US Treasuries have best week in a year Government bond prices rise and yields tumble despite strongest inflation reading in 13 years

(…) “I didn’t anticipate the kind of decline in nominal yields that we’ve seen,” Summers told “Wall Street Week” with David Westin on Bloomberg Television. “I’m surprised. I would have expected that yields would have risen more.” (…)

“Monetary policy has been getting steadily easier through this year even as the economy’s booming,” Summers said. “That defies good sense.” (…)

He noted rapid expansion in the economy and consumer demand, reports of labor shortages, a housing market that’s “on fire” and the warnings of company purchasing managers as reasons to worry.

“It’s going to lead to problems and the sooner we recognize that, the better it will be,” he said.

Leaders of the Group of Seven rich nations were in broad agreement about the need to continue supporting their economies with fiscal stimulus after the ravages of the COVID-19 pandemic, a source familiar with the discussions said on Friday.

The backing for more stimulus was shared by all leaders including Angela Merkel of Germany which has traditionally opposed heavy borrowing to spur growth, a position it has relaxed in the face of the COVID-19 crisis.

The administration of U.S. President Joe Biden has been pushing its allies to keep on spending with Treasury Secretary Janet Yellen urging her G7 colleagues in February to “go big”.

“There was broad consensus across the table on continued support for fiscal expansion at this stage,” the source said, adding that Biden, British Prime Minister Boris Johnson and Italy’s Mario Draghi expressed particular support.

The International Monetary Fund has repeatedly urged Group of Seven countries and others to continue fiscal support measures. (…)

“There was a bit of discussion on inflation but the feeling was that it was temporary,” the source said. (…)

RECOVERY WATCH

- Why That Sofa You Ordered Isn’t Showing Up Soon Even companies that have built domestic supply chains are running up against extreme shortages of goods and labor.

(…) Manufacturing and shipping delays have pushed back delivery times across the industry by months. That has put a limit on the ability of many manufacturers to capitalize on demand. IKEA is short of some furniture at certain U.S. stores, and a Design Within Reach promotion offers discounts on purchases of items in stock. (…)

Demand hasn’t let up. Consumer spending on furniture and appliances in the first quarter of this year remains nearly 30% above that time frame in 2019, before the pandemic began, according to federal data. (…)

“Our open orders are way beyond what we can actually produce right now,” said Bell Vice President Judy Bell. (…)

Wood-Products also got Room & Board to agree to raise the wholesale prices it pays for Wood-Products furniture, in part to account for record lumber prices. Room & Board said it wouldn’t change prices from those listed in its catalog. (…)

- From Thor Industries’ latest quarterly results:

“We continue to see robust demand for our RVs and see no signs of demand slowing even as the economy recovers from the pandemic. The most recent RVIA forecast projects total North American wholesale RV shipments of approximately 576,100 units in calendar year 2021, representing an increase of 33.8% over 2020.

Demand in the market remains very high, such that our recent deliveries to dealers are being sold at retail very quickly and are therefore not increasing dealer inventory

levels. Currently, independent RV dealer inventories are at historically low levels in North America and we believe the restocking cycle will take a number of quarters to complete. In the longer-term, which we define as late calendar 2022 and beyond, we expect to get back to a more normal ordering cycle where dealers order to replenish sold stock, and we anticipate that demand will continue to exceed historical norms even after dealer inventories are restocked. (…)This increasing consumer demand has driven our order backlog to more than $14 billion at the end of the quarter and includes units that will be needed to restock depleted dealer inventories. (…)

While we reported excellent results, the supply chain continues to be a constraint for the RV industry and THOR Industries alike, limiting our ability to further increase production to meet increased levels of dealer demand.

- ‘Revenge Spending’ Clears Out Lamborghini for Most of 2021 It’s almost sold out for the year as an easing pandemic unleashes a free-spending attitude among consumers confined to their homes for months.

THE INFLATION DEBATE

On May 18, I published THE INFLATION DEBATE: JFK, LBJ, JOE AND JAY, highlighting how the current economic, financial and political situation resembled the mid-1960’s. Last week, the WSJ had an essay by Jon Hilsenrath making the same parallel. And Joseph Carson added his own angle. Good reads.

