Manufacturing PMIs

Note: China and Japan PMIs were out last Friday.

USA: Strongest improvement in operating conditions on record amid marked uptick in client demand

April PMITM data from IHS Markit indicated a robust improvement in the health of the U.S. manufacturing sector, and the steepest since data collection began in May 2007. Overall growth was supported by quicker expansions in output and new orders, with the latter rising at the sharpest pace since April 2010. The headline index was also pushed higher by unprecedented supplier delivery delays (ordinarily a sign of improvement in operating conditions). Raw material shortages also led to the fastest rise in cost burdens since July 2008, with firms seeking to pass on supplier price hikes through marked upticks in output charges.

Meanwhile, business confidence moderated, amid concerns regarding supply chain disruptions and strains on future production capacity.

The seasonally adjusted IHS Markit U.S. Manufacturing Purchasing Managers’ Index™ (PMI™) posted 60.5 in April, up from 59.1 in March and broadly in line with the earlier ‘flash’ estimate of 60.6. The PMI figure was the highest since data collection for the series began in May 2007 and signalled a marked expansion.

Contributing to the greater headline figure was a sharp and faster upturn in production across the manufacturing sector. Output growth was commonly linked to a stronger rise in new orders, although some companies continued to highlight pressure on capacity following raw material shortages.

New orders increased markedly in April, with the rate of expansion accelerating to the fastest for 11 years. Firms noted that the upturn was due to stronger client demand, with some companies mentioning that customers were placing larger orders amid substantial supplier delivery delays. At the same time, new export orders expanded at the second-quickest rate on record as lockdown restrictions eased in key export markets.

Pressure on capacity meanwhile persisted, as backlogs of work rose at the second-steepest rate yet recorded by the survey. Subsequently, employment increased strongly and at the second-fastest pace since December 2017.

April data signalled another marked monthly deterioration in vendor performance across the goods-producing sector, with lead times lengthening to the greatest extent on record. Alongside raw material shortages and pressure on supplier capacity, firms linked delays to ongoing disruption to transportation, including port congestion.

Worst affected were consumer-facing firms, where a lack of inputs has caused production to fall below order book growth to a record extent in over the past two

months as household spending leapt higher.Input costs rose rapidly in April, with the rate of inflation quickening to the sharpest since July 2008. The increase was widely attributed to material shortages and greater transportation costs.

Firms sought to pass on higher costs to clients through a further rise in output charges in April. The rate of charge inflation eased slightly from March, but was the second-fastest on record.

Firms expanded their buying activity at the steepest pace since August 2014. As well as reports of increased input buying due to greater production requirements, some firms also noted efforts to build stocks. Consequently, firms registered a modest expansion in pre-production inventories. Stocks of finished goods fell, however, as firms often reported that demand exceeded current production.

Finally, business confidence moderated in April, with optimism slipping to a three-month low. Expectations were weighed down by concerns regarding supply chain disruptions. (Markit)

Canada: Robust growth in manufacturing production sustained in April

April data signalled another robust overall expansion in operating conditions at the Canadian manufacturing sector, with the latest result extending the period of growth to ten consecutive months. Despite a surge in COVID-19 cases and a series of tightening restrictions, output and new orders rose sharply, although the rates of growth moderated from those seen in March. Firms responded to the sustained increase in demand by adding to their workforces, however capacity pressures remained evident with backlogs rising markedly. Meanwhile, port congestion and pandemic restrictions led to another lengthening in supplier delivery times. To guard against future delays firms added to their input stocks at a near-record pace.

Turing to prices, higher raw material costs and shortages in the supply of inputs added to costs burdens. Firms consequently raised their selling charges, with the rate of output price inflation the sharpest in the ten-and-a-half year history of the survey.

The headline seasonally adjusted IHS Markit Canada Manufacturing Purchasing Managers’ Index® (PMI®) registered 57.2 in April, down from 58.5 in March, to signal the third-strongest growth in operating conditions in the survey to date, which began in October 2010.

Canadian manufactures recorded another solid upturn in their production volumes, although the rate of growth moderated from March’s recent peak. Survey respondents commented on supportive demand conditions and greater willingness to spend among clients, particularly those in the construction sector.

Similarly, new orders rose sharply, albeit at a slightly softer pace than that seen in the previous survey period. Panellists widely commented on greater demand from both domestic and foreign markets (mainly the US).

