The Conference Board Employment Trends Index™ (ETI) Increased in April Index shows no signs of slowing job growth

The Conference Board Employment Trends Index™ (ETI) significantly increased in April, after an increase in March. The index now stands at 105.44, up from 102.65 (an upward revision) in March. The index is currently up 45.7 percent from a year ago.

“Despite the disappointing April jobs report, the Employment Trends Index significantly increased in April, suggesting strong employment growth in the coming months,” said Gad Levanon, Head of The Conference Board Labor Markets Institute. “Most of the Index’s components are rapidly improving. However, the number of employees in the temporary help industry, usually a strong leading indicator of employment, declined in April. Rather than signaling a weak outlook for job growth, it may reflect some substitution in employment as employers hire more regular employees and end contracts with temporary workers. In the coming months we expect job creation to continue, but at a possibly slower pace than expected in light of the latest job numbers. A slew of indicators measuring recruiting difficulties, quit rates, and wage growth suggest the US economy is experiencing an historical, though probably temporary, labor shortage. Among the shortage’s many effects, it may put a damper on job growth.”

- Global business surveys indicated a marked upturn in hiring in April as companies boosted activity in line with resurgent demand for goods and services. As such, the data point to a substantial improvement in official labour market data in coming months. Global PMI data, compiled on behalf of JPMorgan by IHS Markit from its proprietary business surveys of over 28,000 companies in more than 40 countries, recorded the largest influx of new business into businesses since April 2010 at the start of the second quarter. Service providers reported the steepest increase in new orders since June 2014 while manufacturers reported the biggest gain since May 2010.

")

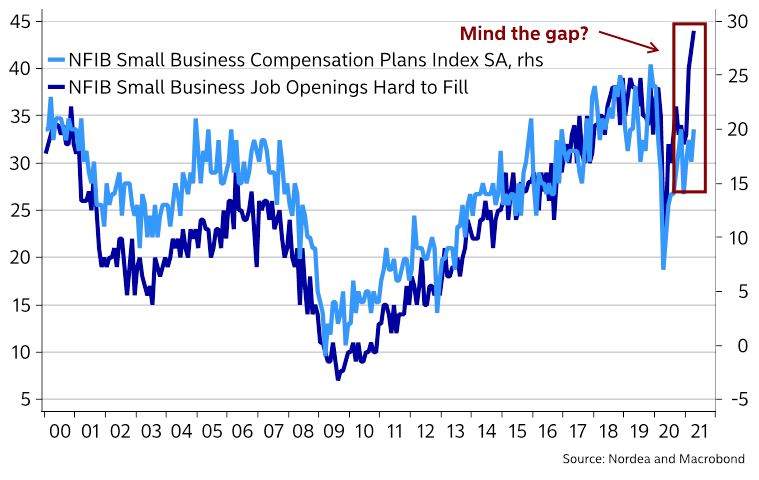

Small Business Optimism Up in April but Job Openings Remain at Record Highs

- This is a pessimistic bunch:

- Sales are only so-so

- but they are aggressively raising prices:

- Job openings remain lower than pre-pandemic:

- Trying to resist increasing wages…

- …because sales are still weak, costs are up and profit are under pressure:

- Trying to protect margins:

- In all, it’s been worse, but it’s ben better:

- Commodities boom sends bulk shipping costs to decade highs China’s ‘insatiable appetite’ for iron ore is key factor in surge in dry bulk index

-

China: PPI inflation has arrived and chip inflation is coming

China’s consumer inflation is still modest due to the very high prices of pork last year. In contrast, producer prices jumped in April due to expectations on infrastructure demand. What’s more, inflation caused by semiconductor chip shortages is on its way.

CPI inflation in April was modest at 0.9%YoY after 0.4%YoY in March. There was a short public holiday in April, and this boosted spending and small leisure trips. But the CPI growth rate was capped by pork prices which were very high last year. This high base effect will normalise from 4Q21. So we will see continued modest CPI growth rate for a few months.

In contrast, PPI in April jumped to 6.8%YoY up from 4.4%YoY in March. That was mostly caused by the expectation of infrastructure projects in China and the US. But the market might not yet have taken into account that some transportation projects in China have been stopped as they overlapped with other projects. This has resulted in a reduction in the issuance of local government special bonds.

According to the [NY Fed] April 2021 Survey of Consumer Expectations, median year-ahead inflation expectations increased to 3.4 percent in April from 3.2 percent in March. This marks the measure’s highest level since September 2013. The three-year outlook remained unchanged at 3.1 percent. Home price change expectations rose sharply to a new series high of 5.5 percent in April from 4.8 percent in March. Rent growth expectations posted a fifth consecutive increase, rising to a new series high of 9.5 percent.

Median household spending growth expectations retreated slightly from a six year high level of 4.7% in March to 4.6% in April.