- When Americans Took to the Streets Over Inflation In the 1960s and 1970s, spiraling prices for staples like meat and gasoline wreaked havoc on the U.S. economy, thanks to political and policy mistakes that offer a warning for today.

(…) The mid-1960s started out looking like the old pattern. Consumer prices started rising as President Johnson sought to fund the Vietnam War and his Great Society social programs. But as the war ground on, so did creeping inflation. “They didn’t do anything about it,” Mr. Cecchetti said.

When Richard Nixon entered the White House in 1969, the annual inflation rate had already risen to 5%, from less than 2% during the Kennedy administration. What followed was more than a decade of mismanagement by Republicans, Democrats and a supporting cast at the Federal Reserve, a critical institution that was supposed to be apolitical. (…)

Hilsenrath describes how inflation crept in thanks to various policy errors and a weak and political Fed, magnifying the effects of excessive monetary stimulation.

(…) Mr. Bosworth said he suspects policy makers will ultimately conclude they pumped too much money into the economy in response to the pandemic. Will we see Americans in the streets again protesting out-of-control prices? Not if policy makers heed the lessons of the past.

My own conclusion was:

If Janet Yellen moved from the Fed chair to Treasury Secretary, one could say that Jerome Powell has set a foot in each job. Such dynamic duo of very similarly noble minds is likely to test the historical and necessary independence of the Federal Reserve. But rest assured, Powell wrote to Senator Rick Scott on April 8, 2021

“We understand well the lessons of the high inflation experience in the 1960s and 1970s, and the burdens that experience created for all Americans. We do not anticipate inflation pressures of that type, but we have the tools to address such pressures if they do arise.”

Interest rates being where they are, Powell must know he will need teamwork if “we” need to “address such pressures if they do arise”. But he may be underappreciating the importance of 2022 and 2024 in the Democrat politicians’ agenda.

As William McChesney Martin learned, “you can’t abolish the law of supply and demand. That is a law we must reckon with always, for whenever we ignore the working of the market we do so at our peril, and ultimately must pay the piper.”