Goods producers in Canada lifted headcount numbers for the tenth month in succession in April. The rate of job creation softened from that in the previous survey period but was still historically strong. Despite this, signs of capacity pressures continued to emerge with incomplete work now accumulating in each month since last August. Panel comments suggested material shortages were the key driver of rising backlogs.

Amid reports of raw material shortages, (particularly resin and metals) average lead times lengthened in April. Transportation bottlenecks were also blamed for the deterioration in vendor performance. In efforts to reduce delays, firms added to their pre-production inventories, with the rate of growth the second-strongest in the series to date.

Raw material scarcity and supply-chain disruption continued to exert upward pressure on firms’ costs burdens, with input price inflation reaching a 32-month high. Higher expenses were passed on to clients with the overall rate of selling price inflation climbing to a survey peak.

Amid hopes of increased investments, and greater client demand manufacturers were confident of a rise in production over the coming 12 months. The level of positive sentiment eased to broadly in line with it’s long-run average, however, as some firms were concerned about the longer-term effects of COVID-19.

Eurozone manufacturing PMI hits fresh survey record high in April

The eurozone manufacturing economy registered another stellar performance in April, with operating conditions improving at a rate that surpassed March’s survey record. This was signalled by the seasonally adjusted headline PMI® which improved to 62.9, up from 62.5 in March and its highest ever recorded level (survey data have been available since June 1997). It was also the tenth successive month that the index has posted above the 50.0 no-change mark.

Growth was again broad-based per market group, with both the investment and intermediate goods categories registering considerable gains. Moreover, the improvement seen in investment goods was the strongest ever recorded. Consumer goods meanwhile saw a marked improvement in operating conditions, though growth lagged the two other categories covered by the survey.

The Netherlands led the way in terms of absolute PMI readings, posting a new record for that survey, followed by Germany which experienced a slight fall in its headline index since the previous month. Growth momentum was nonetheless seen across most nations, with Italy and Austria also posting survey highs in April.

Growth rates for both aggregate manufacturing output and new orders remained close to March’s survey records as firms reported rising market confidence. New order books expanded sharply amid evidence that both manufacturers and clients are anticipating a sharp rise in activity over the coming months, as restrictions related to COVID-19 are relaxed. Moreover, growth came from both domestic and international sources: new export orders rose again at a considerable pace in April.

Production growth was limited to some degree by capacity constraints, in turn partly the result of stretched supply chains. April saw average lead times for the delivery of inputs deteriorate to a degree unsurpassed in the survey’s history. A mismatch of supply and demand, allied with ongoing challenges in transportation networks, especially for sea freight, were widely reported as causal factors.

Product shortages subsequently helped to drive input prices up at a rate beaten only once in the survey history (February 2011). Chemicals, metals, and plastics were amongst those inputs reported to be up in price and this led, alongside growing confidence in the outlook, to companies raising their own charges to the strongest degree in over 18 years of data availability.

Fearful of ongoing shortages in supply, and faced with rising output and order requirements, manufacturers increased their purchasing activity at an unprecedented rate. Firms also chose to utilise their inventories of purchases wherever possible, with stocks being depleted for a twenty-seventh successive month. A drop in stocks of finished goods was also reported as firms struggled to meet rising order book requirements. The decline in inventories was the greatest since December 2009.

With new orders continuing to rise sharply, and production in part constrained by supply-side delays, capacity came under increasing pressure. Backlogs of work rose again at a survey record pace and have now risen for nine months in succession.

In response, companies added to their workforce numbers, increasing payroll numbers for a third successive month. The net gain was also the best since February 2018 with all nations registering higher employment numbers. Growth was strongest in Austria and the Netherlands.

Recruitment was in part influenced by positive projections for the coming 12 months. According to the latest data, manufacturers were at their most optimistic in nearly nine years of data availability amid hopes that successful vaccination programmes will lead to a strong uplift in economic activity.

“Encouragement comes from the sharp increase in employment and investment in machinery and equipment signalled by the survey, which suggests firms are scaling up capacity to meet resurgent demand. This should help bring supply and demand more into line, taking some pressure off prices. But this will inevitably take time.”

The J.P. Morgan Global Manufacturing PMI reached 55.8 in April from 55.0 in March, its best reading since April 2010. Total new orders and new export business both rose at the quickest rates since May 2010.

