SERVICES PMIs

Note: The U.S. PMI will be out later today.

Eurozone economy contracts at faster pace in August as services activity tips into decline

The HCOB Eurozone Services PMI Business Activity Index fell below the no-change mark of 50.0 in August to 47.9, from 50.9 in July and indicating the first decline in activity since December 2022. Moreover, the rate of contraction was the fastest since February 2021.

The four largest eurozone economies all posted declines, led by France and Germany. Italy and Spain registered only marginal contractions while Ireland posted a solid, albeit slower, increase in services output.

The volume of new business fell for the second month running, and at the fastest pace since February 2021. Demand for services has now contracted eight times since the second half of 2022.

As was the case for total activity, France and Germany were the main drivers of weakness in August. New export business (including intra-eurozone trade in services) fell for the third month running, and at a faster rate.

Looking ahead, expectations for business activity remained positive, although the degree of optimism was unmoved from July’s 2023 low.

With new contracts at service providers drying up in August, the level of incomplete business continued to fall. The rate of contraction was the strongest in two-and-a-half years. This led to greater caution around hiring as employment in the services sector rose at the slowest rate since February 2021, the first month of the current upturn. Italian service providers cut staff for the second month running.

Input prices at service providers rose at the fastest rate in three months in August, and one that remained above the long-run survey average. The prime suspect is likely the wage hikes, which are not necessarily in sync with the business cycle, given their often longer term nature. That said, cost pressures remained well down on the record highs seen in 2022. Inflation of prices charged for services eased to a 23-month low, but remained very high in Germany in particular.

China: Service sector expansion slows in August

China: Service sector expansion slows in August

At 51.8 in August, the seasonally adjusted headline Caixin China General Services Business Activity Index slipped from 54.1 in July to signal a modest increase in activity. (…)

The slowdown in business activity coincided with a weaker increase in overall new business. New orders increased modestly, and at a pace that was below the average seen for 2023 to date. Data suggested that this was partly due to weaker foreign demand for Chinese services.

New export business fell for the first time since December 2022, albeit marginally, amid reports of sluggish overseas market conditions.

Although growth momentum slowed, companies continued to add to their staffing levels during August. The rate of job creation was little-changed from July and modest, amid reports of higher business requirements and plans to expand capacity. (…)

Outstanding business meanwhile accumulated further in August, despite the sustained rise in headcounts. Companies often mentioned that backlogs of work had increased due to greater amounts of new orders and subsequent pressure on capacity. Though modest, the rate of accumulation was the most pronounced since January.

Cost pressures continued to ease in August, with average input costs across China’s service sector increasing at the softest pace in six months. Higher operating expenses were generally linked to increased raw material, staff and fuel costs.

Competitive market pressures dampened the overall pricing power of Chinese service providers in August, with output charges increasing only slightly. Furthermore, the rate of inflation was the weakest seen since April.

THE CHINA SYNDRONE (CONTINUED)

China’s economic problems are now well known having reached page one just about everywhere. Looking for solutions needs a proper assessment of the debt challenge:

Of the 25 provinces that have released audit reports of their 2022 budgets, 80% had mismanaged bond funds, according to an analysis by Sinolink Securities Co. analysts led by Zhao Wei. The problems include insufficient project preparation, misuse of the bond proceeds and money granted being left unused.

The slow rollout of the funds is one of the “clogging points in stabilizing growth” cited in the provincial reports, the analysts wrote in a note on Wednesday. “And problems in the management of special bond funds and insufficient project preparation are likely key reasons for the slow use of the funds.”

Beijing has been putting pressure on local governments to speed up special bond sales in order to boost infrastructure spending and offset the slump in property and private sector investment. Officials set a September deadline for provinces to issue all of this year’s 3.8 trillion yuan ($520 billion) quota of new special bonds, and instructed them to put the cash into use by the end of October.

The findings from the auditors show the limitations of that approach, with provinces increasingly unable to find good enough projects to invest in. (…)

The audit reports also showed how high debt levels are impeding local governments’ ability to spend. (…)

- Why China Has a Giant Pile of Debt A major lender abroad, China is facing a debt bomb at home: trillions of dollars owed by local governments, their financial affiliates, and real estate developers.