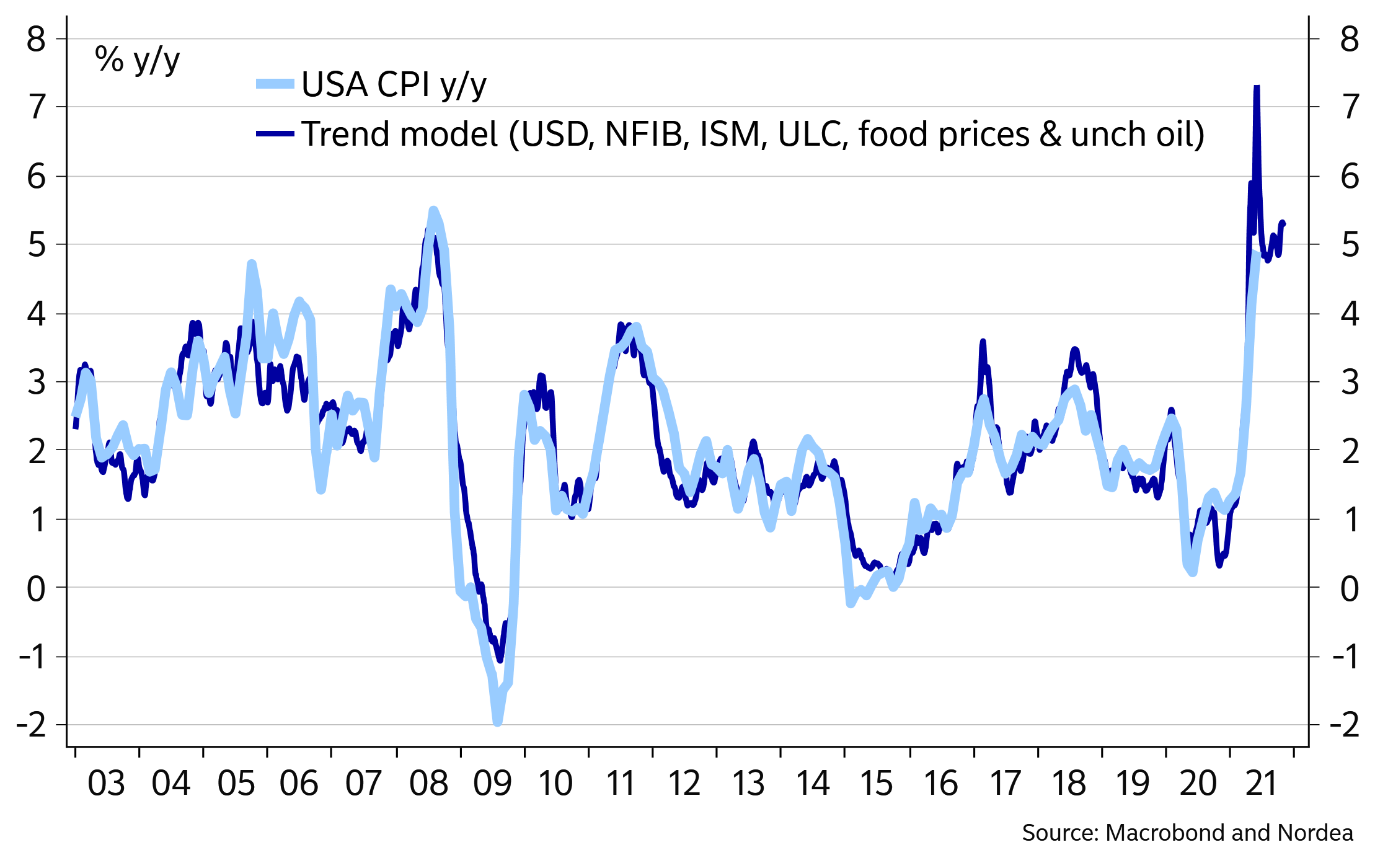

Consumer price inflation is experiencing its most significant increases in decades. Yet, reported inflation does not capture the full scale and breadth of experienced inflation. I never thought the US would experience rampant inflation again, but based on the 1970s price measurement methods, the US experienced double-digit inflation in the past twelve months. (…)

Over the last several decades, reported inflation has seen substantive measurement changes. For example, government statisticians now employ an arbitrary and non-market price for owner’s rent, removing actual housing prices from the calculation. Other substantive changes in the CPI occurred in the mid-1990s following the Congress-sponsored Boskin report, which purportedly shaved 50 to 100 basis points off of reported core CPI each year.

Adjusting reported inflation for those exclusions or changes would result in double-digit gains in both headline and core CPI for the past twelve months. What’s worse, knowing consumer prices are running at a double-digit pace, or not knowing actual inflation is that high?

Denying that the current inflation cycle is nothing more than a base effect and is, therefore, “transitory” brings back memories of the 1970s. In the 1970s, Federal Reserve Chair Arthur Burns denied that monetary policy played a role in the inflation cycle. Mr. Burns argued that higher inflation was due to idiosyncratic factors, such as food shortages and the OPEC oil embargo.

The Fed Chair demanded that the Fed staff strip out the volatile food and energy components to prove his point, thereby creating what is now called the core inflation index. That proved to be a policy blunder as it allowed Mr. Burns to maintain an easy money policy that fueled the most significant and most extended inflation cycle in the post-war period.

In recent decades, regional branches of the Federal Reserve have created new price conventions (e.g., median cpi, trimmed cpi). These price measures are misleading as they eliminate the tails in the distribution of prices. And during price cycles, the price tail for items rising a lot is much larger in scale than those at the bottom.

Once inflation cycles start, they gain momentum on their own. That is because price cycles force changes in firms’ pricing, ordering, inventory policies, and workers’ wage demands. (…)

Inflation cycles end badly, even when everyone is aware of the problem. Investors are the biggest fans of the “doing nothing” approach of the current generation of policymakers. Yet, if past inflation cycles are a guide to the future, investors will soon become the Fed’s loudest critics.

The U.S. Department of Commerce has a little known stat, “Market-based PCE”, “a supplemental measure that is based on household expenditures for which there are observable price measures”, i.e. excluding imputed prices. The BLS does not have a similar measure in its CPI data.

