Note: I started blogging January 3, 2009. I do not recall having posted such a broadly frightening post. Inflation, China, commodities, currencies, cryptos, valuations…![]()

Inflation Slipped in April, but Upward Pressures Remain U.S. inflation eased slightly in April, dropping for the first time in eight months as energy prices moderated.

U.S. inflation edged down to an 8.3% annual rate in April but remained close to the fastest pace in four decades as the economy continued to face upward price pressures.

The Labor Department’s consumer-price index reading last month marked the first drop for inflation in eight months, down from an 8.5% annual rate in March. The decline came primarily from a slight easing in April gasoline prices, which have since reached a new high. Broadly, the report offered little evidence that inflation was cooling. (…)

Airline fares surged 18.6% in April from a month earlier, the fastest rise on record. The cost of full-service restaurant dining rose 0.9% from March, the biggest gain since last October. (…)

Used car and truck prices were up 22.7% on the year in April, down from a 35.3% rise in March. But new vehicle prices were up 13.2% from a year ago in April, the largest 12-month increase since 1949. (…)

A steady pickup in housing costs, which account for nearly one-third of the CPI, is also adding to inflationary pressure. Both tenant rent and so-called owners’ equivalent rent, which estimates what homeowners would pay each month to rent their own home, rose 4.8% from a year earlier, a pace last seen in the late 1980s and early 1990s. (…)

Core CPI was up 0.57% MoM after 0.32% in March. Two-month average: 0.45% or 5.4% annualized. The previous 2 months averaged 0.55%, 6.5% a.r.. Trending down, very slowly. We are far from the late 2020s.

In April, MoM, rent +0.56%, owners’ equivalent rent +0.45%. Core services prices overall rose at their fastest pace since 1990 (+0.72%).

- Manhattan Apartment Rents Hit Record With Intense Summer Ahead With vacancies tight and the market entering its busiest season, costs are predicted to rise even higher.

An analysis of inflation data needs to take two different perspectives: inflationary trends from a financial market viewpoint (interest rates, equity valuations) and inflationary pressures from an economic viewpoint (consumer squeeze, recession risk). The former focuses on core CPI while the latter must include the important food and energy components given their impact on discretionary spending power.

This ING chart tackles both concerns with none particularly encouraging.

- Core goods inflation (orange) is cresting and could well eventually become negligible like before but core services inflation (yellow) is 50% higher than before and trending up. Core services prices jumped 0.7% in April, are up 6.7% a.r. ytd and 7.5% a.r. in the last 3 months. Shelter prices have been rising at a 6% a.r. in the last 3 months. The fundamental trend in inflation remains up as rising wages filter through services prices.

Contributions to annual US inflation

Source: Macrobond, ING

No reason to expect an imminent turn in rent components

-

Food and energy prices are adding 3%+ to core inflation with no signs of easing meaningfully. Food-at-home inflation was 10.8% YoY in April after having jumped 15.4% a.r. in the first 4 months of the year. Energy inflation is 30.3% YoY, in spite of -2.7% MoM in April, likely to reverse itself in May since gasoline prices are back to their February peak. “Essentials Prices” (food, energy and shelter) are up 8.6% YoY.

INFLATION ON ESSENTIALS (YoY)

INFLATION ON ESSENTIALS (MoM)

Greg Ip:

Inflation Is Headed Lower—but Maybe Not Low Enough While supply disruptions are subsiding, without slower demand, inflation will still be too high for the Fed’s comfort to stop raising interest rates.

(…) Bottom-up analysis of the consumer-price index’s components, inflation-linked bond yields, and wage behavior all point toward inflation settling at roughly 4%. (…) But there are good reasons it will stay around 4% or even drift higher. (…)

The Korean War analogy is comforting because while the Fed did tighten monetary policy, it avoided a recession. Inflation shot from 2% in mid-1950 to 9.6% the following April, and was back below 1% by December 1952.