The Fed Is Playing With Fire

By Christian Broda and Stanley Druckenmiller

(…) Normally at this stage of a recovery, the Fed would be planning its first rate hike. This time the Fed is telling markets that the first hike will happen in 32 months, 2½ years later than normal. In addition, the Fed continues to buy $40 billion a month in mortgages even as housing is clearly running out of supply. And the central bank still isn’t even thinking about ending $120 billion a month of bond purchases. (…)

Not only is the recovery happening at record speed, excesses of fiscal policy are already visible. Consumers are spending like never before, construction is booming, and labor shortages are ubiquitous, thanks to direct government transfers. Two-thirds of all relief checks were sent after the vaccines were proved effective and the recovery was accelerating. (…)

Isn’t the Fed’s independence supposed to act as a counterbalance to these political whims? (…)

The federal government has added 30% of GDP in extra fiscal deficits in only two years, right as the baby-boomer retirement wave is beginning to accelerate. The Congressional Budget Office projects that in 20 years almost 30% of all yearly fiscal revenues will have to be used solely to pay back interests on government debt, up from a current level of 8%. More taxes simply won’t be enough to bridge the gap, so pressures to monetize the deficit will inevitably rise over the years. The Fed should be adapting policy today to minimize these risks. (…)

Even after trillions spent to prop up the bond market, foreigners have continued to be net sellers. The Fed chooses to interpret this troubling sign as the result of technicalities rather than doubts about the soundness of current and past policies. (…)

Fighting inequality and climate change are very far from the Fed’s central mission. (…)

Fed policy has enabled financial-market excesses. Today’s high stock-market valuations, the crypto craze, and the frenzy over special-purpose acquisition companies, or SPACs, are just a few examples of the response to the Fed’s aggressive policies. The central bank should balance rather than fuel asset prices. (…)

Chairman Jerome Powell needs to recognize the likelihood of future political pressures on the Fed and stop enabling fiscal and market excesses. The long-term risks from asset bubbles and fiscal dominance dwarf the short-term risk of putting the brakes on a booming economy in 2022.

-

California Governor Proposes Tripling Spending on Stimulus Checks Most individuals would get $600, and families an additional $500, as the nation’s most populous state enjoys a record budget surplus due largely to booming tax revenues from wealthy residents.

California Gov. Gavin Newsom on Monday proposed a $100 billion economic stimulus plan that would triple the state’s direct cash assistance program to reach an estimated two-thirds of residents.

The announcement comes as Mr. Newsom said the state is expecting an unprecedented $75.7 billion state budget surplus, due largely to booming tax revenues from wealthy residents.

The budget proposal, if passed by the Legislature, would send $600 tax rebate checks to households making up to $75,000 and an additional $500 to families if they have children. The cost of the new checks is about $8.1 billion.

“California’s recovery is well under way, but we can’t be satisfied with simply going back to the way things were,” Mr. Newsom said in a statement.

The Democrat also announced he would be doubling the amount of direct assistance to renters to $5.2 billion and is proposing another $2 billion in aid to help with utility expenses. (…)

The new stimulus plan comes as Mr. Newsom is facing a likely recall election later this year. (…)

About $8 billion of the money is prompted by a 1979 law that requires the state to split excess revenues between schools and taxpayer rebates if the budget surplus hits a certain threshold. The law was last triggered in 1987, when state officials refunded about $1.1 billion to taxpayers.

Mr. Newsom said his proposal goes “above and beyond the statutory requirement.” (…)

- Investors Rush Into ‘Pick-Your-Poison’ Junk Bonds Risky companies are selling junk bonds at a record pace, getting ultralow borrowing costs and increasingly loose borrowing terms, such as “pick-your-poison” clauses.

(…) The pick-your-poison nickname comes from the fact that both cash being paid to shareholders and extra debt being added to the business could be “poison” for existing lenders, but the clause lets the owners of the company choose between taking a dividend or borrowing more money. (…)

In all, nearly 25% of European junk bond deals have had pick-your-poison clauses in the first quarter of 2021, a sharp rise from previous quarters, according to Covenant Review. Among U.S. deals about 14% had such terms, the research firm found in a recent survey. (…)

Tech stocks lead global sell-off as inflation worries flare up Key measure of US inflation expectations reaches highest level since 2006 as economy rebounds

-

The global tech rout that began yesterday in the U.S. has gone global. The Hang Seng Tech Index sank as much as 4.5%, extending its tumble from a February high to about 30%. In Europe, the Stoxx 600 Index fell the most since January as tech sector losses drove the gauge lower. One of the biggest winners over the past year, Cathie Wood’s Ark Innovation ETF, was down more than 3% in pre-market trading after plunging 5.2% yesterday. (Bloomberg)