Market-based PCE inflation has accelerated sharply this year, from 1.2% annualized in the last 4 months of 2020 to 5.2% during the first 4 months of 2021 and 6.2% during the most recent 2 months (May data will be released at the end of June). Core Market-based PCE is up 4.3% a.r. since December 2020 and also +6.2% a.r. in the last 2 months.

- Survey says: the Initiative on Global Markets at the University of Chicago’s Booth School of Business last week released a poll of 38 top economists who reacted to the following statement: “The current combination of U.S. fiscal and monetary policy poses a serious risk of prolonged higher inflation.”

A very normal curve: 30% agreed, 24% disagreed and 46% were uncertain with their respective confidence level roughly the same (only 4% strongly disagreed).

Markit’s PMI Input Price Index suggests that the CPI could soon reach 6% YoY. Let’s hope it does not happen because it would mean a +1.5% MoM surge in June’s headline CPI, last seen in August 1973 (+1.8%). Note that May was the worst of the base effect. In both June and July 2020, headline CPI rose 0.5% MoM (core: +0.24% and +0.54%).

Retiring Workers Alter Fed’s Calculus on Jobs Shortfall Shrinking labor force lowers the bar for when monetary stimulus can be dialed back

Federal Reserve officials have long said a key condition for raising interest rates is a return to maximum employment. Their evolving views about how much job growth that will entail could lead them to roll back support for the economy sooner than previously expected. (…)

The Fed has never put a number on its full employment target. Still, central bankers for months have compared current employment to the number of jobs in February 2020, before the pandemic hit the U.S. economy, to illustrate the ground that needed to be made up. Chairman Jerome Powell said earlier this year that gap was “one way of counting it.” In May, the shortfall stood at 7.6 million jobs. (…)

The Fed believes many factors holding back the labor force are tied to the pandemic and will fade later this year.

But one might not: The 2.6 million people who retired since February 2020, according to estimates from the Dallas Fed. A steadily aging U.S. population suggests limited scope for reversing that trend, some economists say.

“The number of people who left the labor force through retirement was higher during this pandemic recession-recovery than in previous recession-recoveries,” Cleveland Fed President Loretta Mester said June 4 on CNBC. “Typically, when people retire, they don’t come back into the labor force.” (…)

Because of the retirement wave, Ms. Mester said she is focusing more closely on participation in the labor force by people who are of prime working years, ages 25 to 54. (…)

If officials become convinced that the economy is destined to operate with lower rates of labor-force participation than before, they could start to tighten policy sooner than expected. (…)

“The spike in retirements may well moderate in a stronger economy, as we saw in the year or two before the pandemic,” the Fed’s vice chairman for supervision, Randal Quarles, said May 26. But, he added, “We may need additional public communications about the conditions that constitute substantial further progress since December toward our broad and inclusive definition of maximum employment.”

That was my point on June 7:

But the Fed’s goals may require reconsideration. There is clearly a supply problem, particularly in the 55+ age group which accounts for 2 million of the 7.6 million missing workers and which has shown no inclination to re-enter the workforce.

And if, like Miss Mester, we focus on the 25-54 age group, we find these facts:

- this group’s employment is still down 4.0% from its February 2020 level, 4.1 million people;

- men and women are down by the same percentage and number, 2.0M people each;

- the number of 25-54 unemployed remains 2.2M above its Feb. 2020 level;

- but another 2.3M have actually left the labor force.

Remarkably, while the participation rate of the 55+ group remains at its cycle low, that of the other age groups has not increased after its spring 2020 bump up.

It’s not because of a lack of jobs:

Given all these available jobs and the re-opening of the economy, particularly the service economy, we should see a rapid increase in employment during the next 4 months as the pandemic unemployment programs expire.

In February 2020, there were 7.0 million job openings and 3.1 million unemployeds. There are currently 2.3 million more openings and 2.2 million more unemployeds as well as 2.3 million more people “not in the labor force”. Then consider that 2.6 million people have since presumably retired for good. Is there a Tinder app for jobs?

This a.m.:

- Fed Officials Could Pencil In Earlier Rate Increase at Meeting Federal Reserve officials could signal this week that they anticipate raising interest rates sooner than previously expected, following a spate of high inflation readings.

In March, the last time they released quarterly economic forecasts, most officials expected to keep the Fed’s benchmark interest rate near zero through 2023 to encourage the economy’s recovery from the pandemic. Officials are set to release updated projections Wednesday after a two-day policy meeting. (…)

For inflation to meet officials’ March forecasts, prices would have to not only stop rising but fall over the rest of the year. Barclays Bank PLC now expects annual inflation, measured by the Fed’s preferred gauge, to hit 3.6% in the fourth quarter—nearly double the central bank’s target.

Fed officials’ individual March projections, charted in their so-called dot-plot, showed all 18 policy makers expected to leave interest rates unchanged through this year. Four expected to start lifting rates next year, and seven projected that rates would be higher by the end of 2023. (…)

JPMorgan Chase chief U.S. economist Michael Feroli said he now expects the dot-plot to show a median expectation of a rate increase in 2023.

“We are also bringing forward our expectations for liftoff to late 2023,” he said in a note Friday. (…)

Fed officials’ updated forecasts are also likely to show they expect the economy to grow faster this year than the 6.5% they projected in March. Goldman Sachs & Co. LLC economists estimate growth of 7.7% this year, helping to push inflation to 3.5% in the fourth quarter from a year earlier.

At a recent conference, former Dallas Fed president Richard Fisher said that “there is a little rebellion taking place within the FOMC as we speak.” Some members are getting very uncomfortable inside the little corner they have painted themselves in. If inflation proves that it is not transitory, “then the weed of inflation grows and kills the garden. That’s the risk position they’ve put themselves in right now.”

Powell has told us to forget the pre-emptive Fed, that the FOMC is now in reactionary mode, needing to see actual data before changing course. And this Fed has become more socially/politically minded, targeting low unemployment for certain ethnic/racial groups, etc..

Yet, nobody told us that monetary policy no longer operates with a lag.

Investors have a lot of faith in this Fed, and in the Powell put. And the Fed knows that, knows that it needs to move carefully, i.e. slowly. But how slow can you be if inflation runs wilder than you expect, if the economy grows faster than you think, if wages rise more than expected?

Let’s pray.

-

Bank of America: Everyone Knows The Fed Will Stop Tapering As Soon As The S&P Drops 10%

- John Authers: The Inflation Scare Is More Heat Than Light So Far

(…) We tend to think in terms of narratives (as Robert Shiller told us last week), and it’s easy to pick the right data to support your pre-existing deflationary or inflationary narrative. The [new Authers’] Indicators will attempt to guard against this and force us to look at the balance of the evidence.

(…) we are presenting the [35] indicators as a heat map, with each square determined by its Z-score for the last 10 years. In other words, they will be colored according to how far they are from the average for the last decade (in which everyone grew accustomed to a “low-flationary” paradigm). A Z-score above 2 implies that a measure is higher than it was for 95% of the time over the last decade. Much higher numbers suggest a clear and present danger of inflation. (…)

So what this tells us, is that official measures of inflation are flashing alarm (after May’s very high numbers), and that surveys of consumers and businesses also suggest elevated concerns. Beyond that, there is little reason for anxiety. (…)

- For David Rosenberg, inflation jitters will turn into deflation fear by year-end The supply side needs some time to respond, he said, but it will, in the second half of the year. Which is about the same time as those government stimulus measures begin to fade and the heat comes off demand.

(…) Mr. Rosenberg said that, frankly, anyone trying to place a firm bet on the inflation numbers or any other economic data in this pandemic is playing with fire. The COVID-19 crisis has made many traditional economic indicators pretty hard to read and anticipate, much less predict. (…)

“We’re in a bog of uncertainty, and intense volatility, as it pertains to all the data,” he said. “To be drawing hard-core assumptions on the future, based on what we’re seeing right now, I think is a dangerous proposition.”

![]()

- “We held off on that for a period of time because we weren’t sure whether the inflation was transitory, and we didn’t want to put our market share and our customers in a place where we all didn’t want to be. But at this point, we’ve said that inflation is big enough and is pervasive enough in the market” – Stanley Black & Decker (SWK) CEO James M. Loree

- ‘This is 100 per cent the worst thing we’ve ever seen’: How Canadian companies are adjusting to supply chain chaos

(…) “There’s only so much anybody’s going to pay for a plastic trash can or a drapery rod,” Mr. Mandelbaum says. “We don’t want to lose our relationship with the customer. We don’t want to lose our space on the shelf. And so we’ll work for no money for the rest of the year.”