In 1973, the Arab oil embargo hit an economy already trying to cope with soaring food prices and strong demand. As an analogy for the present, this episode is a lot less comforting than 1951: Inflation peaked at 12.3% in 1974, and the Fed raised interest rates sharply, triggering a deep recession. Even so, inflation only fell back to 5% in 1976—then headed higher. (…)

And yet looking forward, the supply disruptions that have fueled so much of the rise in inflation are likely to get better, not worse. Gasoline prices hit another record this week but aren’t likely to rise much more since oil has stabilized around $100 per barrel. The queue of container ships waiting off the coast of California has shrunk by more than half, and freight rates have plummeted. About three quarters of China’s top 100 cities by gross domestic product have now either loosened restrictions to pre-Omicron levels or removed them entirely, according to Ernan Cui of the research firm Gavekal Dragonomics. One sign that goods shortages are subsiding is that manufacturing, retail and wholesale inventories, which plummeted 5% between the start of the pandemic and last September, are up 3% since.

(…) annual wage growth has accelerated from about 3.5% before the pandemic to between 5% and 6%. That is consistent with inflation of 4% if productivity maintains its recent, tepid pace, or 3% if productivity perks up. For the Fed to feel confident inflation is headed below 3%, it needs to see lower wage growth, which generally requires slower economic growth and higher unemployment, and it will keep raising interest rates until those things happen. If that means more carnage in the stock market—well, that’s a feature, not a bug.

What about housing and shelter inflation? Demand and supply dynamics don’t seem about to change markedly.

CHINA

‘How did you go bankrupt? ‘Two ways’, gradually and then suddenly.’ (Hemingway)

We just reached the second stage in this slow-mo disaster. Good luck Mr. Xi! But it will ripple…good luck us all!

Major China Developer Sunac Defaults as Debt Crisis Spreads China’s fourth-largest developer said in a filing to the Hong Kong stock exchange that it didn’t pay a $29.5 million coupon on the note before the end of a grace period Wednesday, and that it doesn’t expect to make payments on other securities.

(…) “Going into the cycle you may have been expecting 20%-30% of developers defaulting, but now we are talking about more than 60% or 70% of the market being priced under 60 cents on the dollar, where the implied default rate is very high.” (…)

- China’s Economic Slowdown Is Rippling All Around the World For decades, the world has depended on China as a massive factory floor and market. Now, as the country’s economic growth crumbles, the pain is spreading globally.

(…) The effects of China’s slowdown are showing up everywhere from German factories to Australian tourist spots. Exports are weakening in Asia as China’s neighbors watch their largest market sag. Companies including Apple Inc. and General Electric Co. warned investors about production and delivery problems stemming from China’s troubles, as well as dwindling sales. (…)

That means its weakening economy is bad news for commodity exporters such as Brazil, Chile or Australia that supply China with oil, copper and iron ore. It is bad news for manufacturing powerhouses such as Germany, Taiwan and South Korea that rely on China as a huge market for machinery, cars and semiconductors, as well as a critical link in world-wide supply chains for their companies.

And it is bad news for the U.S., where galloping inflation is squeezing household budgets. (…)

China in 2021 accounted for 18.1% of global gross domestic product, according to International Monetary Fund data, behind the U.S. at 23.9% but ahead of the 27 members of the European Union at 17.8%. It accounts for almost a third of global manufacturing output, according to United Nations data from 2020. (…)

Official data Monday showed Chinese export growth slowed sharply in April, as lockdowns hammered factories and global demand waned, especially in Europe and Japan. After adjusting for inflation, imports of iron ore were 13% lower than a year earlier, imports of copper were down 4% and imports of cars and chassis were down 8%, according to economists at Nomura. (…)

“China’s policy makers have heralded easing to prevent a growth slowdown—but have yet to fully act,” senior economists at BlackRock Investment Institute, the investment analysis division of the world’s largest asset manager, BlackRock Inc., said in a note to clients Monday, in which they downgraded their stance on Chinese assets to neutral. (…)

Taiwan and South Korea’s exports to China in April each fell 3.9% compared with March, according to economists at Goldman Sachs. The slide highlights how some Asian economies are tightly plugged into China’s industrial engine, making them especially vulnerable to a slowdown.

Data from the Organization for Economic Cooperation and Development show that whereas Chinese parts and other inputs account for around 1.4% of the value of U.S. goods exports to the rest of the world, in South Korea they account for 5.2%, in Taiwan, 6.3% and in Vietnam, 14.4%. (…)

Around 900,000 jobs in Germany depend on the Chinese market, he said, while German companies employ close to one million people in China.