From the NYT on July 8, 2023.

(…) Researchers at JPMorgan Chase calculated last month that overall debt within China — including households, companies and the government — had reached 282 percent of the country’s annual economic output. That compares with an average of 256 percent in developed economies around the world and 257 percent in the United States. (…)

The steep increase in China’s debt, more than doubling compared with the size of its economy since the global financial crisis 15 years ago, makes managing it harder. (…)

The real estate and government debt problems overlap. For many years, the main source of revenue for localities came from the sale to developers of long-term leases for state land. As many private-sector developers have run out of money to bid for land, this revenue has fallen. The local financing affiliates have instead done the heavy borrowing to buy the land that such developers could no longer afford, at steep prices. As the real estate market continues to weaken, many of these financing affiliates are in trouble. (…)

Fitch Ratings, the credit rating agency, estimates that local governments have debts equal to about 30 percent of China’s annual economic output. Their affiliated financing units owe debt equal to an additional 40 to 50 percent of national output — although there may be some double counting as local governments borrow and then shift the debt to their financing units, Fitch said. (…)

As its economy slows, a growing number of local governments and their financing units are unable to keep paying interest on their debts. The ripple effect means many localities lack money to pay for public services, health care or pensions. (…)

China’s domestic debt overhang defies quick fixes. The country needs to gradually move away from debt-fueled government construction projects and heavy national security spending, toward an economy based more on consumer spending and services. (…)

- China’s hidden local government debt soars to over $8tn Surge in borrowing, weak land sales leave half of cities struggling to pay interest

From Nikkei Asia on June 15, 2023

A measure of the off-the-books debt of Chinese local governments swelled by half between 2019 and 2022, amid shrinking revenue and heavy borrowing to pay for economy-supporting infrastructure projects.

Debt held by local government financing vehicles (LGFVs) totaled 59 trillion yuan ($8.25 trillion) at the end of last year, according to a recent report from the Rhodium Group.

LGFVs serve as an alternative funding route for cash-strapped local authorities, which the government restricts from raising capital through means other than bonds. They are generally considered to be implicitly guaranteed by local governments, and as such a form of hidden debt.

In addition to funding public works projects, these investment companies have been used to buy state-owned land as actual real estate demand softens, padding revenue but at the same time adding to hidden debt loads.

Observers see reducing these burdens as crucial to heading off broader financial turmoil. But addressing the problem would require a shift in the development model that has driven growth at the local level, potentially further burdening China’s economy.

According to China’s Finance Ministry, local governments had 35 trillion yuan in outstanding on-the-books debt at the end of 2022, including regular bonds and special-purpose bonds for funding infrastructure projects. Adding debt from LGFVs brings the total to nearly 100 trillion yuan, or almost 80% of China’s nominal gross domestic product. (…)

Rhodium calculated the ratio of individual cities’ interest payments on hidden and on-the-books debt to their revenue from official sources and LGFVs, with 10% as the threshold indicating that their debt has become difficult to service.

About half of the 205 cities with financial data available breached that warning line last year, up from one-third in 2021. (…)

From Reuters on August 7, 2023

(…) Local governments are fundamental to China’s economy, with Beijing tasking provincial and city officials with meeting ambitious growth targets. But after years of over-investment in infrastructure, plummeting returns from land sales and soaring COVID costs, economists say debt-laden municipalities now represent a major risk to China’s economy.

Chinese leaders last month pledged, without detailing, to help ease their debts, signalling worries over a potential chain of municipal debt defaults destabilising the financial sector.

Economists took that message as being more constructive than in April, when Communist Party leaders demanded “strict control” of local debts. The implication, they say, is that Beijing has realised it needs to urgently throw cash at the problem.

That could represent a major breakthrough in finding a way out of China’s municipal debt crisis, with Beijing having for years demanded that local administrations sort themselves out. (…)

The extent of any central government involvement, and any conditions attached to it, are still subject to debate, two policy advisers told Reuters. Whether the package of measures will be a short-term or multi-year plan also remains unknown.

