salviati)

Euro-Zone Inflation Hits Record, Backing Calls for Larger Hikes

Consumer prices jumped 8.9% from a year earlier in July — up from 8.6% last month and driven once again by soaring energy and food costs. The number overshot the expectations of economists surveyed by Bloomberg, who saw a gain of 8.7%. (…)

Euro Area: Q2 GDP Surprises Significantly to the Upside

The first estimate of Euro area Q2 GDP showed growth of 0.7%qoq, significantly above consensus expectations, reflecting a post-Omicron rebound amid an easing of virus-related restrictions. Overall, Euro area real GDP is now 1.5% above its pre-pandemic level and country-level back-data revisions suggest scope for further upward revisions to the level of GDP.

Looking ahead, however, we expect growth to moderate sharply as industrial activity has already softened notably and recent activity indicators suggest that the post-Omicron bounce in services is past its peak. Accordingly, we continue to forecast below-consensus growth in H2 and look for a technical recession in coming quarters in the Euro area. That said, we do not think a recession is inevitable given tailwinds to growth in the form of continued services growth in Southern Europe, ongoing fiscal support, and unwind of excess savings accumulated during the pandemic. (Goldman Sachs)

Chinese Leaders Indicate Country Is Likely to Miss Economic Growth Targets Politburo urges stronger provinces to strive to meet their annual growth targets

(…) China’s Politburo, the Communist Party’s top policy-making body, said in a statement Thursday following its quarterly economic meeting that it would aim to keep the economy running within “a reasonable range” in the second half of the year. It also urged stronger provinces to strive to meet their annual growth targets—an implicit acknowledgment that others would miss their benchmarks. (…)

In contrast to after its previous economic meeting in April, Thursday’s Politburo statement didn’t explicitly mention the 5.5% growth target, saying only that leaders would “strive to achieve the best results possible” and keep the economy within “a reasonable range.” (…)

While the Politburo called Thursday for local governments to deploy all of this year’s funds raised by issuance of special bonds, it didn’t announce any new bond quotas or pull forward bond quotas allotted for next year, as many economists had expected—suggesting that Beijing isn’t seeking to dramatically stimulate growth. As of the midway point of the year, Chinese local governments had already issued 93% of this year’s allocation of special bonds, according to the Finance Ministry.

Still, the Politburo said Thursday that it would introduce policies to expand domestic demand and extend more loans to companies forced to suspend production by Covid-19 outbreaks.

The Politburo also directly addressed two intertwined challenges that it is facing: A mortgage strike among home buyers that has raised concerns about the real-estate sector and the rural banking system, which relies heavily on property sales.

In response, China’s top leaders said they would work to resolve risk in the rural banking system and vowed to stabilize China’s property market. The Politburo said local governments should take direct responsibility for securing the deliveries of unfinished homes and protecting people’s livelihoods, while supporting organic demand for housing. (…)

The World’s Economic Growth Engines Slide Into Recession

Monthly research for the Global Sales Managers Index covers China, the USA and India. Together over the past decade, these three countries accounted for almost 60% of global economic growth. None are proving immune to the serious problems now weighing heavily on global economic activity.

(…) three out of four of the growth related Sales Managers Indexes are at near two year lows. The overall Sales Managers Index has tipped into recession, in July registering well below the crucial 50 “no change” level. Staffing levels remain a long way below those seen a year ago. Only Business confidence (that business activity will improve over the next few months) remains fractionally over the 50 level, but also at a 24 month low, and still falling month on month.

The (only) good news is that the Price Index fell significantly in July, suggesting strongly that supply problems may be slowly resolving as business adjusts to the severe problems faced over the Covid years..

USA The Strong Dollar Is Wreaking Havoc Globally — And It’s Just Getting Started

The Strong Dollar Is Wreaking Havoc Globally — And It’s Just Getting Started

(…) The dollar, the currency that powers global trade, is on a tear that has few parallels in modern history. Its ascent is the result primarily of the Federal Reserve’s aggressive rate-hiking — it raised by another 75 basis points on Wednesday — and has left a trail of devastation: Driving up the cost of food imports and deepening poverty across much of the world; fueling a debt default and toppling a government in Sri Lanka; and heaping losses on stock and bond investors in financial capitals everywhere. (…)

“There is simply no alternative to the dollar no matter where you look and it’s pummeling everything else as a result — economies, other currencies, corporate earnings.”

The US currency’s rapid ascent is being felt in daily life around the world because it’s the lubricant for global commerce — roughly 40% of the $28.5 trillion in annual global trade is priced in greenbacks. Its relentless rise risks creating a self-sustaining “doom loop.” (…)

- The Strong U.S. Dollar Is Extending Pain in Emerging-Markets Currencies With the dollar still rallying, currencies in Hungary, Poland and elsewhere are hurting

(…) The extended losses are another example of how the dollar’s strength is rippling through emerging-markets currencies and pressuring central banks across the globe to increase rates—even at the cost of a recession.

“Trouble is coming in emerging markets,” said Megan Greene, global economist and senior fellow at the Harvard Kennedy School, pointing toward Sri Lanka’s sovereign-debt crisis and drained foreign-exchange reserves. “It’s a familiar story in emerging markets and a sneak peek of what’s to come.” (…)

Goldman Sachs Group Inc. strategists said, “cracks are appearing” in emerging-market currencies after more than a year of beating returns against a basket of nine major currencies, including the Swiss franc and Canadian dollar. (…)

“Following the Covid shock, all major central banks were moving in the same direction, but no longer.” (…)

EARNINGS WATCH

We now have 245 companies in (not counting yesterday’s), a 76% beat rate and a +5.0% surprise factor. These 182 companies reported aggregate earnings up 4.6% YoY on a 11.3% revenue growth rate.

Estimates are for Q2 EPS to rise 7.6%, -1.9% ex-Energy. Revenues: +12.1%, ex-E + 7.4%. Q3e: +9.0%, +2.7% ex-Energy. Q3 revenues: +10.8%, ex-E +7.2%. Sower GDP growth, hopefully slower inflation, but same revenue growth rate!

Retail Army: back with a vengeance

Retail traders net bought $4.3B of cash equities this past week, 0.8 standard deviations above 1Y average. This is the first time weekly retail net buying exceeded annual average since early April. At the single stock level, retail traders were net buyers of Technology (+1.4z) and Growth (+1.5z). In options space, retail traders net bought $688MM of delta. (The Market Ear)

JPM Retail Radar

-

From CMG Wealth: