Personal Income and Outlays, February 2021

Just out:

Personal income decreased $1,516.6 billion (7.1 percent) in February according to estimates released today by the Bureau of Economic Analysis. Disposable personal income (DPI) decreased $1,532.3 billion (8.0 percent) and personal consumption expenditures (PCE) decreased $149.0 billion (1.0 percent).

Real DPI decreased 8.2 percent in February and Real PCE decreased 1.2 percent; goods decreased 3.3 percent and services decreased 0.1 percent. The PCE price index increased 0.2 percent.

Excluding food and energy, the PCE price index increased 0.1 percent.

- More info: Release Highlights

REOPENING WATCH

- “The Chase card spending tracker rose 1.1%-pt over the prior day and rose 4.8%-pt over the prior week.”

- In the week that ended March 21, Darden Restaurants comparable sales were up 5.4% above the same week of 2019, before the pandemic disrupted the economy. As recently as late February, Darden’s weekly sales still lagged behind pre-pandemic levels by more than 15%. (WSJ)

- Airlines Add Routes in Fight for Americans Ready to Travel Again Carriers have in recent weeks announced plans to fly more than 150 new domestic routes as they try to ferret out pockets of demand and stimulate new markets.

- In China, the World Economics’ Sales Managers Index suggests that

The Chinese Manufacturing sector data for March shows growing confidence in the near future and a major increase in the Sales Growth Index (this is compared with last months New year holiday period, an exaggerated dip); and a good but more realistic increase in the Market Growth, Staffing and Profit Levels indexes.

The big surprise is a significant fall in the Price Index which is attributed by some managers to attempts to benefit from demand in reawakening global markets before rival capacity is fully operational.

The Chinese Manufacturing sector is clearly leaving in its wake the Covid period.

China Manufacturing: Business Confidence Index

Results from the Chinese Service sector are mixed.

All indexes point to growing economic activity as recovery from Covid expands capacity. But Confidence remains relatively low, certainly in comparison with the manufacturing sector.

The Market Growth remains somewhat muted. And the Price Index, in direct contrast with the Manufacturing Sector sister Index is rising.Overall, the Chinese economy is outpacing its rivals in the race to reopen facilities after the damage wrought by Covid over the past year.

U.S. Initial Jobless Insurance Claims Fall 97,000

Initial claims for unemployment insurance were 684,000 in the week ended March 20, a decline of 97,000 from the previous week; that week’s claims were revised modestly to 781,000 from 770,000 initially reported. The Action Economics Forecast Survey had expected 738,000 initial claims for the latest week. The four-week moving average of initial claims eased to 736,000 from 749,000; by a small margin, this was the lowest four-week average since March 14, 2020, just as the pandemic effects were setting in.

Initial claims for the federal Pandemic Unemployment Assistance (PUA) program were 241,745 in the March 20 week, down 42,509 from the week before. These initial claims do move relatively widely from week to week. The PUA program covers individuals such as the self-employed who are not included in regular state unemployment insurance. Given the brief history of this program, which started April 4, 2020, these and other COVID-related series are not seasonally adjusted.

Continuing claims for regular state unemployment insurance fell to 3.870 million in the week ended March 13 from 4.134 million in the prior week, revised from 4.124 million. Continuing PUA claims for the week of March 6 rose 118,898 to 7.735 million from 7.617 million the prior week. The number of Pandemic Emergency Unemployment Compensation (PEUC) claims also rose in that week, reaching 5.551 million, a new high, from 4.817 million the week before. That program covers people who were unemployed before COVID but exhausted their state benefits. An extension of the PEUC benefits was included in the American Rescue Plan bill passed by the Congress earlier this month, and they will now be available until August 29.

The total number of all state, federal and PUA and PEUC continuing claims rose 733,862 in the March 6 week to 18.953 million from 18.219 million week before. This grand total is not seasonally adjusted.

Powell Says Now Is Not the Time to Focus on Reducing Federal Debt Fed chief says level of U.S. government debt isn’t unsustainable, but its growth rate is

(…) “Given the low level of interest rates, there’s no issue about the United States being able to service its debt at this time or in the foreseeable future,” Mr. Powell said Thursday in an interview with National Public Radio. (…)

“There will come a time—and that time will be when the economy is back to full employment, and taxes are rolling in, and we’re in a strong economy again—when it will be appropriate to return to the issue of getting back on a sustainable fiscal path,” Mr. Powell said. “But that time is not now.” (…)

- Senate Democrats Lay Plans for Higher Corporate Taxes Democrats in Congress began building the policy case for sharp corporate-tax increases, arguing that Republicans went too far with their 2017 tax cuts.

(…) In all, Democrats are planning significant reversals of the 2017 tax law signed by then-President Donald Trump, though they aren’t calling for returning to the previous status quo. They are particularly eyeing features of the law that they say give companies incentives to move activity outside the U.S. (…)

Mr. Biden calls for a 28% tax rate, though moderate Democrats may back a smaller increase.

If the U.S. went back to 28%, it would once again have the highest corporate tax rate among major economies after including state taxes, said Pam Olson, who was the top Treasury Department tax official under President George W. Bush.

“That’s a place that I don’t think we want to occupy,” she said.

Goldman Sachs has done the simulation:

Suez Backlog Grows as Efforts Resume to Free Lodged Ship The Suez Canal remained shut as Egyptian authorities worked to clear a ship blocking the critical waterway and shipping experts warned a resumption of traffic through the channel could be days away or longer.

(…) The Suez Canal backup mostly won’t affect big U.S. retailers directly, but European companies will see a hit in an already tight shipping market, said Chris Sultemeier, a former executive vice president of logistics for Walmart Inc., the largest importer and retailer in the U.S.

“The Suez is primarily used for Asia to Europe traffic, so from a consumer goods, retailer standpoint it will have a dramatic effect on Europe,” he said. (…)

Some U.S. importers expecting shipments from India are bracing for potential delays in coming months because of the Suez Canal blockage, adding to what has already been a difficult shipping year. (…)

If the Ever Given can’t be dislodged quickly, or if the vessel isn’t seaworthy because of hull damage or the weight of its cargo, shipping lines will have to divert around Africa, extending transit times and driving up fuel consumption, said Alan Murphy, chief executive of Denmark-based maritime research firm Sea-Intelligence ApS.

A prolonged blockage would exacerbate a continuing container shortage and tie up more vessels and boxes in the Asia-Europe trade lane, Mr. Murphy said. “That would force importers to fight for the available containers,” he said, and the problem would ripple out to other trade lanes the longer the Suez is blocked. (…)

- Dislodging the Suez Canal Ship Said to Need at Least a Week

- What a ship jam looks like: This map shows 150+ ships stuck in the Suez Canal (Axios). Bloomberg counts 237 cargos stuck.

")

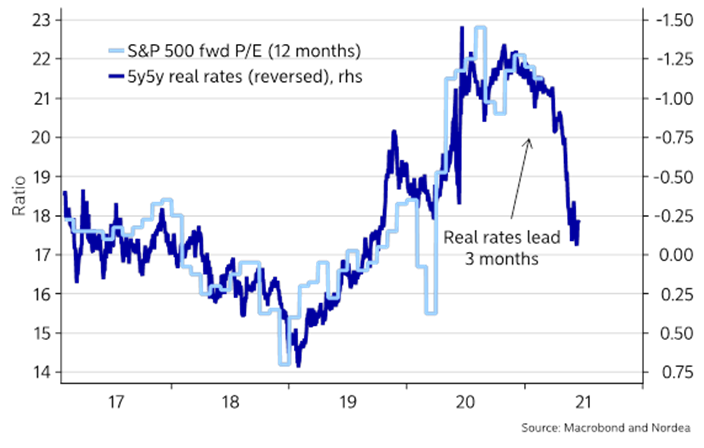

MEAN MEAN REVERSIONS

- The bond price mean reversion was quite mean. It rarely gets worse:

- Are equities also meaning to mean revert? (Ed Yardeni)

- All about real rates and valuation? FYI, 18x forward EPS of $175.60 = 3160. This would be 10% below the current 200dma, the red line on Yardeni’s chart above.

Real rates may have risen enough to cause a setback for risk assets.

- Coincidentally:

AAII Sentiment (Ed Yardeni)

This Bull Market Has a Troubling Reliance on Speculation Earnings, valuation and rampant speculation have all played a role in the extraordinary bull market that began a year ago this week. The latest combination of the three has a troubling reliance on the speculative element.

(…) The parallel in the stock market is the hunt for the greater fool. Sure, GameStop shares bear no relation to the reality of the company, but I can make money from buying an overpriced stock if I can find someone willing to pay even more because they “like the stock.” (…)

- Global deal making hits $1.4 trillion amid blank-check IPO frenzy

- Odell Beckham Jr. Jumps Into SPAC Surge The NFL wide receiver has signed on to be a strategic adviser to a special-purpose acquisition company sponsored by Tribe Capital Management, according to people familiar with the matter.