These details will be key for investors to gauge how decisive and long-lasting Beijing’s solution will be. (…)

It is an unsustainable situation that puts Beijing in a bind: provide no help and the economic model unravels with severe consequences on growth and social stability, or step in at the risk of encouraging more reckless spending.

“A principle should be established: not all debt will be assumed by the central government,” a policy adviser told Reuters on condition of anonymity.

“This could lead to moral hazard.”

To avoid that risk, the adviser suggested all stakeholders bear some of the burden: financial institutions, local governments, Beijing and society at large. (…)

“Extension of local government and LGFV debt and de facto restructuring, especially with banks, will likely be encouraged, while local governments may also be pushed to sell or mortgage some assets,” said Tao Wang, chief China economist at UBS.

Then comes frugal Beijing, which has most room for manoeuvre, with a central government debt of only 21% of GDP.

Beijing issued 1 trillion yuan in special bonds in 2020 to cope with the pandemic, 1.55 trillion in 2007 to recapitalise its sovereign wealth fund and 270 billion yuan in 1998 to recapitalise the “big four” state banks.

“The central government can issue low-cost bonds to replace local debt,” a second policy adviser said.

China’s 10-to-30-year government bonds yield 2.7%-3.0%. Some cities and LGFVs pay 7-10% interest. (…)

For the local debt problem to stop re-occuring policymakers need to implement profound changes to how the economy works. (…)

But ultimately Beijing, and the Chinese society, may have to accept lower growth after four decades of expansion at a staggering pace.

“Whether Beijing will be able to accept a significant slowdown in local government investment, and therefore economic growth, will be one of the most important questions in any restructuring,” Rhodium’s Wright said.

Coincidentally, John Authers’ today’s column discusses China:

The drumbeat of major news headlines from China on an almost daily basis seems all but to spell doom for the world’s second-largest economy. After decades of growth far in excess of anything in the developed world, the picture looks troubled. Rebecca Choong Wilkins and Colum Murphy put it succinctly in this Big Take piece: “The $18 trillion economy is decelerating, consumers are downbeat, exports are struggling, prices are falling and more than one in five young people are out of work.” (…)

China has converged with the US economy in a way it had hoped to avoid. As this chart from Björn Jesch, global chief investment officer at DWS Investment shows, China’s debt to GDP ratio has now overtaken the US, while its growth rate is also converging. (…)

It is China’s debt, more than anything else, that is arousing concern, and dividing opinon. Diana Choyleva of Enodo Economics, a long-time China-watcher, made this scathing assessment after reviewing projections for credit losses:

The numbers are a shocker. We estimate credit losses at between 37% and 42% of GDP, up from 26%-31% last year. The Party-state faces its biggest clean-up operation in the most challenging of times. Looking at impairment rates by sector, it is noteworthy that IT is most at risk , surpassing real estate whose woes are well understood. This is not only a reflection of the fact that Xi Jinping managed to bring China’s tech giants to heel, hurting their bottom line, but also a serious worry for the leadership’s technology ambitions for China.

(…)

Russian and Saudi Oil-Production Cuts Flash Warning on Chinese Economy An extension of oil-production cuts by Russia and Saudi Arabia hardened Wall Street fears that the Chinese economy has hit a rough patch.

Russia and Saudi Arabia surprised many investors by curtailing output through the end of the year, pushing oil prices to their highest levels of 2023. Benchmark U.S. crude gained more than 1.3%, closing at $86.69 a barrel. (…)

On Tuesday, private-sector data showed the slowest expansion in China’s services output in eight months, while an official gauge of manufacturing activity last week indicated a fifth-straight month of contraction.

The country’s oil demand remains high by historical standards, said Ole Hansen, head of commodity strategy at Saxo Bank. But if prices continue to rise, he said, Beijing could protect domestic companies by digging into its crude reserves instead of purchasing crude on the open market. (…)

IEA via The Market Ear

- Meanwhile, US crude oil field production jumped to 12.8 mbd at the end of August (Ed Yardeni).

