Vaccines Become a Race Against Time as CDC Warns of Covid Surge

The U.S. could soon go the way of Europe, with a burgeoning resurgence of the coronavirus, as states loosen restrictions and more contagious variants become increasingly prominent, the nation’s top public health official warned. (…)

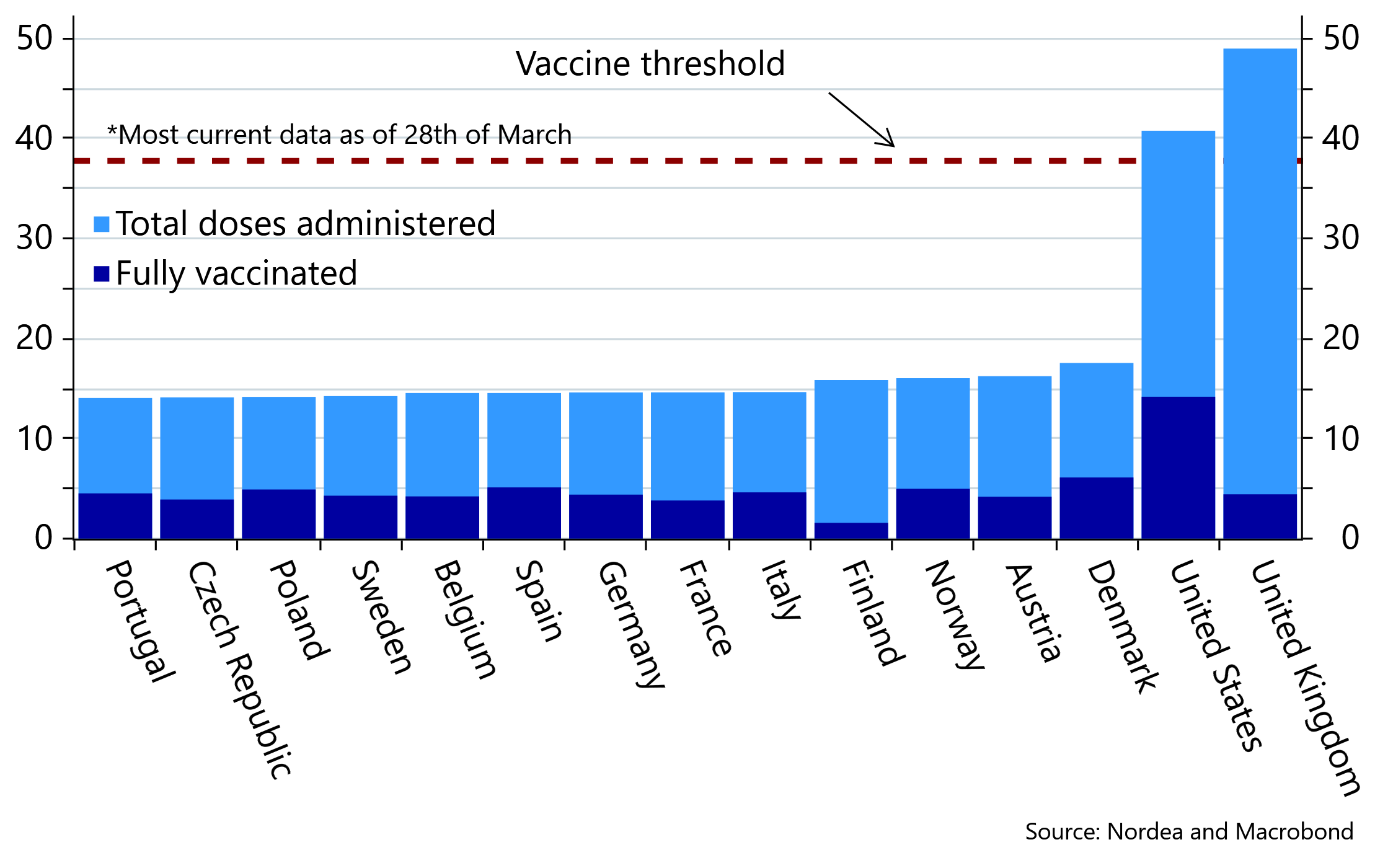

While the U.S. races to vaccinate its population — almost 29% have received at least one dose — the virus could still push ahead, experts said. Each time it infects a new person, the possibility increases of additional mutants that could spread faster or evade vaccines. (…)