At South Shore Furniture, a family-owned furnishings manufacturer headquartered in Sainte-Croix, Que., president Jean Laflamme says his three factories were on the verge of shutting down recently because the company had trouble getting metal drawer guides, handles and other specialized pieces it typically sources from China. He is now ordering enough stock to last six months instead of the usual three and has also had to import things by plane.

“We’re fighting like the devil in holy water to find suppliers in other countries that can help us,” says Mr. Laflamme. “It’s an ongoing fight. Every day we find a new problem somewhere.”

The appetite for South Shore’s furniture and decor has rarely been stronger, but the company can’t meet the demand, he adds. His team has been forced to slow down production at times in recent weeks to make sure they have enough parts and materials, and they’ve now decided to refocus on a smaller number of products they can crank out with consistency.

Companies that will be most successful in weathering this storm are those with the financial capacity to stock inventory and parts in advance, according to Mr. Laflamme. On the flip side, those with tight cash flows and limited access to credit will be particularly vulnerable. The smallest businesses with no experience navigating the whims of spot-market freight costs might not survive. (…)

Still, the company says ongoing supply-chain constraints will continue to undermine retail sales growth in the months ahead, particularly as it relates to the availability of certain raw materials. BRP’s biggest problem now is the same one hitting car makers, consumer electronics companies and sectors from biomedicine to telecommunications: It can’t get enough semiconductor chips.

Rather than cutting production, BRP is maintaining output for its Sea-Doos, Ski-Doos and Can-Am brand all-terrain vehicles, and setting aside any models with missing components for final finishing later on. (…)

“This is a complete reset of the whole industry,” says Mr. Boisjoli. “Dealers are cleaning out used inventory, new inventory. [Manufacturers] are doing the same. And all of us have a chance to do things better going forward than the system we had before.” (…)

The paradox is stark: At a time when many companies are generating some of their highest-ever sales, the money isn’t flowing to the bottom line. At Umbra, sales surged 40 per cent last year to roughly $200-million, and they’re up 82 per cent so far this year through May, according to Mr. Mandelbaum. Profit, however, is down 34 per cent as costs eat away at earnings. (…)

TECHNICALS WATCH

Amid the hated discussions about the economy, profits, inflation and valuation, smart technical analysis has been a good guide throughout these totally uncharted waters. Lowry’s Research remains my favorite source for technical analysis, followed closely by CMG Wealth’s generous blog.

Last week’s action finally resolved to the upside stocks’ uncertain behavior of the last several weeks but low demand intensity prevents a clear all-out buy signal.

Small caps have had a strong rally since mid-May but they have yet to break above their mid March highs with greater demand conviction.

The same can be said for NDX:

The NYFANG Index retraced to its 100dma but it has yet to break its lower highs line. (Components: BABA, AMZN, AAPL, BIDU, FB, GOOG,NFLX, NVDA, TSLA, TWTR)

The volatility on AMZN during the last year is amazing, particularly the convergence of its moving averages and the recent decline in its 200dma.

A flat stock while sales and cashflow per share jump 55% and 50% respectively has to get valuation down. AMZN’s price/CF is near the low end of its 23-45 range since 2008 while cashflow margins at near historical highs. Historically cheap even though biz remains really strong. On the other hand, 28x cashflow is nowhere cheap. Just FYI. (Chart from CPMS/Morningstar)

But back to small caps. The end of June is when the Russell 2000 gets “rebalanced”, so to speak. Bloomberg’s Tracy Alloway explains:

As the value of certain meme stocks jumps at key times, those companies are going to be included in benchmark indexes tracked by passive investors who are actively trying to avoid making big bets.

As Michael Green, chief strategist at Simplify and a former Odd Lots guest (you can listen to him here), told me this week:

“The indexers just do what they’re programmed to do—buy in proportion to market cap. The assumption is always ‘the market is right.’