Soaring Dollar Raises Alarm as China, Japan Escalate Pushback

Japan issued its strongest warning in weeks against rapid declines in the yen on Wednesday, with its top currency official saying the nation is ready to take action amid speculative moves in the market. Shortly after, China’s central bank offered the most forceful guidance on record with its daily reference rate for the yuan, as the managed currency weakened toward a level unseen since 2007. (…)

Resilient US economic data is persuading some traders that the Federal Reserve will keep interest rates higher for longer, sending the dollar jumping and a gauge of Asian currencies toward the lowest since November. That means policymakers in the region, who spent last year burning through their reserves to support local currencies, are heading back to the battlefield to take on bearish speculators. (…)

Elevated oil prices have also reignited fears over higher inflation, a move that’s undermining expectations Asian central banks were done hiking interest rates and hurting the appeal of local-currency bonds. Bonds in Indonesia and Thailand are both seeing foreign outflows this month.

China’s dire economic outlook, which was built on data that have been disappointing for months, is also weighing on sentiment on emerging-market currencies. (…)

“The immediate implication of the soaring US dollar is that it will prevent most Asian central banks from loosening monetary policy, out of fear of aggravating currency weakness,” said Alvin T. Tan, head of emerging-market currency strategy at RBC Capital Markets in Singapore.

China’s auto workers bear the brunt of price war as fallout widens

As Shanghai sweltered in a heatwave in June, the car factory where Mike Chen works switched production to night shifts and dialled down the air-conditioning.

For Chen, toiling through the early hours in his sweat-soaked uniform, it was the latest slap in the face after cuts in bonuses and overtime slashed his monthly pay this year to little more than a third of what he earned when he was hired in 2016.

Chen, 32, who works for a joint venture between China’s state-owned car giant SAIC (600104.SS) and Germany’s Volkswagen (VOWG_p.DE), is far from alone. Millions of auto workers and suppliers in China are feeling the heat as an electric vehicle price war forces carmakers to shave costs anywhere they can. (…)

The price war triggered by Tesla (TSLA.O) has sucked in more than 40 brands, shifted demand away from older models and forced some automakers to curb production of both EVs and combustion-engine cars, or shut factories altogether.

Reuters interviews with 10 executives of carmakers and auto parts suppliers, as well as seven factory workers, point to a broader industry in distress, with penny-pinching on everything from components to electricity bills to wages – which is in turn hitting spending elsewhere in the economy. (…)

Economists warn that China’s auto sector could even become a drag on economic growth because of the fallout from the price war, which would be a stark turnaround for a car industry that is by far the world’s biggest.

The problem is that while there has been huge investment in production capacity, helped by large state subsidies, domestic demand for cars has stagnated and household incomes remain under pressure, economists say.

In the first seven months of 2023, China sold 11.4 million cars at home and exported 2 million, but growth came almost entirely from abroad. Exports leapt 81% but domestic sales only crept 1.7% higher – despite the widespread price cuts. (…)

“China really has to learn to walk on two legs.” (…)

Including factories making combustion-engine cars, China had the capacity to produce 43 million vehicles a year at the end of 2022, but the plant utilisation rate was 54.5%, down from 66.6% in 2017, China Passenger Car Association (CPCA) data show.

At the same time, pay cuts and lay-offs in the auto industry and its suppliers – which employ an estimated 30 million people according to Chinese state media – are hitting living standards at a time when Beijing desperately wants to lift consumer confidence from near record lows.

Cutting salaries is illegal in China, but complex pay structures offer ways around this.

SAIC-VW, for example, was able to reduce Mike Chen’s take-home pay by reducing working hours and cutting bonuses, without tinkering with his base pay, which typically covers up to half the compensation workers expect when they join. (…)

A Reuters analysis of the estimated income included in recent job adverts from 30 auto firms showed hourly salaries of 14 yuan ($1.93) to 31 yuan ($4.27), with Tesla, SAIC-GM, Li Auto (2015.HK) and Xpeng (9868.HK) at the higher end. (…)

Several automakers including Mitsubishi Motors (7211.T) and Toyota (7203.T) have laid off thousands in China after sales slumped. Others such as Tesla and battery maker CATL (300750.SZ) have slowed hiring as they delayed expansions. Hyundai (005380.KS) and its Chinese partner, meanwhile, are trying to sell a plant in Chongqing. (…)

State-run China Automotive News estimates there are over 100,000 auto suppliers in the country. In a March survey of nearly 2,000 by auto parts trading platform Gasgoo, 74% said automakers had asked them to reduce costs.