Mr. Wuttke said he expects the worst of the Covid-related disruption from the recent lockdowns hasn’t even been felt in Europe yet, as shipments that were supposed to leave China during the last couple of months would only now start to arrive in European ports. (…)

Global growth slows and inflation pressures intensify amid rising economic headwinds

- Global Auto Production Forecast Downgraded Further for 2022

- Copper Sinks Below $9,000 as Metals Slide on Global Demand Fears

- China’s Li Urges Fiscal, Monetary Policies to Boost Economy “We should further study and use a variety of policy tools to effectively stabilize employment.”

- PBOC Says It’s Making Stabilizing Growth a Higher Priority “The PBOC will make stabilizing growth a more prominent priority, strengthen cross-cyclical policy adjustment, and accelerate to implement policy measures already announced, especially to actively plan new policy tools,” said Chen.

- Russia Cuts Gas Supplies to Germany in Escalation of Energy Feud

- Recession looms after UK economy shrank in March

Bitcoin Falls Below $26,000, Tether Briefly Edges Down From $1 Peg Bitcoin plunged and the world’s largest stablecoin, tether, briefly edged down from its $1 peg, adding to fears of more turbulence in the cryptocurrency market.

- More Than $200 Billion Wiped Off Cryptocurrency Market in a Day

- Coinbase Says Users’ Crypto Assets Lack Bankruptcy Protections Cryptocurrency trading firm warns its customers could be viewed as general unsecured creditors

- Tether Reassures Markets After Biggest Stablecoin Slips While Tether claims to be backed dollar-for-dollar by actual assets, questions about the quality of the assets it holds have persisted.

FYI, it’s been rumoured that many of the commercial paper assets “backing” Tether are Chinese developers’…

We will shortly know who’s swimming naked. Here’s a candidate:

- SoftBank Reports $13 Billion Annual Loss, Hit by Tech-Share Slump The publicly listed stocks that compose much of the Japanese technology investor’s Vision Fund have fallen by more than half since the start of the year.

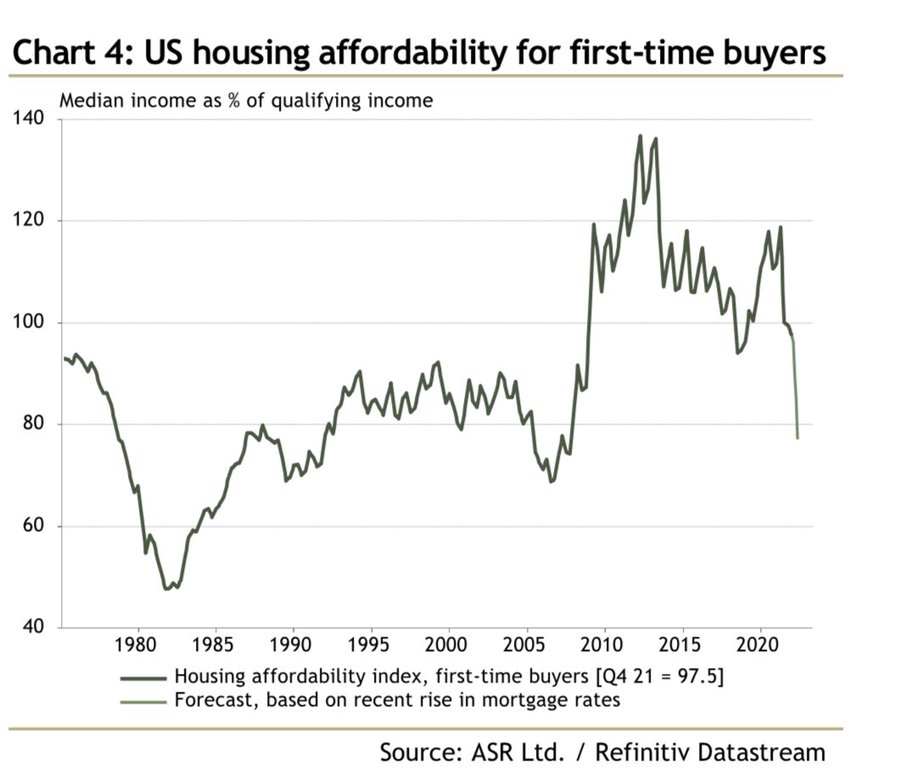

OSFI says it may tweak mortgage stress test as interest rates climb, housing market cools Since the Office of the Superintendent of Financial Institutions toughened the mortgage stress test last June, the country’s housing market and borrowing conditions have changed significantly

