U.S. Manufacturing PMI: Production growth accelerates amid stronger client demand,but supply chain disruption remains marked

May PMITM data from IHS Markit indicated a substantial improvement in the health of the U.S. manufacturing sector, with the rate of overall growth accelerating to a fresh record high. The upturn was supported by stronger expansions in output and new orders, with the pace of the latter reaching the fastest on record. Nonetheless, constraints on production capacity were exacerbated further during the month, as severe supply-chain disruptions led to a marked accumulation of backlogs of work and one of the fastest rises in input prices since data collection began in May 2007.

Although firms were able to partially pass on higher cost burdens, supply shortages and the potential for future strain on capacity pushed output expectations down to their lowest for seven months.

The seasonally adjusted IHS Markit U.S. Manufacturing Purchasing Managers’ Index™ (PMI™) posted 62.1 in May, up from 60.5 in April and from the earlier release ‘flash’ estimate of 61.5. The increase in business activity signalled among U.S. manufacturers was among the strongest in the 14-year series history.

Contributing to the uptick in the headline figure was a significant expansion of production during May. The increase in output was widely attributed to stronger client demand and a further marked rise in new order inflows. The accelerated pace of growth in production was the second-strongest since late-2014. That said, component shortages and supplier delays reportedly continued to limit operating capacity, and stymied the upturn. Although the extent to which lead times for inputs lengthened softened slightly, it was among the most marked on record.

New orders increased at the fastest pace on record in May, as both domestic and foreign client demand ticked higher. The upturn was often linked to the loosening of COVID-19 restrictions and successful vaccine rollouts, which led to stronger demand conditions. Similarly, new export order growth quickened, and was the sharpest since the first month of data collection in May 2007.

As a result of the combination of strong demand and supply constraints, supplier prices were hiked once again, leading to the sharpest rise in cost burdens since July 2008. Greater demand for inputs across the sector, in addition with higher logistics fees, were commonly cited as factors driving the rise in input prices.

Firms sought to pass on higher cost burdens to their clients amid favourable demand conditions, with the rate of charge inflation quickening to a fresh series high.

Meanwhile, backlogs of work rose at an unprecedented pace. Despite a further expansion in employment, firms noted that efforts to process work-in-hand were stymied by input shortages. As such, the rate of job creation slowed to the softest since December 2020. Others also stated that the slower rise in employment was linked to difficulties finding suitable candidates and struggles to fill available vacancies, exacerbating capacity constraints.

In an effort to protect against future supply shortages, firms increased their input buying activity markedly. Pre-production inventories were built at the fastest rate on record, but stocks of finished goods fell further as holdings were used to supplement production.

Finally, supply issues weighed on business confidence in May. The degree of optimism remained upbeat on average, but dipped to a seven-month low amid concerns regarding future supply flows.

Chris Williamson, Chief Business Economist at IHS Markit:

These backlogs of orders should support further production growth in the next few months, adding to signs of impressive economic expansion over the summer. But manufacturers’ expectations further ahead have moderated, hinting that the growth rate is peaking, linked to worries about capacity limits being reached, rising prices hitting demand and a peaking of stimulus measures.

China Factories Delay New Orders as Costs Rise, Risking Supply Shortages Buffeted by rising costs, some Chinese manufacturers are refusing to accept new orders or are considering shutting down operations temporarily—moves that could put more strain on global supply chains and cause more inflation.

(…) Surging raw-material prices and a shortage of workers have pinched smaller Chinese manufacturers, including many that sell their products to the U.S. and other Western markets. While many have passed their higher costs on to overseas buyers, the pain is so severe at some manufacturers that they are finding it hard to raise prices enough to make up the difference. Others don’t want to risk losing business to competitors. Many are now looking for other solutions to avoid losing money. (…)

But the strategy could fail if prices of raw materials continue to climb, or if Western demand doesn’t cool. In that scenario, factories that curb production would just be creating more goods shortages that in turn could lead to more cost pressures. (…)

The latest gauge of China’s factory activity showed signs of a slowdown. The official manufacturing purchasing managers index edged down slightly to 51.0 in May from 51.1 in April, led by a cool-off in new orders, though the index remains above the 50 mark that separates activity expansion from contraction. A subindex tracking small enterprises fell into contraction in May after two months of expansion. (…)

In a recent survey conducted by the Shanghai branch of the People’s Bank of China, about 47% of manufacturers said they plan to adjust prices in the near term. And 37% said they will be cautious about accepting new orders, wrote Lü Jinzhong, head of research with the PBOC’s Shanghai branch in an official publication in May. More than 38% of those surveyed expect prices for raw materials to continue climbing for another quarter on average, the article said. (…)

Foshan Modern Copper & Aluminum Extrusion Co., an aluminum processing firm with around 700 factory workers in Guangdong province, said the factory is still short 70 workers even after it raised salaries by 10% this year, compared with the usual 3% annual increase before the pandemic.

“Obviously that’s still not attractive enough for many young people,” said Huang Ruifeng, a representative at the company. “Covid likely prompted more workers to stay in their hometowns instead of looking for jobs.” (…)

Yesterday we saw apparent, though mild, contradictions between China’s official Manufacturing PMI and Markit’s, the former being down a little from 51.1 to 51.0 and the latter being up a little from 51.9 to 52.0. Markit’s survey is broader and includes more mid and small size firms while the official PMI is more weighted towards larger companies. China’s increased emphasis on pollution control may be responsible for slowing production at larger, state-controlled, firms.

- China’s economic boom leaves manufacturing hubs short of power Factories ordered to shut for days after hot weather and coal concerns exacerbate supply problems

According to Markit,

The ASEAN manufacturing sector as a whole saw sustained growth in May. Central to the latest upturn were further expansions of both output and new orders. For the latter, the rate of increase slowed only slightly from April’s eight-year high and remained strong overall. As a result, factory production rose for the third straight month. The rate of output growth slowed on the month, but was nonetheless the second-strongest since May 2018.

- J.P. Morgan Global PMI: Strong upswing in global manufacturing sector led by solid expansions in the eurozone, UK and US

The global manufacturing sector expanded at a robust pace in May. Production rose at one of the fastest rates in a decade, as new order growth accelerated to an 11-year high. The outlook remained positive, with manufacturers forecasting further increases in output over the next 12 months.

The J.P.Morgan Global Manufacturing PMI™ – a composite index produced by J.P.Morgan and IHS Markit in association with ISM and IFPSM – posted 56.0 in May, up from 55.9 in April, to register its highest level in over 11 years (April 2010). Solid improvements in business conditions were seen across the consumer, intermediate and investment goods sectors. (…)

Subdued growth was registered in Japan, China, Russia and India. The Philippines, Turkey, Thailand, Mexico, Colombia and Myanmar all saw contractions. (…)

Pressure on capacity continued to build during May. Average vendor lead times lengthened to the greatest extent in the survey history, while backlogs of work at manufacturers rose at a near survey-record pace. This fed through to increased inflation, as highlighted by the steepest rise in input costs for over a decade and record inflation of selling prices.

John Authers today: China’s Inflation Could Be the World’s Problem

(…) A fascinating piece by Gavekal’s Louis Gave attempts to derive the likely psychology of the current leaders from their upbringing. They spent their youth under Mao Zedong, and had their fill of Marxist orthodoxy. Counterintuitively, this might make them very anxious to avert rising inflation:

“all Chinese leaders were raised in the Marxist church. And the first tenet of this faith is that historical events are shaped by economic forces (rather than individuals or ideas), with inflation being among the most powerful. For Karl Marx, Louis XVI would have kept his head and his throne, had it not been for rapid food price inflation in the years before France’s revolution in 1789. And for a Chinese technocrat, the Tiananmen uprising of 1989 only happened because, at the time, inflation was running above 20%.”

As this chart from Gave shows, the Tiananmen massacre of 1989 followed a period of extreme inflation, while China’s devaluation a few years later, as Deng Xiaoping opted for a policy of aggressive growth, brought another awful price spike in its wake. The degree to which it has kept headline inflation under control since then, against the background of historically impressive growth, is remarkable. It suggests that China’s leaders really, really want to avoid higher inflation:

On this basis, the People’s Bank of China is the latter-day Bundesbank, dedicated to eradicating inflation when all others are more relaxed about it.

(…) if China is a less enthusiastic buyer of stuff, it could mean slower global growth. And second, if it exports inflation as it once exported deflation, it creates a very distinct extra problem for the rest of the world.

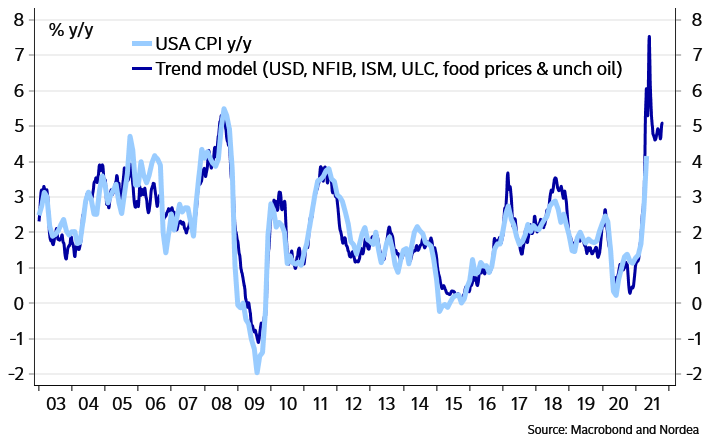

- Historically, the U.S. dollar tends to fall when U.S. CPI is higher than rest of DM (BCA Research)

While still on inflation, Markit’s data is troubling:

Eurozone manufacturing continued to grow at a rate unprecedented in almost 24 years of survey history in May, but also indicated record capacity constraints. While several indicators suggest output growth will remain very strong in coming months as firms reduce backlogs of work, these indicators also highlight growing price pressures, which are currently at a record high.

The IHS Markit headline PMI broke new records for a third month in a row during May to rise to a new high of 63.1. The surging manufacturing sector adds to signs that the eurozone economy is rebounding strongly in the second quarter, especially as the upturn in May was accompanied by signs from the flash PMI of the service sector also showing renewed signs of life.

However, production growth would have been even stronger in May had it not been for record supply delays. Supply difficulties and widespread shortages of inputs are constraining output and leaving firms unable to meet demand to a degree not previously witnessed by the survey.

With new orders growing faster than output, the production shortfall relative to demand signalled in May was the largest for 12 years.

Backlogs of uncompleted work (orders received by manufacturers but not yet started or completed) have consequently accumulated at a record pace.

High sales volumes are consequently depleting warehouse stocks, resulting in a new order to inventory ratio far in excess of anything previously recorded by the survey.

While these forward-looking indicators bode well for production and employment gains to persist into coming months as firms seek to catch up with demand, the flip-side is higher prices. The combination of strong demand and deteriorating supply is pushing up prices to a degree unparalleled over the past 24 years.

The survey data therefore indicate that the economy looks set for strong growth over the summer, but will likely also see a sharp rise in inflation.

We expect price pressures to moderate as the disruptive effects of the pandemic ease further in coming months and global supply chains improve. We should also see demand shift from goods to services as economies continue to reopen, taking some pressure off prices but helping to sustain a solid pace of economic recovery. However, this assumes the impact of the pandemic continues to wane in the coming months, and further waves of COVID-19 infections would inevitably darken this improving picture. With signs already appearing of Asia-Pacific economies being hit by a renewed surge in cases, a smooth path to the restoration of global supply chains is by no means assured.

")

")

")

")

ING adds:

Across eurozone industry, multiple sectors are now reporting significant shortages in equipment. The European Commission’s Economic Sentiment Indicator provides quarterly information on which factors are limiting production and ‘equipment’ has spiked as a factor in 2Q 2021. In fact, for total eurozone industry, it is now at its highest level since the start of the indicator in 1985, with 22.8% of businesses reporting equipment shortages as a key factor limiting production.

Shortages are rising across sectors, but the sectors affected most by this are logical given the pressing problems in computer chips, plastics and lumber. Rubber and plastics producers top the list, with electrical equipment producers a close second. Automotive, wood and computer and electronics producers round out the top five, showing a clear link to the problems in finding chips, plastics and lumber at the moment.

The impact on production has varied for now, with the main problems accumulating in the auto sector so far due to semiconductor shortages. This has brought production down -14.3% from its November peak. Other sectors are seeing less impact in terms of outright production declines. Furniture production is also down 6% from its recent peak, while smaller declines are reported among computer and electronics producers.

Shortages have become a key issue in several industrial sectors

Source: Eurostat, ING Research

The impact on producer prices has started to show. In April, producer prices increased by 7.6% year-on-year, the strongest increase since 2008, much of which is because of energy price base effects. For some of the sectors most affected by shortages, the lack of availability of inputs has not yet translated into excessive increases in producer prices up till now. This could be because the data lags a bit; producer prices for May have not yet been reported. It could also be because the shortages represent a small amount of total inputs in the production process, think of computer chips in car production. In wood production, we’re starting to see elevated producer prices at 6.3% YoY in April, but the spike in lumber prices continued in May so this is not yet the peak.

The sectors for which we have seen large increases in producer prices have been base metals and the manufacture of coke and refined petroleum products, at 18.3 and 53.1% YoY. So for many of the sectors experiencing shortages, margins have not yet come under huge pressure, which has limited the pressure to raise prices so far.

Even though producer prices have had differing responses to shortages, businesses do seem ready to start increasing prices. Selling price expectations among businesses have shot up dramatically in recent months, which has been led by sectors depending on lumber as its main input, but also the oil and chemicals sector, rubber and plastics and basic metals sector have seen a rapid rise in expected selling prices.

While other sectors have seen a more muted response, almost all goods-producing sectors currently face a much higher percentage of businesses expecting to increase prices than was the case on average in the 2016-2019 period. This shows that businesses do intend to increase prices on the back of the disruptions facing the supply chain.

Selling price expectations are the highest for industries experiencing shortages

Source: European Commission, ING Research calculations

The question is how this is going to influence consumer price inflation and importantly, whether the impact is temporary or more long-lasting. When looking at past behaviour of businesses experiencing equipment shortages, we find that the impact on selling price expectations is usually coincident with the shortage. This means that once shortages fade, selling price expectations normalise again.

What firms are currently facing is not a normal event though as chart 3 shows. We’re currently at the highest level of reported shortages limiting production since the start of the time series. When we look at the impact for another period with significant shortages like 2011 when supply chains were significantly disrupted by an earthquake and tsunami in Japan, and flooding in Thailand, we find a slightly longer-lasting effect of higher expected selling prices into the next quarter. Given the extent of the current issue, that could be expected in this period as well.

Now ultimately, we see that this relation between shortages and selling price expectations does translate into consumer prices, but the effect is more watered down and uncertain. Chart 4 shows that the relationship between the two is stronger with a lag of two quarters, which would result in an acceleration of non-energy industrial goods prices for the consumer over the summer.

Shortages are at historic highs, expect goods inflation to trend higher over the summer months

Source: European Commission, Eurostat, ING Research

Goods prices have only risen cautiously so far, but this is just the start. With supply chain issues, shortages of inputs and strong demand, they are going to increase from here and add to inflation that is already above the European Central Bank’s target. This means that when energy base effects start to fade, the ECB will not be out of the woods and we expect inflation to remain above 2% for a large part of 2021.

Still, we do expect most disruptions, and the shortages, to ease over the course of this year and early next, with semiconductors being the major exception, as tight markets are likely to remain. This means that we expect goods inflation to rise over the coming months, but the effect of shortages should fade over the course of 2022 because we find that the impact of shortages on inflation is usually only temporary.

For the ECB this means that, bar any second round effects, the spell of above-target inflation is likely to end sometime early next year. Still, with a strong economic rebound and above-target inflation, a discussion around tapering will be unavoidable in the coming months.

I bet the same is happening in the U.S.. Businesses are now padding orders and hoarding materials, amplifying the problems and inflation expectations.

Oil Price Hits Two-Year High as OPEC Sees More Demand Producers led by Saudi Arabia and Russia plan to pump more as global rebound boosts commodity appetite.

(…) Members of the Organization of the Petroleum Exporting Countries and their allies, a group known as OPEC+, agreed Tuesday to a previously planned output increase of about 450,000 barrels a day, starting next month. Saudi Arabia, meanwhile, agreed to continue easing separate, unilateral cuts of one million barrels a day that it put in place earlier this year.