B.1.1.7, a contagious strain that first surfaced in the U.K., now makes up about 26% of all sequenced viruses, Walensky said Monday. The CDC has previously projected it could become the dominant coronavirus strain in the U.S. by March. It is “probably less forgiving and more infections will occur,” Walensky said on Monday. (…)

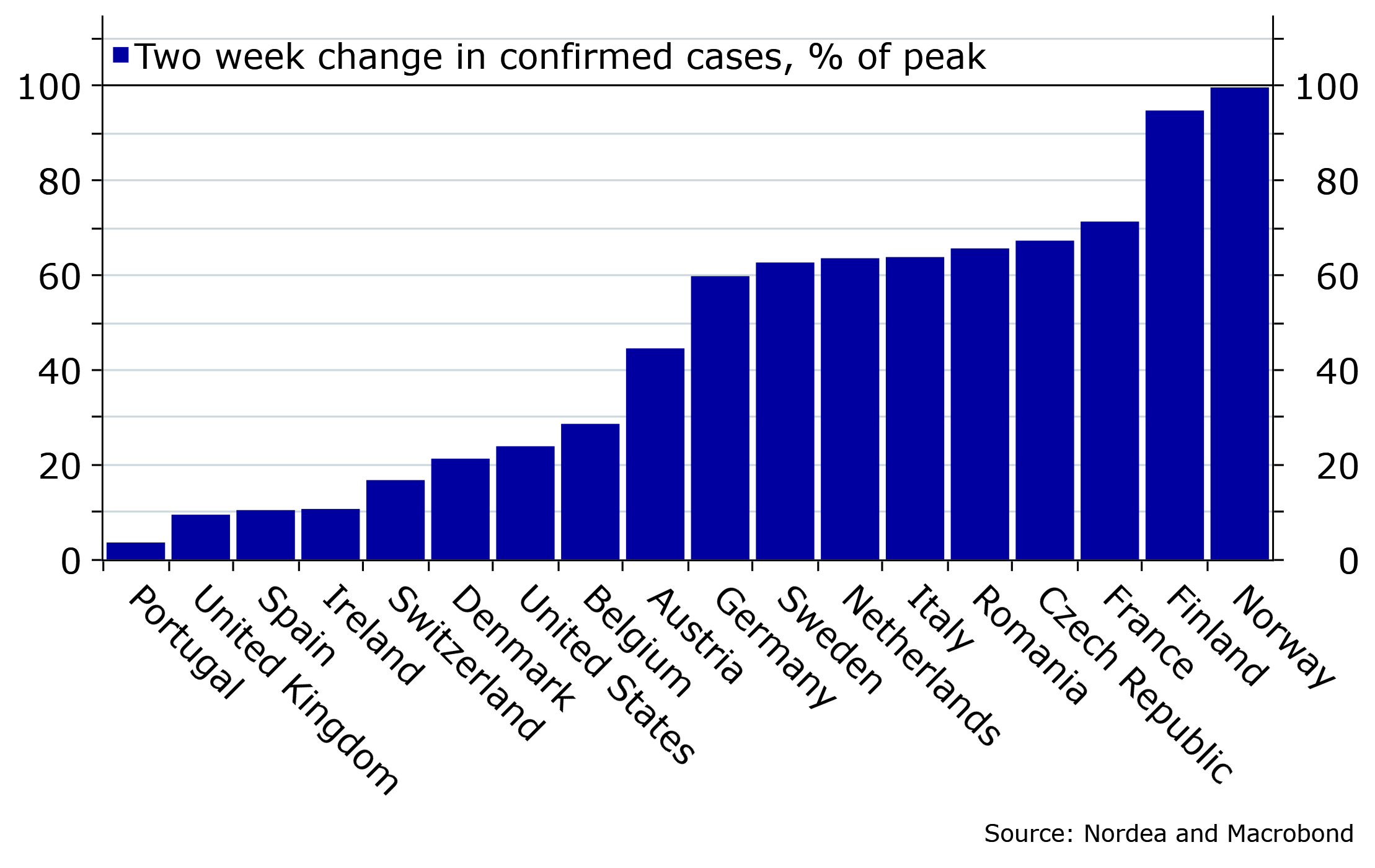

Daily case totals have surged to the highest levels since November in France, where doctors have warned that shortages of ICU beds loom. Italy, Germany and other countries are also seeing increases. So far deaths are well below levels from previous waves of the pandemic, however.

In the U.K., meanwhile, both cases and deaths have plunged to the lowest levels since September. The country has been Europe’s leader in vaccination, with shots given to more than half of the adult population. (…)

Bloomberg

Change in cases over the past two weeks as % of peak of the pandemic

Covid-19 vaccines from Pfizer Inc. and Moderna Inc. effectively prevented coronavirus infections, not just illness, with substantial protection evident two weeks after the first dose, government researchers said.