More than half were asked for reductions of 5% to 10%, higher than the 3% to 5% targets of previous years. Nine out of 10 companies expected more such requests this year.

Suppliers typically negotiate prices once a year, but many have been pressed to lower prices on a quarterly basis in 2023, two senior executives at auto suppliers said.

Before it kicked off the price war, Tesla sent emails to its direct suppliers, encouraging them to lower costs by 10% this year, according to a person with direct knowledge of the matter. (…)

The EV battery market has also turned, with suppliers cutting prices for automakers. CATL, which counts Tesla as its biggest client, offered smaller domestic EV makers discounted batteries in February.

Lithium iron phosphate (LFP) batteries, the type used by Tesla in China, were 21% cheaper in August than five months ago, while nickel-cobalt batteries were 9% to 18% cheaper, RealLi Research data show. (…)

The US still lags behind much of Europe and Asia in returning to the office as stark differences emerge between countries, cultures and companies.

- Remote work is working well for many Americans. The proportion who said their productivity was at optimal levels is almost double that in the rest of the world, INSEAD research shows.

- Missing out on social connections through work is more of a concern for employees in Asia and Europe than it is for Americans.

China Bans iPhone Use for Government Officials at Work The directive is the latest step in Beijing’s campaign to cut reliance on foreign technology and could hurt Apple’s business in the country.

World’s hottest summer

World’s hottest summer

The unmistakably large jump in meteorological summer’s global average surface temperature compared to past years is a telltale reflection of deadly heat waves and record-warm oceans.

According to preliminary data from the Copernicus Climate Change Service’s ERA5 data set, the global average surface temperature for June through August was about 1.17°F above the 1991-2020 average.

- This beat the previous record-hot summer of 2019 by nearly 0.54°F.

- June and July were each record-hot months. July ranked as the warmest month since the dawn of the instrument era in the 19th century.

Data: ECMWF/ERA5 via Brian Brettschneider. Chart: Axios Visuals

Globally, Australia had its warmest winter since reliable records began there in 1910. All-time winter heat records were set in multiple locations in South America, from Brazil to Chile.

- Europe saw repeated, scorching heat waves that broke all-time seasonal records in Spain, France, Italy, Greece and Switzerland.

- In Tokyo, daytime highs rose above 86°F every day during August — a first for any month since data began there in 1875.

- In Japan, August was the hottest month on record.

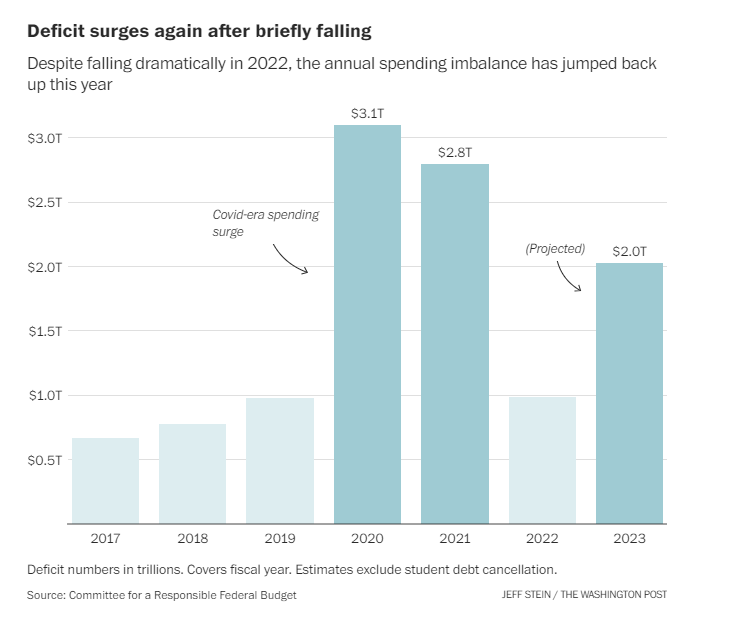

Federal funding continues to flow from President

Federal funding continues to flow from President

Source:

Source:

{kind=link}