So meme stocks simply become a way of exploiting the passive algorithms. You can make Melvin cover their shorts AND make Vanguard and BlackRock buy…kinda genius short-term, but very damaging to capital allocation long-term.

SPACs (like Lordstown) are a little more ‘gross.’ They exploit a loophole in index methodology called “fast-track inclusion.”

If they come in adequate size and with adequate float (increased by the PIPE), they can result in index inclusion in as few as five days versus 6-12 months for a traditional IPO.”

A good example of this dynamic is taking place this month in the form of the Russell 2000’s annual reconstitution exercise, which is set to be affected by the surge in certain meme stocks including AMC. Some on WallStreetBets are also salivating about the prospect of both Clover Health and Lordstown being included in the revamped index. “RIDE skyrockets, shorts are f—-d, covering happens, frenzy begins. the week of June 27th WILL BE NUTS,” said one Redditor.

Veteran short-seller Mike Wilkins used less colorful language in his recent 28-page letter to investors, summarized by Institutional Investor this week, but the sentiment was the same. Benchmark index inclusion is turning into a convenient way for meme stocks to find new bagholders:

“While the bulk of Wilkins’ letter looked back in great detail, he noted that the rebalancing of the Russell 2000 at the end of June ‘is going to be a doozy.’

Wilkins is predicting a 30% turnover. ‘The rebalance is done by ranking U.S. stocks almost solely by market capitalization,’ he explained, and ‘since last June’s rebalance, many penny stock silverfish have grown their market values substantially.’

‘Greater fools will arrive in late June,’ he warned, ‘wallets dangling from back pockets.’”

So the Russell 2000 chart shown above could inherit a very different allure post “rebalancing”.

House Bills Seek to Break Up Amazon, Big Tech Companies Lawmakers proposed a raft of bipartisan legislation aimed at reining in Big Tech, including a bill that seeks to make the e-commerce giant and others split into two companies or shed some of their products and services.

The bills, announced Friday, amount to the biggest congressional broadside yet on a handful of technology companies—including Alphabet Inc.’s GOOG -0.30% Google, Apple Inc. AAPL 0.98% and Facebook Inc. FB -0.36% as well as Amazon AMZN -0.08% —whose size and power have drawn growing scrutiny from lawmakers and regulators in the U.S. and Europe.

If the bills become law—a prospect that faces significant hurdles—they could substantially alter the most richly valued companies in America and reshape an industry that has extended its impact into nearly every facet of work and life.

One of the proposed measures, titled the Ending Platform Monopolies Act, seeks to require structural separation of Amazon and other big technology companies to break up their businesses. It would make it unlawful for a covered online platform to own a business that “utilizes the covered platform for the sale or provision of products or services” or that sells services as a condition for access to the platform. The platform company also couldn’t own businesses that create conflicts of interest, such as by creating the “incentive and ability” for the platform to advantage its own products over competitors. (…)

The proposed legislation would need to be passed by the Democratic-controlled House as well as the Senate, where it would likely also need substantial Republican support.

Each of the bills has both Republicans and Democrats signed onto it, with more expected to join, congressional aides said. Seven Republicans are backing the bills, with a different group of three signing on to each measure, according to a person familiar with the situation. (…)

Rep. Ken Buck (R., Col.), the panel’s top Republican, said he supports the bill because it “breaks up Big Tech’s monopoly power to control what Americans see and say online, and fosters an online market that encourages innovation.” (…)

Gaining sufficient Republic support for the bills will be an uphill battle: While Republicans are concerned about technology companies’ power, many are skeptical about changing antitrust laws. Even if they pass, the laws could take years to implement as federal agencies try to enforce them over the companies’ likely legal objections.

“The fact that there is day-one support from Republican antitrust leaders suggests these bills are definitely in the doable range,” said Paul Gallant, an analyst with Cowen & Co. “But the gap between sounding tough at a hearing and actually voting for a breakup is significant. I do wonder if these bills can get to 60 [votes] in the Senate.” (…)

While the bills don’t name any companies, only Amazon, Apple, Facebook and Google currently meet the parameters laid out in those bills, according to the person familiar with the matter. (…)

")

")

@RARohde

@RARohde