Cost inflationary pressures remained strong at the start of the second quarter, with average producer prices rising to the greatest extent in over a decade. Manufacturers passed part of this increase on to customers in the form of higher selling prices. Subsequently, output charges rose at the quickest pace since data on this price measure were first compiled in October 2009.

- Bidenomics Takes Root in Europe’s Economically Fragile South Italy, Spain and Greece plan once-in-a-generation investments to revamp their economies by borrowing big. If it doesn’t work, a mountain of debt could revive eurozone tensions.

It is clear from the manufacturing PMIs that companies are fighting the supply issues and price increases by hoarding stuff, fueling the uptrends. Bloomberg’s Joe Weisenthal today:

Yesterday Tracy Alloway and I talked to Ryan Petersen, the CEO of the firm Flexport, about the ongoing logistical havoc facing companies all over the world right now. The episode will be out next week, but one thing he confirmed is that at least from his perspective, there are still no signs of the strains ebbing. There are still delays and bottlenecks basically everywhere you look across supply chains. (…)

At the core of the issue is simply the fact that the global trade system wasn’t built for a period during which there would be such a spike in demand for physical goods, as the pandemic caused a shift in consumption away from services.

Ultimately Petersen doesn’t see a true normalization until we get a further reopening and demand for goods starts to meaningfully downshift again. The good news, theoretically, is that some of the strains we’re seeing could actually ease once things ostensibly normalize.

PENT UP VS SPENT UP

David Rosenberg is the most vocal consumer bear but he seems to be softening with the more recent data:

With the weather improved, the vaccinations gaining momentum, the economy re-opening and jobs coming back, along with the gifts from Washington, the spending spree in March was broadly based and impressive. What was most interesting, was the relentless buying of merchandise goods even as the economy re-opened. No wonder there is a shortage of material —the further build-up of durable goods assets on household balance sheets was truly incredible —durable goods expenditure bounced 10.3% on the month and +44% on a YoY basis.

Is the FOMC also beginning to soften its stance?…

Fed’s Williams: Fed Far From Achieving Job, Inflation Goals Federal Reserve Bank of New York President John Williams said Monday that while the U.S. economy is likely to have a very strong year ahead, this welcome turn of events doesn’t suggest the central bank faces any imminent need to pull back on its aggressive levels of monetary policy support.

(…) In an appearance on CNBC Monday, Federal Reserve Bank of Richmond President Thomas Barkin said one of his key metrics for knowing when to pare back bond buying is the employment to population ratio, as opposed the unemployment rate, which many, including some Fed officials, believe understates the true level of joblessness in the nation.

Mr. Barkin said the employment-to-population ratio has seen only “modest progress” on recovering what was lost over the pandemic, and further improvement on this front will help drive his decision on when it is time to pull back on bond buying. (…)

![]() But last Friday, Dallas Fed President Robert Kaplan publicly stated he wanted to start having a conversation over a “taper”.

But last Friday, Dallas Fed President Robert Kaplan publicly stated he wanted to start having a conversation over a “taper”.

But who’s afraid of inflation?

Corporate America Rides Wave of Inflation to Record Profits

(…) Faced with rising prices for everything from lumber to oil to labor and computer chips, chief executive officers have cut costs and boosted prices for their products. The strategy appears to be working, with first-quarter income from S&P 500 companies jumping five times as fast as sales, data compiled by Bloomberg Intelligence show. (…)

The so useful Ed Yardeni has some great charts on these trends:

- Prices paid vs received:

- And the spread, clearly suggesting a margin squeeze, recently totally offset by the surge in revenues. The 265 S&P 500 companies that have reported Q1 so far have shown revenues up 10.8% YoY.

- Here’s the link to PPI Final Demand:

- And the flow through CPI Goods inflation. Note that CPI-Core Goods inflation is +1.7% in March and, surprisingly, unchanged QoQ in Q1’21. To be monitored.

- How about that relationship from BofA?

