Walmart Cuts Starting Pay for Some New Hires Under the new structure most new hires will make the lowest possible hourly wage for that store.

The country’s largest private employer changed its wage structure for hourly workers in mid-July, according to documents reviewed by The Wall Street Journal and Walmart employees.

Under the new structure, most new hires will earn the lowest possible hourly wage for that store. In the past, some new hires, such as those who collect items for online orders, would have made slightly more than other new staff members, such as cashiers. (…)

The recent flatlining in Indeed Job Postings (as of Sept. 1) suggests that BLS Job Openings could as well.

- NY Fed’s John Williams yesterday confirmed the focus on wages:

“We’ll have to keep watching the data carefully analyzing all of that and really asking ourselves the question: is this sufficiently restrictive,” he said. “Do we need to maybe raise rates again to make sure that we’re keeping that steady progress in terms of shrinking imbalances in the labor market and bring inflation back down?”

- Student Loan Borrowers Face Repayment Soon. CFOs Are Watching to See if Spending Takes a Hit. ‘Student loans will definitely be a change to the consumer,’ says one finance chief

(…) Some 43 million people, or around 17% of adults in the U.S., have federal student loan debt. The typical monthly student loan payment falls between $209 and $314, equating to a pay cut of around 4% to 5% of U.S. median household income before taxes, according to a Wells Fargo analysis, which used data collected in 2019. (…)

Via John Authers:

Credit card delinquency rates are far from their extremes before the Global Financial Crisis, but they’re clearly rising, particularly among the young. That’s shown in another Ned Davis Research chart:

It’s also concerning to see that use of “Buy Now Pay Later” — a classic sign that consumers are no longer flush with cash — is rising. This chart is from Torsten Slok, chief US economist of the Apollo Group:

(…) Finally, there is a worrying argument from the summer’s excitement over pop concerts, in particular the mega-tours by Beyoncé and Taylor Swift. Incredibly, it looks like they had a measurable impact on US consumption. Now that Swift has moved on to tour the rest of the world, while Beyoncé’s concerts are winding down, that’s reason to expect the consumer to be less active. Indeed, the end of the Beyoncé and Taylor Effect could on its own pull back consumption by 0.6 percentage points in the fourth quarter compared to the third. (…)

During the third quarter, Swift’s “Eras” tour had 15 concerts, with average stadium capacity of 54,000 people. The average spend per attendee was $1,500, (Repeat: Each person paid $1500 to go to a concert, my emphasis added) including tickets, hotels, flights, food and other items. Beyoncé’s “Renaissance” tour has 34 concerts scheduled this quarter in stadiums with an average capacity of 70,000. Each of those attendees is expected to pay a total of $1,800 for the experience. In total, that’s $5.4 billion in extra spending during the quarter. The Barbie and Oppenheimer movies also brought more people to cinemas.

According to Morgan Stanley, the two great female performers don’t seem to have displaced demand for other artists. The fan count at Live Nation concerts (which didn’t involve Swift or Beyoncé) rose 17% in the second quarter of this year compared to the second quarter of 2019. Demand for concert-going is rising.

(…) But these numbers are extraordinary, suggest unnatural consumer strength that must now be close to exhaustion, and imply that expenditures will reduce in the fourth quarter.

A bigger risk…

…considering how low inventories are (strategic reserves included (left) and excluded (right)):

@zerohedge

(…) The crown prince has targeted a higher oil price to pay for its costly Vision 2030 reform project, which ranges from building the concept city Neom on the Red Sea to buying in superstar footballers such as Cristiano Ronaldo. “The reality is that the Saudi budget and MBS’s long term ambitions is going to require oil around $85 or higher,” said Alkadiri. “Projects like Neom don’t get built on $70-a-barrel oil.”