(…) OSFI rules apply to borrowers who do not require mortgage insurance, which occurs when borrowers make a down payment of at least 20 per cent of the property’s purchase price. The regulator requires borrowers to prove they can make their mortgage payments at an interest rate of 5.25 per cent, or 200 basis points above their mortgage contract, whichever is higher.

But now, fixed-mortgage rates are quickly rising as the Bank of Canada embarks on an aggressive round of interest-rate hikes, and could soon top OSFI’s minimum qualifying rate of 5.25 per cent.

Today, the average five-year fixed-rate mortgage has an interest rate of 4.19 per cent, according to mortgage brokers. That is up from January’s average of about 2.69 per cent. That means that a borrower must now prove they can make their mortgage payments with an interest rate of 6.19 per cent if they want a fixed-rate mortgage, which is already above the 5.25-per-cent stress-test floor. And the stress test will become even harder as mortgage rates continue to climb.

That will drive more borrowers to variable-mortgage rates, as well as to non-bank mortgages – which typically have higher interest rates than chartered banks.

Already, borrowers are seeking variable-rate mortgages, which are at about 2.4 per cent today, according to mortgage brokers. (…)

Borrowers are also turning to alternative lenders such as trusts and private mortgage-investment companies, which do not have to comply with federal banking rules. (…)

VALUATIONS CORRECTION

First and foremost, this is a valuation correction, the pricking of the broad valuation bubble. Profits are still rising and apart from a few doomsayers, recessions calls are still not significant (though rising). Fed tightening has just begun. Since 1962, there have been 9 tightening episodes, 7 ending in recessions, starting on average 27 months after the first hike (range 12-41 months).

Since 1961, there have been 7 valuation correction episodes, when the Rule of 20 P/E exceeded 23 and subsequently declined to its median “fair value” of 20. Only 3 were followed by recessions (1968, 1971, 2000).

The valuations corrections lasted between 3 months (1987) and 28 months (2000-03) with an average of 13 months (median 9 months) and brought the S&P 500 index down 17.5% on average before the index reached “fair value”. (In 1992, valuations corrected but equities nonetheless rose 12.5% as profits exploded 40% during the period.) Excluding this episode, valuations corrections brought the S&P 500 down 18.3% on average and lasted 11 months on average.

During the current episode, the S&P 500 has declined 18% so far over 4.5 months but the Rule of 20 P/E, at 24.5, remains 18% above its 20 fair value.

There are 2 ways to reduce the R20 P/E: rising earnings and/or declining inflation. If the current consensus is right, trailing EPS will near $221 after the Q2 earnings season in early August. To get a R20 P/E of 20, we would thus need inflation at 2.4% at the current 3900 level.

Assuming inflation of 4%, an index level of 3550 would be fair value. Understand that undershooting is the norm.

Because after the valuations correction might come the recession correction which would take earnings down.

The Great Dollar Squeeze of 2022 is causing global havoc The rocketing US dollar is draining global liquidity and tightening conditions violently for large parts of the international financial system, and for the interlinked nexus of credit contracts and derivatives.

(…) Something was bound to snap, and snap it has over the last three trading sessions. Almost every asset has gone down in unison: equities, credit, Bitcoin, gold, commodities, and ‘high beta’ currencies. Technical support lines have been breached across the board. (…)

The twin-effect a rising dollar and rising US rates is slow torture for the $12 trillion offshore dollar lending market. Borrowers in emerging markets have $3.7 trillion of outstanding loans and bonds denominated in dollars (BIS data), and a substantial chunk is on maturities of one-year or less, and must therefore be rolled over at much higher cost.