Two doses of the vaccines provide as much as 90% protection against infection, according to data from U.S. Centers for Disease Control and Prevention study published Monday.

The study adds to evidence that new vaccines made with messenger RNA technology actually reduce the spread of the virus in real-world conditions. An earlier study in Israel found a single dose of the Pfizer vaccine reduced infections by as much as 85%. (…)

Doses administered and fully vaccinated people as percent of population

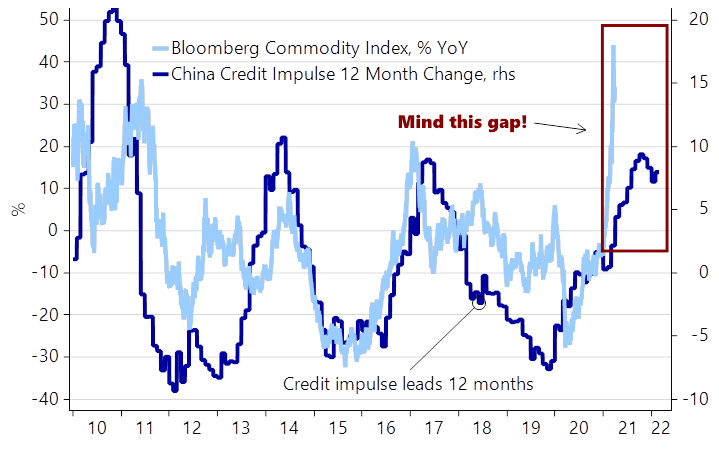

China, Long a Source of Deflation, Starts Raising Prices for the World Rising raw-materials costs and unrelenting supply-chain constraints are prompting many Chinese exporters to increase prices for the goods they sell abroad, raising fears it may add to global inflationary pressures.

(…) Rene de Jong, director of Resysta AV, an outdoor furniture manufacturer based in the southern Chinese city of Foshan, said he plans to raise prices by around 7% on new orders this summer. (…) “In my nearly 25 years in China, I’ve never seen anything like this. I’ve never seen shipping costs like this before while steel and aluminum prices shot through the roof,” he said, adding that the company’s profit margins are under pressure.