In case you missed yesterday’s Daily Edge:

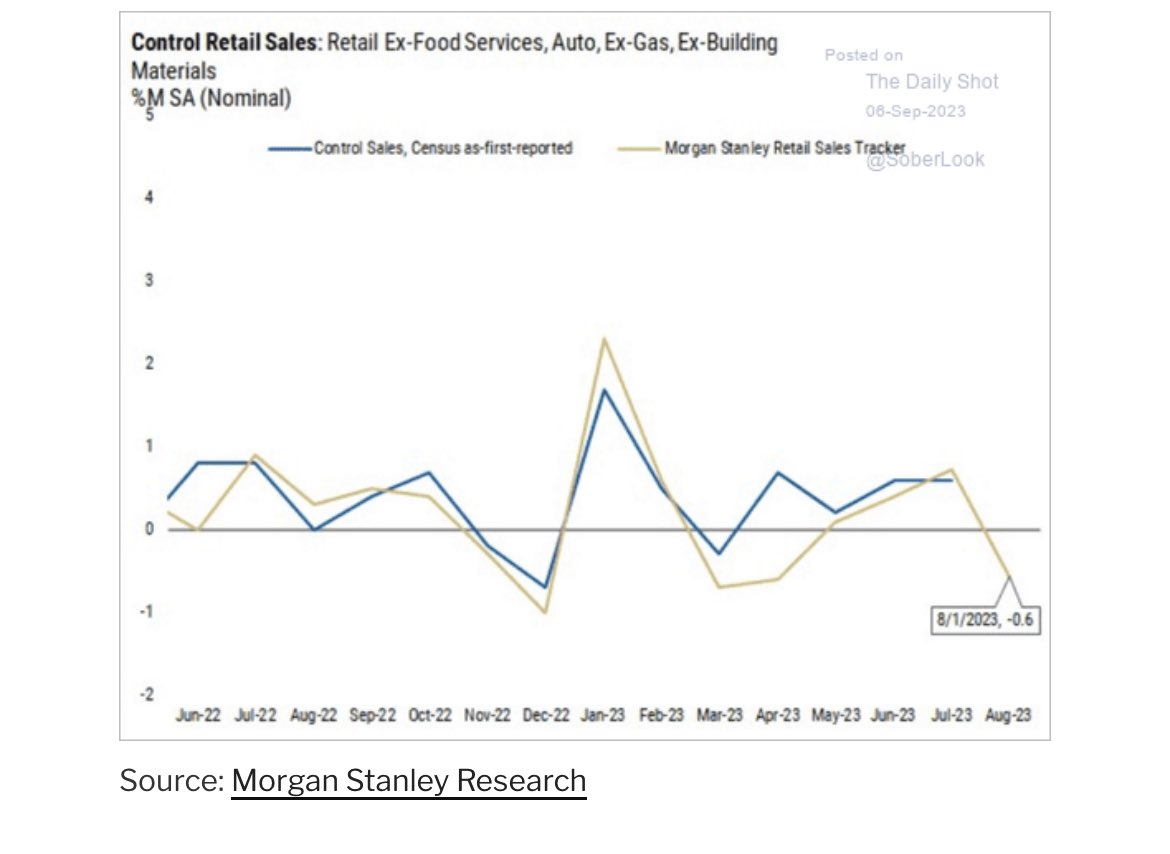

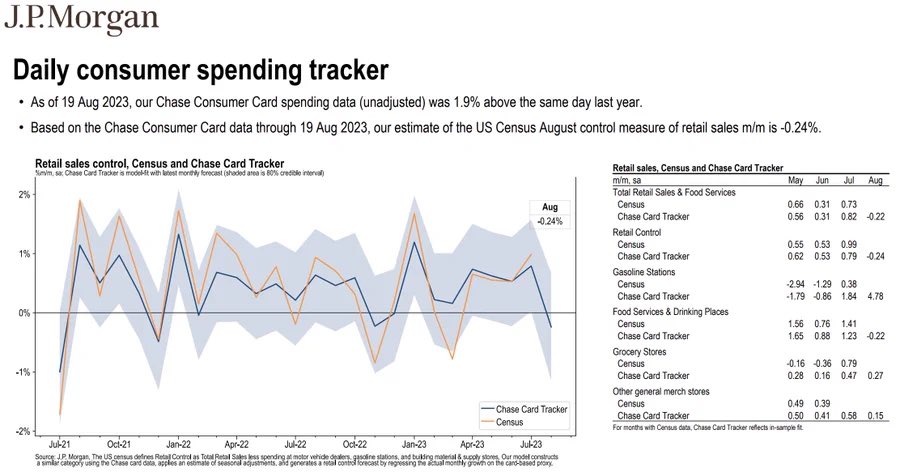

- Based on Chase consumer card data through Aug 29, JPM’s estimate for Aug control group retail sales is a big step down to -0.49% from a boomy 0.99% in July (Census figure; JPM’s estimate for July is 0.79%). (@Econ_Parker)

- Health-Insurance Costs Are Taking Biggest Jumps in Years Employers and workers are expected to see an increase of about 6.5% or higher in the cost of their health plans next year.

- GM offers 10% wage hike in contract talks that UAW calls ‘insulting’

The largest U.S. automaker said it offered workers a 10 per cent wage hike and two additional 3 per cent annual lump sum payments over four years in its offer to the union ahead of the Sept. 14 contract expiration.

It is also offering a $6,000 one-time inflation-related payment and $5,000 in inflation-protection bonuses over the life of the agreement, along with a $5,500 ratification bonus.

GM said that under its offer, current temporary employees will receive a 20 per cent increase to $20 per hour wage and it would shorten the time it takes to get to the maximum wage rate for permanent employees – mirroring proposals from Ford.

Last week, Ford said it had offered a 9 per cent wage increase through 2027 and 6 per cent lump sump payments, much less than the 46 per cent wage hike being sought by the union. The UAW has said 97 per cent of members voted in favor of authorizing a strike if agreement is not reached.

(…)The union’s demands include a 20 per cent immediate wage increase followed by four 5 per cent annual wage hikes, defined-benefit pensions for all workers, 32-hour work weeks and additional cost of living hikes. GM is proposing to give employees an additional paid holiday.

The UAW also wants all temporary workers at U.S. automakers to be made permanent, seeks enhanced profit sharing and the restoration of retiree health-care benefits and cost-of-living adjustments.