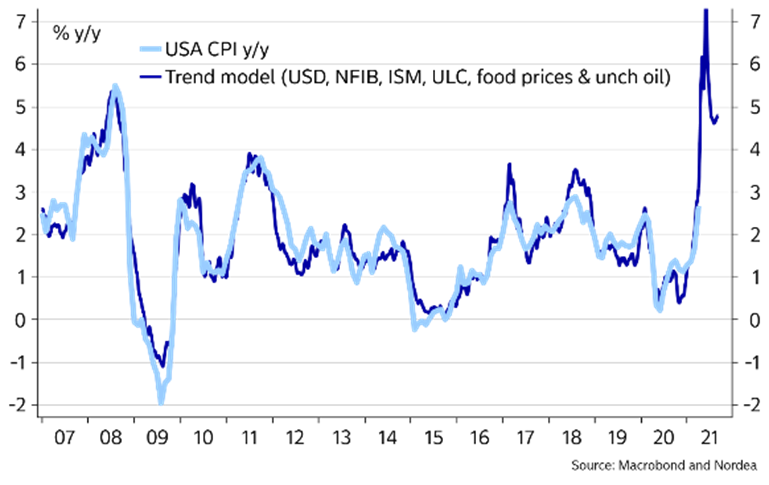

- In closing, here’s Nordea’s scary chart:

Our trend model that, among other variables, includes the USD, NFIB, ISM prices and food prices hints of >7% this summer. It looks too bad to be true, but if everything is in a bottle-neck at the same time, then price pressures can turn fairly violent. We know how e.g. lumber, oil and food prices have risen markedly, and there is anecdotal evidence of substantial bottle-necks in other sectors as well. It will be tough to explain such inflation readings away for Powell, but he will probably do his best to find arbitrary transitory explanations.

Our inflation model is summoning its inner doom monger

More on inflation:

America is running low on chicken. Blame covid-19, a sandwich craze and huge appetite for wings. “What we need,” the official told WSOC-TV, “is a four-winged chicken.”

Coming soon: fake chicken!

Speaking of chickens…

SENTIMENT WATCH

Es gibt keine Alternative.

This is TINA in German (according to Google ![]() ).

).

Cautious German Savers Brave the Stock Market U.S. stocks such as Tesla, Apple and GameStop are attracting investors, as negative bank rates prompt risk-averse Germans to shift their savings

(…) More Germans entered the stock market for the first time during the pandemic than in any stretch since the dot-com boom. Deutsches Aktieninstitut, a finance-industry association, estimates that 2.7 million people in Germany started owning shares directly or through funds last year, boosting the investor total to 12.4 million, up 28% from 2019.

Still, less than 18% of Germans 14 years of age and older hold shares, equity funds, or exchange-traded funds. In the U.S., 53% of families hold stocks directly or indirectly, according to the Federal Reserve. If more savers in Europe’s largest economy shift to stocks, that could ripple through the market.

Germans have long resisted investing directly in stocks and other risky assets, preferring the safety of guaranteed bank deposits. Most Germans also rely on generous state pensions to fund retirements. Some were burned by a similar surge into shares before the dot-com bust.

But the punishing reality of negative rates has changed the equation. Also playing a role in getting Germans to invest: increased savings during the coronavirus pandemic, free time resulting from lockdowns and a young population excited about the boom in U.S. tech stocks.

“My new buyers are U.S.-stock buyers” going after Amazon.com Inc., Tesla Inc. TSLA -3.46% and other tech giants, said Erik Podzuweit, founder and co-chief executive officer at Scalable Capital, a Munich-based online broker. (…)

“The reality is that there aren’t better alternatives for your money out there,” Mr. Hösle said. (…)

Mr. Schacht, the clothing-shop owner, put his savings with FAM Frankfurt Asset Management AG, a boutique firm. Ottmar Wolf, FAM’s co-founder and chief investment officer, said assets under management at the two-year-old firm grew 25% over the past 12 months as wealthy and retail clients fled negative rates on their bank accounts.

“In my 22-year career, I have never seen anything like this,” Mr. Wolf said.

Leon Cooperman on CNBC on Friday: “I am a fully invested bear”.

Lee is one of a very few bears left:

Here’s the AAII data:

There is even a paucity of cautious bulls. Very few people now believe there is a risk of a correction.

No more bears, virtually no more chickens! A brave world. Eine mutige Welt, for our German friends.

Treasury Expects to Borrow $1.3 Trillion in Second Half of Fiscal 2021

That would bring total borrowing for the fiscal year ending Sept. 30 to $2.3 trillion, compared with $4 trillion in the last fiscal year, when the pandemic plunged the U.S. into a recession that drove deficits to record highs.

The Treasury estimated the government would borrow $463 billion during the current quarter, nearly five times as much as the $95 billion it estimated previously, before Congress passed the $1.9 trillion relief bill. Still, that is a fraction of what the U.S. borrowed during the same period last year, from April through June, when emergency spending to combat the pandemic and weak tax revenues sent deficits soaring and pushed total borrowing to $2.7 trillion.