In April, the group agreed to increase output by more than two million barrels a day by the end of July, bringing cumulative additions over the past year to some four million barrels a day. That is a big chunk of the 9.7 million barrels a day the group agreed to cut early in 2020 when the coronavirus first started shutting down economies, sapping global crude demand and sinking prices. (…)

A technical committee of the OPEC+ group forecast on Monday that oil demand would jump by six million barrels a day in the second half, according to OPEC delegates. As a result, global oil stocks will fall below their five-year average for the 2015-2019 period by the end of July, signaling an end to the pandemic glut, they predicted. (…)

The Organization for Economic Cooperation and Development said Monday it expects global output to increase by 5.8%, which would be the strongest expansion since 1973. (…)

- Business Travel Starts to Make a Comeback Alison Taylor, chief customer officer at American Airlines Group Inc., said 47 of the airline’s 50 largest corporate accounts have said they plan to resume traveling this year.

(…) Corporate trips remain 70% or more below pre-pandemic levels, according to airlines, which rely heavily on business travel for a huge share of their revenue. (…) In a survey by the U.S. Census Bureau conducted in May, 35% of small-business owners said they expect to have travel expenses in the next six months, up from 31.5% in April and 26.5% in mid-February. (…)

Before the pandemic, business travel accounted for roughly 30% of trips, but high-paying corporate customers typically account for as much as half of airline revenues, according to trade group Airlines for America. Domestic and international business travelers in the U.S. directly spent more than $330 billion in 2019, according to the U.S. Travel Association. (…)

Airlines have said they are expecting more business travel to resume this fall, once offices and schools reopen, but a full rebound could be years away. (…)

Bloomberg:

More signs of bullishness in the oil market: Gasoline demand reached the highest since the start of the pandemic last week, reaffirming bets that Americans will be out traveling in force this summer. The cautious optimism is now “fully optimistic,” RBC said. Morgan Stanley boosted its long-term oil price forecasts. U.S. inventories of oil and clean fuels are all seen dropping last week, a survey showed.

AMC Soars as Company Sells $230 Million in Stock to Hedge Fund Mudrick Capital quickly unloads at a profit 8.5 million shares it purchased in deal with movie-theater chain

AMC Entertainment Holdings Inc. took advantage of a skyrocketing stock price last week to sell shares to a hedge fund for $230.5 million, it disclosed Tuesday, news that drove its stock higher still.

The hedge fund that bought the shares, New York-based Mudrick Capital Management LP, was a winner too. It had paid a premium to Friday’s closing price but promptly turned around and sold for a profit, according to a person familiar with the matter, unloading all 8.5 million shares it received in the deal.

AMC’s share price soared as high as $33.53 before ending the session at $32.04, a 23% jump. The movie-theater chain’s stock price is up more than 1,400% for the year, including a furious 116% climb last week. (…)

Mudrick Capital sold the shares it bought—its entire equity position in AMC—on the belief that the stock is overvalued, the person familiar said. (…)

The hedge fund bought the shares at about $27.12 apiece, AMC said in a news release, a 3.8% premium to Friday’s close of $26.12. The price at which the fund sold wasn’t immediately clear. (…)

Individual investors continued to bid up the shares Tuesday. “DIAMOND HANDS BABY, NOTHING CAN LET ME SELL,” one user posted on Reddit. (…)

Mudrick saved AMC from bankruptcy last December injecting $100M in debt financing. Last Friday, it bought $230.5M in equity and promptly resold the 8.5M shares on Tuesday for a profit of around $33M while boosting the value of its debt holding. Good luck baby!

Bloomberg adds:

Chief Executive Officer Adam Aron also addressed the deal in a series of tweets on Tuesday.

“Some of you have asked questions about AMC raising $230.5 million from the sale of 8.5 million shares. Like you, I am an AMC shareholder, and my team and I have the best interests of AMC shareholders very much top of mind.”

Curious as I can be, I fetched INK’s latest insider trading activity report on AMC. Mr. Aron’s teammates seem to have something different at the top of their mind.

No Grave Dancing for Sam Zell Now. He’s Paying Up for Hot Properties. Storied real-estate investor is focusing on more mainstream deals, a strategy reflecting the dearth of distressed properties

Sam Zell, who made a fortune buying distressed commercial properties, isn’t finding many bargains these days.