- WeWork Plans to Go Public in $9 Billion SPAC Merger WeWork has agreed to merge with a special-purpose acquisition company, in a deal that would take the shared-office provider public nearly two years after its high-profile failure to launch a traditional IPO.

(…) A $9 billion valuation is a far cry from the $47 billion that WeWork was valued at in a private round of financing from SoftBank Group Corp. earlier in 2019. The Japanese technology investor was later forced to rescue WeWork and now holds a majority stake.

Bow Capital Management, the SPAC’s sponsor, is run by Vivek Ranadivé, owner of the NBA’s Sacramento Kings and founder of Tibco Software Inc. The venture firm lists basketball great Shaquille O’Neal as an adviser. (…)

![]() Must be the “slam dunk” effect…Here’s the “smash” effect:

Must be the “slam dunk” effect…Here’s the “smash” effect:

And now, the NFT effect:

- New York Times Sells NFT Column in an Auction for $560,000 Another sign of the red-hot market for digital collectibles.

Meanwhile

Biggest Bitcoin Fund’s Woes Worsen as Discount Hits Record

The $29.4 billion Grayscale Bitcoin Trust (ticker GBTC) has dropped about 20% so far this week, nearly double the decline in the world’s largest cryptocurrency. GBTC closed over 14% below the value of its underlying holdings on Wednesday as a result — a record discount, according to data compiled by Bloomberg. The dislocation has deepened despite Grayscale Investment LLC parent Digital Currency Group Inc.’s plans to purchase up to $250 million worth of GBTC shares.

The GBTC free-fall highlights the extent to which the latest leg of the retail-driven crypto craze is cooling. The trust has persistently traded at a premium to its net asset value since launching, with investors willing to pay up for a piece of Bitcoin as it rockets higher. However, given that GBTC doesn’t allow redemptions — meaning that trust shares can only be created, not destroyed like in conventional funds — the number of shares outstanding has ballooned to a record 692 million. With Bitcoin’s price now stalling, that’s created a supply and demand imbalance as accredited investors in the trust seek to offload their shares in the secondary market

“GBTC has a fixed supply and acts like a leveraged play on Bitcoin,” Bloomberg Intelligence analyst James Seyffart said. “As price goes down, sentiment goes down, GBTC is going to fall further than Bitcoin. Same thing happens on the way up.” (…)

In addition to individual investors stepping back, demand from institutions may be cooling with the debut of several Bitcoin ETFs in Canada. While U.S. regulators have yet to approve the structure, high-profile issuers such as Fidelity Investments have filed plans.

“The addition of ETFs in Canada likely pulled away some capital from GBTC,” Seyffart said. “Mainly institutional money, because most retail can’t easily buy a Canadian ETF.”

Fed Says Limits on Payouts to End for Most Banks After June 30 The central bank placed restrictions on dividends and buybacks last summer, citing the need to conserve capital during the coronavirus-induced downturn.

Here we go again:

Argentina Can’t Repay IMF $45 Billion, Vice President Says

Argentina is unable to repay its $45 billion debt with the International Monetary Fund under current negotiating conditions, influential Vice President Cristina Fernandez de Kirchner said Wednesday, diminishing the possibility of an agreement with the country’s largest creditor.

“We can’t pay because we don’t have the money to pay,” Fernandez de Kirchner said at an event in Buenos Aires, adding that the terms and conditions are “unacceptable.” (…)

Argentina faces an economic minefield. The country is just emerging from three years of recession, inflation is projected to hit nearly 50% this year and unemployment is in the double digits. The government’s $65 billion debt restructuring with private creditors last year didn’t boost its credibility, and the bonds are now in junk territory again. The country has no access to foreign credit, forcing it to print money.

Now seeking its 22nd IMF program since 1956, Argentina’s fraught history with the lender includes its 2001 financial crisis, when painful budget cuts urged by the Fund failed to avert an economic collapse and debt default. (…)

Apple’s Move to Block User Tracking Spawns New Digital Ad Strategies Apps and advertisers are looking for other ways to connect with consumers and target ads, as the iPhone maker prepares to roll out an update allowing users to limit ad-tracking.