The Treasury also estimated net marketable borrowing would total $821 billion from July through September, assuming Congress agrees to suspend the federal borrowing limit on Aug. 1. (…)

Federal debt is now on track to reach 108% of gross domestic product, according to estimates from the Committee for a Responsible Federal Budget, higher than it was after World War II. (…)

China Tensions Spill Over as Europe Moves Toward Biden’s Side

(…) The multiple signs of strain suggest Europe’s biggest players are moving closer to the views of President Joe Biden’s administration in its standoff with China. As Secretary of State Antony Blinken holds talks in London this week with his Group of Seven counterparts, a Europe more aligned with Washington would signal some repair to the damage done to transatlantic ties by the Trump administration, with implications for trade, tariffs and access to technology. (…)

Economic ties remain paramount since China is the EU’s biggest trading partner, with a total volume of some $686 billion in 2020 outstripping U.S.-China trade of $572 billion. Yet now even the Netherlands, which is among China’s top 10 trading partners, is growing more wary, protecting its high-tech companies from takeover and enacting a dedicated China strategy. According to the Chinese official, the U.S. has forced the EU to take sides. (…)

The shift in Europe has not been lost on Washington. A Biden administration official said there’s been a sea change in European thinking, coming on board with the U.S. stance on China. There’s been real evolution in Germany too, the official said.

- Chinese banks accused of funding deforestation around world Report undermines Beijing’s drive to be seen as global leader in climate change campaign

COVID-19

It’s Not Just India. New Virus Waves Hit Developing Countries

Nations ranging from Laos to Thailand in Southeast Asia, and those bordering India such as Bhutan and Nepal, have been reporting significant surges in infections in the past few weeks. The increase is mainly because of more contagious virus variants, though complacency and lack of resources to contain the spread have also been cited as reasons. (…)

Although nowhere close to India’s population or flare-up in scope, the reported spikes in these handful of nations have been far steeper, signaling the potential dangers of an uncontrolled spread. The resurgence — and first-time outbreaks in some places that largely avoided the scourge last year — heightens the urgency of delivering vaccine supplies to poorer, less influential countries and averting a protracted pandemic. (…)

States Roll Back Restrictions as Covid-19 Cases Decline With more than 40% of adults fully vaccinated and the daily number of new Covid-19 cases declining, governors across the U.S. are broadly rolling back restrictions implemented during the pandemic.

On Monday, governors from New York and New Jersey said their states would on May 19 lift most capacity restrictions at places of business.

Neighboring Connecticut previously ended many capacity restrictions and announced in April that it would end all restrictions on businesses beginning May 19, except for indoor masking requirements. (…)

According to recent data from the Kaiser Family Foundation, 27 states have fully reopened, up from 22 on March 15. (…)

From MIT Tech Review:

The good news is that there isn’t a lot to worry about—not least because these breakthroughs are vanishingly rare. The CDC has received a smidgen over 9,000 reports of covid infections among more than 95 million people who are fully vaccinated. That means only one in every 10,000 vaccinated people have reported catching SARS-CoV-2. (…)

Even when infections do happen, they appear to be less dangerous:

“New studies published last week show that even in high-risk settings like nursing homes, these breakthrough infections seem to be rare,” she writes. “And when infections do occur, symptoms tend to be nonexistent or mild. What’s more, vaccinated individuals who become infected have lower viral loads than unvaccinated people—meaning they are less likely to transmit the virus.”

Since vaccines prepare our immune systems to battle a covid infection, our bodies are also less susceptible to it: the cycle of infection and transmission is suppressed.

This doesn’t mean that we should let our guard down completely, however. There’s the possibility that variants could develop which allow covid to sidestep those immune responses: tweaks to the virus that make it just different enough to slide past the body’s defenses. That evolution is known as immune escape.Still, there’s good reason for optimism. As Cassandra writes:

“It’s important to track breakthrough infections to look for unexpected changes. A rising number of infections in vaccinated people might mean waning immunity or the emergence of a new variant that can dodge the immune response. The vaccines might need to be tweaked, and we might need booster shots. But over time, ‘our bodies will develop a more complete immune response,’ says Stephen Kissler, an epidemiologist at Harvard’s T.H. Chan School of Public Health. ‘And even if we do get reinfected, we’ll be protected from the most severe outcomes. In the long term, the outlook is good.’”