Instead, the storied real-estate investor is doing something he usually avoids: following the pack and spending big on something safer. (…)

But the 79 year-old’s more conventional investment strategy is the latest sign that the pandemic hasn’t produced the distressed opportunities many investors expected.

Hotels, malls and other properties have suffered enormous declines in revenue. But few owners have been forced to sell at steep discounts thanks to government stimulus programs and the Federal Reserve’s easy money policy which kept a lid on foreclosure. (…)

Yet on a recent conference call, Mr. Zell described retail real estate as a “falling knife”—investors who think they are getting a bargain might end up getting bloody themselves. Prices haven’t fallen enough in the sectors that are getting beaten up, he said.

“There obviously is going to be an opportunity in retail. I just don’t think it’s here yet,” he said. He added that hotels also look expensive: “I can’t relate…pricing to the way I see opportunity.” (…)

Huawei Targets Google’s Android Dominance with Harmony OS The Chinese tech giant plans to launch its new operating system, known as Harmony OS, across many of its smartphones, as well as unveil smart devices that will also run the company’s latest homemade software.

(…) While Huawei’s own smartphone sales are in free fall after briefly topping the world a year ago, the company is targeting other handset vendors that they hope will adopt Harmony OS, posing a direct challenge to Google Android’s dominance of the market.

Samsung Electronics Co., Xiaomi Corp. and the rest of the world’s top-selling phone makers besides Apple Inc. all use Google’s Android. Chinese sellers make up 57% of the global handset market, according to market-research firm Canalys and could be potential takers if Huawei’s Harmony OS develops into a worthy match. (…) More than eight out of 10 smartphones sold run Android. (…)

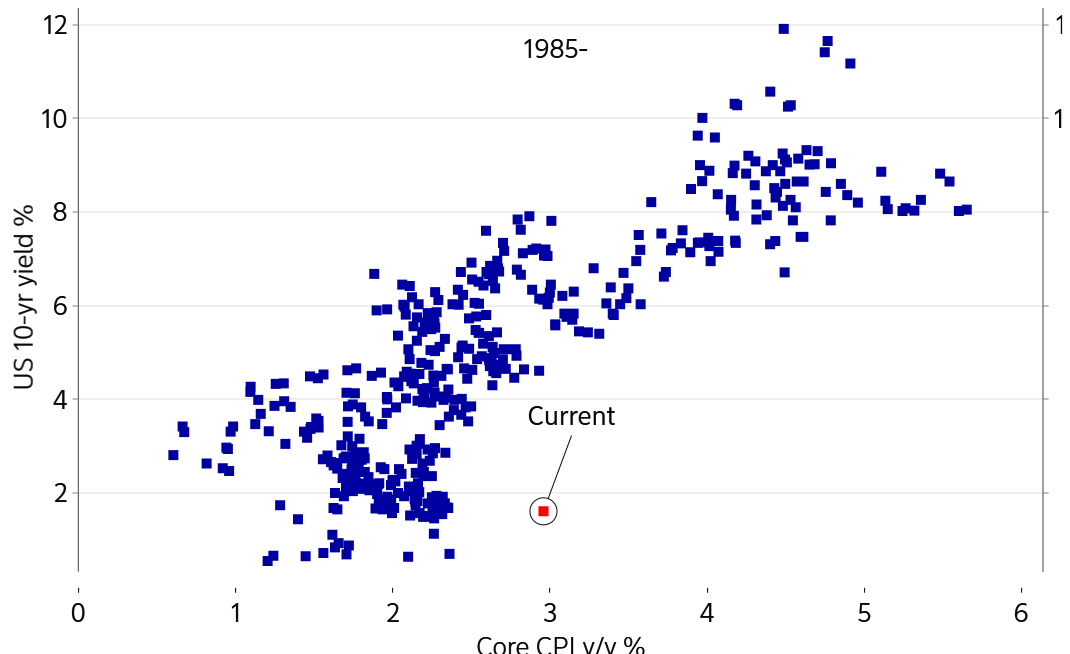

(Goldman Sachs vis The Market Ear)

(Goldman Sachs vis The Market Ear)