Facebook Inc., gaming companies and ad-tech providers are weighing a variety of responses, including updated payment models, new advertising techniques and notifications for users. In China, social-media apps have tested a potential workaround that would continue tracking users’ digital footprints. (…)

Once the software is installed, Apple will ask users in a pop-up if they want to allow a given app to track their activity across apps and websites from other companies. If users choose to “ask app not to track,” the apps will no longer be able to collect a user’s advertising identifier without permission. That ad ID is widely used by digital-ad and data brokers, but many expect users to reject tracking amid concerns about privacy. (…)

Alphabet Inc.’s Google has said it plans to comply with Apple’s new rules. Christophe Combette, group product manager for Google Ads, cautioned in a blog post that the changes would reduce visibility into metrics showing how ads drive app installations and sales, and how advertisers value and bid on ad impressions. Google plans to expand use of a tool that infers whether an ad interaction led to online spending or subscription without identifying individual users. (…)

Companies in China tested a possible workaround that would involve creating an alternate advertising identifier to track users without letting them opt out of the data collection, according to people familiar with the matter. The testing was part of an initiative developed by the state-backed China Advertising Association to create a national standard for Chinese technology companies, the people said.

The identifier, called CAID, uses a technique known as “device fingerprinting” that Apple has banned. This method logs data passed between phones and apps, such as their internet protocol addresses, and uses them as clues to keep track of that user. The Financial Times earlier reported the effort. (…)

A Tencent executive told investors Wednesday that Apple’s ad-tracking changes were causing uncertainty globally.

Video-sharing platform TikTok, which is owned by ByteDance, doesn’t intend to use CAID, said a person familiar with the matter. (…)

Apple’s plans to enforce its new policy are likely to lead some apps to change their business models. “Some smaller apps, which used to be free until now, might switch to being paid,” said Barak Witkowski, vice president of product at mobile-ad measurement company AppsFlyer. (…)

Nii Ahene, chief strategy officer at digital-ad consulting firm Tinuiti, predicted an initial pullback in advertising, especially if bought through Facebook, while advertisers gauge its effectiveness under the new rules. In time, advertisers might shift from finding new customers toward communicating with existing ones to boost loyalty, he predicted.

This could be especially painful for the videogame industry, which has long used targeted ads to find the rare customer willing to spend big on in-app purchases.

“They spend most of their dollars trying to find the 1% or 2% of their audience that spends $100, $200 a month,” Mr. Ahene said. “It’s going to be significantly diminished by the fact that you don’t have a unique identifier to attract those individuals.” (…)

Mercedes to Unveil Flagship Electric Sedan With Tesla-Beating Battery

H&M’s Xinjiang Crisis: Manufactured Goods and Manufactured Outrage The digital boycott of H&M’s China business after an online furor over its decision to avoid Xinjiang cotton could be a sign of things to come. Western consumer brands have some uncomfortable decisions to make.

H&M’s Xinjiang Crisis: Manufactured Goods and Manufactured Outrage The digital boycott of H&M’s China business after an online furor over its decision to avoid Xinjiang cotton could be a sign of things to come. Western consumer brands have some uncomfortable decisions to make.

(…) H&M and its stores have found themselves more or less erased from e-commerce platforms like Taobao and even Chinese mapping and ride-hailing services like Baidu Maps and Didi Chuxing. The list of foreign companies targeted by Beijing for crossing ever-shifting nationalist red lines is long—the National Basketball Association, Korean retail brand Lotte, FedEx, and hotel chain Marriott, to name just a few. But the censure aimed directly at H&M is nearly unprecedented, and sends a deeply worrying signal to other Western consumer brands operating in China. (…)

Western consumer brands will increasingly have to choose between customers back home, who find situations like the one in Xinjiang abhorrent, and Chinese consumers who often don’t realize the full extent of what their government is doing and are surrounded by media that depict any criticism of Beijing as a hypocritical attempt to keep China down. (…)

The surge of outrage comes days after the European Union, for the first time since Tiananmen, sanctioned China over human rights. The fact that a European firm was singled out first, before the outrage spread, seems significant. The object may be to inflict so much pain that Europe won’t dare to take further steps in concert with the U.S. to push back on human rights or other issues in the future. (…)

(…) Burberry is a member of the Better Cotton Initiative, a group that promotes sustainable cotton production which said in October it was suspending its approval of cotton sourced from Xinjiang, citing human rights concerns. (…)

The backlash – particularly in social and traditional media – has also enveloped mass-market brands like H&M, Adidas AG and Nike Inc which have previously expressed critical views on labour conditions in Xinjiang, China’s biggest cotton-producing region. (…)

Hong Kong lawmaker Regina Ip said she would stop buying Burberry.

“Burberry is one of my favorite brands. But I will stop buying Burberry products. I stand with my country in boycotting companies that spread lies about Xinjiang,” Ip wrote on her Twitter account.