Other Chinese exporters raising prices include apparel businesses and a toy wholesaler who told The Wall Street Journal his company has raised prices for new orders across the board by 10% to 15% since the beginning of March. (…)

Prices for imports from China to the U.S. rose 1.2% over the past year, the fastest increase since 2012, with most of the increase coming in the three months ending in February, according to data from the U.S. Bureau of Labor Statistics. (…)

Not an obvious problem just yet:

On the other hand:

- US companies sound inflation alarm From housebuilders to toymakers, businesses say costs are rising

- Saudi Arabia wants OPEC+ to extend oil supply cuts into June, source says

Saudi Arabia is prepared to support extending oil cuts by OPEC and its allies into June and is also ready to prolong its own voluntary cuts to boost prices amid a new wave of coronavirus lockdowns, a source briefed on the matter said on Monday. (…)

“They don’t see demand as yet strong enough and want to prevent prices from falling,” the source said. (…) A source familiar with Russia’s thinking said on Monday Moscow would support extending cuts again while seeking another small rise in production for itself.

On the other hand:

JPMorgan, Salesforce Join List of Firms Dumping Office Space Rise of remote work means demand for office space could be permanently lower for some companies

(…) At the end of 2020, 137 million square feet of office space was available for sublease across the U.S., according to CBRE Group Inc. That is up 40% from a year earlier and the highest figure since 2003. (…) But this time many of the companies ditching real estate are doing well financially; they say they need less space because they plan for more employees to work at least part time from home even after the pandemic is over. (…)

Office rents for more expensive space, including concessions, fell around 17% over the past year in New York and San Francisco and 13% nationwide, according to real-estate firm JLL.

Sublease space usually comes with an additional 25% discount, said David Falk, president of the New York tri-state region at real-estate services firm Newmark. And since firms can sublease on short notice, rising sublease availability can serve as an early indicator of the true state of the office market. (…)

In previous years, tech companies often leased more space than they needed at the time to be prepared for growth, JLL’s Mr. Ryan said. This practice, dubbed space banking, has left some with too much office space that they are now trying to get rid of. (…)

And the suburbs aren’t immune either. A number of companies are looking to get rid of call centers and other back-office facilities in cheap locations, Mr. Ryan said. (…)

FROM GROWTH TO VALUE TO TRASH

Bloomberg’s John Authers:

(…) By Bloomberg’s measurement, pure value is having its strongest performance relative to momentum since 2018. A brief rebound for big tech stocks earlier this month has been canceled out:

(…) The problem may now be that value companies are being bought as though they are completely interchangeable with stocks that do well in conditions of high inflation. They aren’t. In the following graph, Andrew Lapthorne, chief quantitative strategist of Societe Generale SA, compares his “inflation” basket of global stocks, mostly from the resources sector, that will do best during periods of inflation, with the Russell 2000 Value index, which covers U.S. small-caps that look cheap. There are no stocks that are in both, and yet their performance has been identical over the last six months as money has poured into small-cap value ETFs:

To look at the same phenomenon another way, one line in the following chart shows the Solactive Global Copper Mines index (as sensitive to rises in commodity prices as just about any companies on Earth) relative to the MSCI All-World index, and the other the Russell 2000 Value. The performance has been almost identical:

(…) The rally of the last 12 months has in many ways been a “dash for trash,” in which companies with weak balance sheets did better as fears of a widespread bankruptcy crisis receded.

Another way to capture this is through the “quality” factor, which has various definitions but which generally refers to stocks with clean balance sheets and reliable profitability. Such stocks did predictably well during the Covid scare a year ago, and have performed shockingly badly since then, as illustrated by this chart from Mike Wilson, U.S. equity strategist at Morgan Stanley:

High-quality stocks now look extremely cheap compared to low-quality stocks, then. Wilson also compares quality stocks to the U.S. market as a whole going back to 1984, and reveals that the virtues of a strong and stable company have never been less in demand:

(…) interest cover for smaller companies looks barely better than at the worst points of the last two bear markets, as this chart from Lapthorne of SocGen shows:

Just so you know:

EQUITIES: LONG-TERM FORECASTS

U.S. stock prices will double over the next decade, as pandemic-induced policy changes and an increasingly desperate hunt for real returns push investors to equities, Sanford C. Bernstein strategists said.