The UAW said Ford’s profit-sharing formula change would have cut payouts by 21 per cent over the last two years. (…)

Canada Rate Policy Might Be ‘Sufficiently Restrictive,’ Gov. Tiff Macklem Says Bank of Canada Gov. Tiff Macklem said higher interest rates are suppressing consumption and dampening price increases, and might be at “sufficiently restrictive” levels for the central bank to achieve its 2% inflation target.

(…) “Excess demand in the economy has diminished substantially,” due to higher interest rates, Macklem said. “With past interest rate increases still working their way through the economy, monetary policy may be sufficiently restrictive to restore price stability.” (…)

Macklem said softening consumer spending was most pronounced on furniture and other durables often bought on credit.

Together with a fifth-straight quarterly decline in housing investment, “this points to the moderating effect higher interest rates are having on household spending,” Macklem said in his speech. He said the central bank also sees signs of slowing in the labor market from “overheated” levels, noting employment gains have lagged behind population growth for five of the last six months and job vacancies are down by about a quarter from their peak last year.

The unemployment rate has climbed by a half-point, to 5.5%, in the past three months. Macklem said annual wage growth between 4% to 5% remained elevated, although he added he expects those pay increases to slow as well.

Macklem said “inflation is still too high, and the downward momentum [on prices] is slow. And we are concerned that there’s a certain stubbornness in the stickiness of inflation.” (…)

US bank profits, deposits broadly steady as spring turmoil abates – FDIC

Overall industry profits in the second quarter fell 11.3% year-on-year to $70.8 billion, driven by the acquisitions of Silicon Valley Bank and two other large lenders which failed from March to May after depositors yanked their cash. Stripping out those rescue deals, profits were up 5.7% from the prior year.