Some $9 trillion of global financial contracts are priced off dollar credit rates (formerly Libor). The Financial Stability Board in Basel estimates that world markets have $200 trillion of notional exposure to dollar-linked derivatives. As US Treasury secretary John Connally said pithily in 1971: “the dollar is our currency, but your problem”. (…)Episodes of extreme currency misalignment have powerful consequences and usually end badly. This one feels like a mix of the Asian financial crisis in 1998 and Europe’s ERM crisis in 1992, both caused by the relentless rise of an anchor currency that was causing havoc for everybody else on the periphery. (…)

The BoJ has briefly achieved the Holy Grail of 2pc inflation but it is the wrong kind of inflation, causing people to tighten their belts rather than generating a virtuous circle of rising wages and rising demand. Governor Haruhiko Kuroda thinks the headline rate will slither back down. It is “very, very hard” to create lasting inflation, he said.

The weak yen has in turn destabilised China’s exchange rate policy, made worse by Xi Jinping’s war on “disorderly capital”, by which he means overmighty technology tycoons who dare to defy the Communist Party. It is made worse yet by his refusal to ditch zero-Covid in the face of Omicron, a policy now enforced with a Maoist hunt for “doubters, distorters, and deniers”.Beiijing has given up trying to defend yuan in the face of capital flight and the competitive trade threat of the cheap yen, all too aware that currency intervention has the unwanted side-effect of tightening internal credit conditions within China. This would compound what is already a de facto recession.

Beijing has let the yuan plummet against the dollar over the last month, though we are not yet back to the Chinese currency crisis of 2015. (…)The consensus among the big banks is that the Fed will blink once Wall Street drops by another 5pc or so. Or put differently, the strike price of the ‘Fed Put’ is around 3,800 on the S&P 500 index. We are getting close. And remember, bear market rallies can be torrid.

There again, the consensus may be wrong, and we have yet to find out what ugly feedback loops have already been set in motion by the Great Dollar Squeeze of 2022. The weak link is never where you expect it to be.

- Sterling’s Drop to Parity With the Dollar Is a Growing Risk Traders fear that high inflation and weak economic growth will make it impossible to keep the UK currency from dropping further.

Finland Says It Will Apply to Join NATO in Response to Russia’s Ukraine Invasion Membership of the alliance would be a major break from decades of nonaligned defense policy and deal a blow to Russian President Vladimir Putin’s ambition to divide and weaken the Western alliance.

Rare Russia Criticism Within China Shows Simmering Policy Debate

Russian setbacks in Ukraine have begun to prompt more explicit warnings in China about Moscow’s value as a diplomatic partner, in a sign of growing unease over President Xi Jinping’s strategic embrace of Vladimir Putin.

Russia was headed for defeat and being “significantly weakened” by the conflict, a former Chinese ambassador to Ukraine told a recent Chinese Academy of Social Sciences-backed seminar in remarks widely circulated online. The comments, which Bloomberg News was unable to verify, were attributed to retired diplomat Gao Yusheng, who served as China’s top envoy in Kyiv from late 2005 to early 2007. (…)

“The so-called revival or revitalization of Russia under the leadership of Putin is a false proposition that does not exist at all,” Gao said. “The failure of the Russian blitzkrieg, the failure to achieve a quick outcome, indicates that Russia is beginning to fail.” (…)

Besides Gao’s comments, one of the country’s most prominent international relations scholars said this week that the war meant “nothing good” for China because it accelerated a shift from globalization.

“The war makes it almost impossible for Russia to have any global influence,” Yan Xuetong, dean of Tsinghua University’s Institute of International Relations, said in an interview Tuesday with Phoenix TV. The conflict brings “only losses and damages to China, but no benefits whatsoever,” Yan said. (…)

Gao, the former ambassador to Ukraine, went further to say that Russia was “duplicitous” and had reneged on promises. (…)

INTERESTING MAP

![]() FYI: Are NFTs really art? Collectible and cartoonish, these digital multiples, traded in cryptocurrency, confer membership of an exclusive club – sometimes literally. But do they have any aesthetic value? A critic weighs in. (The Guardian)

FYI: Are NFTs really art? Collectible and cartoonish, these digital multiples, traded in cryptocurrency, confer membership of an exclusive club – sometimes literally. But do they have any aesthetic value? A critic weighs in. (The Guardian)