The S&P 500 index will reach 8,000, up from its 3,971 close on Monday, Inigo Fraser-Jenkins and Alla Harmsworth wrote in a note. (…)

“We are in a totally new policy environment where there is a case for higher (but not too high) inflation and also the possibility that real rates remain low,” Fraser-Jenkins said in an email (…)

“Rates may not respond as quick to inflationary signals,” the Bernstein analysts wrote in the note. “This leaves us with the prospect of persistent low real yields which can justify market valuations.” (…)

- Richardson Wealth warns about valuations:

- KKR pounds the table:

We think that we are in the early stages of an economic recovery that will look quite different from that which occurred starting in 2009. We think that nominal growth will run above trend for the foreseeable future, driven by a stronger than expected consumer and a rebound in non-tech related capital expenditures. While we expect cyclical inflation, we remain in the camp that a secular increase in inflation is not upon us.

From a portfolio construction perspective, we advocate for more of a cyclical bias that favors pricing power and is connected to global growth and hard assets. Financials, Loans, and higher quality Emerging Markets should all benefit. All forms of collateral-based cash flows should be owned in size. By comparison, government bonds should be underweighted in global portfolios, particularly in the United States

In terms of our concerns arising from global growth being too hot, we think that the biggest risk is that investors don’t lean in enough to what our macro models are saying about future growth and return prospects. We do not typically make these type of table pounding statements, but the early indications across the global capital markets in 2021 suggest that we are at the early stages of a secular change in portfolio construction that warrants attention from all globally oriented asset allocators and macro traders.

- US 10-year Treasury yield hits highest level since last January Key measure of long-term borrowing costs reverses nearly all of the pandemic-induced fall

Credit Suisse Bid for Tidy Archegos Fix Ends With Banks Brawling

(…) Given Archegos’s size, unwinding its positions could generate losses of around $2.5 billion to $5 billion for the industry, depending on how hard it is to liquidate holdings, JPMorgan Chase & Co. analyst Kian Abouhossein wrote in a note to clients. (…)

- The question now is whether the implosion at Archegos will have knock-on effects. It could do this by creating equity losses at other funds that force them to make adjustments. Or, more damagingly, it could radiate out through the problems created for the banks who lent to them. By the close of trading Monday, it looked as though major contagion had been avoided. It is always possible that more losses will pop up in unexpected places. (John Authers)

- But many hedge funds have exposure to the same basket of stocks as Hwang’s family office and with the U.S. economy rebounding, some of the speculative capital that ploughed into Chinese shares is exiting.

- Another major bank joined the list of firms warning of potential losses. MUFG’s securities arm estimates a loss of about $300 million tied to an unidentified U.S. client. It’s indeed linked to Archegos, a person familiar said. (BB)

The other question is why bankers continue to heavily deal with people like Hwang:

Prime brokers shook off concerns about Archegos as they eyed lucrative lending

Concerns?

- In late 2008, the Wall Street Journal said Tiger Asia suffered losses from shorting Volkswagen AG (…). Hwang’s Tiger Asia finished down 23% in 2008.

- In 2012, he agreed to pay $44 million to settle with the Securities and Exchange Commission over insider trading of Chinese bank stocks.

- In 2014, Hong Kong banned him for four years and slapped him with a HK$45.3 million fine ($5.3 million).

- In this case, Bloomberg reported that Archegos had used derivatives contracts with brokers known as swaps to gain substantial additional leverage. That meant that the firm didn’t have to disclose its holdings in regulatory filings, since the positions were on the banks’ balance sheets.

FYI: U.S.-based long-short hedge funds are still 201% leveraged, only 9% lower than January’s decade-high. (…) Friday’s margin call was not an isolated event. More pain is in store for those who have embraced the same strategies. (Bloomberg)