While deposits declined for the fifth quarter in a row, they were down just 0.5% compared with a record 2.5% decline in the first quarter. That was driven by a decline in uninsured deposits, while insured deposits actually rose again in the second quarter by 0.8%. (…)

Unrealized losses on securities increased 8.3% in the second quarter, rising to $558.4 billion, the FDIC said, although that increase comes after banks had reporting declining unrealized losses for two straight quarters.

“Despite the period of stress earlier this year, the banking industry continues to be resilient,” FDIC Chairman Martin Gruenberg said in a statement.

“However, the banking industry still faces significant challenges from the effects of inflation, rising market interest rates and geopolitical uncertainty.” (…)

The FDIC’s “problem bank” list was unchanged at 43 firms in the second quarter. (…)

U.S Treasuries yielded 3.8% at the end of June and 4.0% on July 31. Now: 4.25%.

KKR reckons that U.S. banks had nearly $700B of unrealized bond losses at July 31 and suggests that “these holders will likely sell quickly if prices do rally back”.

Apple Becomes the Biggest U.S.-China Pawn Yet Few companies are safe if the iPhone maker isn’t immune to China’s retaliation.

The Wall Street Journal reported on Wednesday that the Chinese government is banning the iPhone and other foreign-branded devices from use by workers at central government agencies. Bloomberg reported Thursday that such a ban might also be extended to state-owned enterprises and other government-backed entities. That could amount to a significant swath of people in a state-led economy with a population totaling more than 1.4 billion.

According to China’s National Bureau of Statistics, about 56.3 million urban workers were employed by “state-owned units” in 2021. Those jobs commanded an average wage about 8% above the national urban average—an attractive segment for a company specializing in premium devices. And because Apple now ships roughly 230 million iPhones globally every year, 56 million would be a notable chunk to take out of the pool of potential buyers—especially in a mature global smartphone market with low growth prospects. (…)

China has at least some interest in not overly harming a major local employer during a time of growing unemployment. One Chinese city alone reportedly has more than one million workers building Apple products or employed in related jobs. (…)

The recent developments are also just the latest challenge Apple has faced in the country that now serves as its third-largest geographical segment, accounting for 19% of the company’s total revenue in the 12-month period ending in June.

Apple’s sales in its Greater China segment also generated pretax operating margins that were 12 percentage points higher than the company’s total during its most recent fiscal year. (…)

But China is still the company’s largest manufacturing base by far. And the iPhone is still Apple’s largest business, accounting for 52% of revenue. That ironically makes Apple a relatively easy target in the economic war between the U.S. and China. (…)

China has also deployed other creative punishments for U.S. firms, such as withholding approval on major mergers and acquisitions, throwing a wrench into growth plans for major U.S. semiconductor companies such as Qualcomm, Intel and Applied Materials.

Throwing a rock at Apple also creates major ripples across the tech pond. The company is one of the world’s largest buyers of chips for its devices. (…)

Stocks vs bonds

@TaviCosta

-

Unit Labor Costs Revised Up (GS)

Nonfarm productivity was revised down by 0.2pp in Q2 to +3.5% (qoq ar) and the year-over-year rate was unrevised at +1.3%. Since 2019Q4, labor productivity has grown at an annualized rate of 1.4%, roughly in line with the pre-pandemic trend.

Unit labor costs—compensation divided by output—were revised up by 0.6pp in Q2 to +2.2% (qoq ar), and the year-over-year rate was revised up by 0.1pp to +2.5%.

Compensation per hour was revised up by 0.2pp to +5.7% in Q2 (qoq ar), and the year-on-year rate was revised up by 0.1pp to +3.8%. Our wage tracker now stands at +4.4% year-over-year in Q3 (vs. +4.8% in Q2).

Total business sales growth turned negative in March They were -3.1% YoY in June while ULC rose 2.5% in Q2 when pretax profits dropped 9.3%.

Here’s a close up view:

Andrew Ng: Opportunities in AI – 2023

Two of our sons are true geeks who try to keep me abreast of tech stuff. The link above will take you to a 36 minutes presentation that I found quite instructive.

BTW, if any of you have smart ideas in search of Ai brains to execute, Danny can help you (bld.ai)