Jobless Claims Nearing New Highs

Jobless claims have continued to weaken with this week’s release, rising by 5K to 245K versus expectations of no change from last week’s upwardly revised 240K print. At current levels, claims sit at the high end of the range since the start of 2022 and only a couple thousand below last month’s high.

Philly Fed April 2023 Manufacturing Business Outlook Survey

The diffusion index for current general activity decreased 8 points to -31.3 in April, its eighth consecutive negative reading and lowest reading since May 2020. Although most firms reported no change in activity (59 percent), the share of firms reporting decreases (35 percent) exceeded the share of firms reporting increases (3 percent).

The indexes for new orders and shipments both remained negative but increased this month: The new orders index rose 6 points to -22.7, and the shipments index climbed 18 points to -7.3. Almost 28 percent of the firms reported decreases in shipments (down from 31 percent last month) compared with 20 percent that reported increases (up from 6 percent last month).

On balance, the firms reported mostly steady levels of employment. The employment index rose 10 points to a near-zero reading. Similar shares of the firms reported increases and decreases in employment (16 percent); most firms (67 percent) reported no change. The average workweek index rose from -22.0 to -8.4.

In this month’s special questions, the firms were asked about changes in wages and compensation over the past three months, as well as their updated expectations for changes in various input and labor costs for the current year.

More than 55 percent of the firms indicated wages and compensation costs had increased over the past three months, 45 percent reported no change, and none reported decreases. Most firms (58 percent) have reported not needing to adjust their 2023 budgets for wages and compensation since the beginning of the year; however, almost 33 percent noted they are planning to increase wages and compensation by more than originally planned, and 10 percent noted they are planning to increase wages and compensation sooner than originally planned.

The firms still expect cost increases across all categories of expenses in 2023, and the median expected increases were in line with or slightly lower than expectations for most categories when this question was last asked in January. Responses indicate a median expected increase of 3 to 4 percent for wages, down slightly from 4 to 5 percent from January, and of 4 to 5 percent for total compensation (wages plus benefits), unchanged from January.

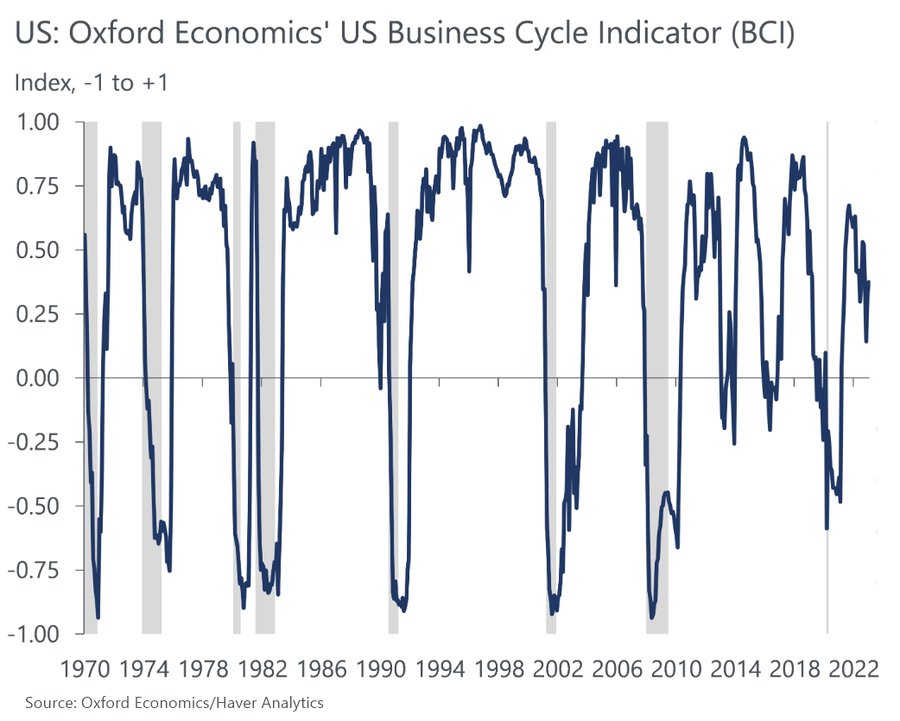

Rosenberg Research has another chart saying we’re supposed to be in recession:

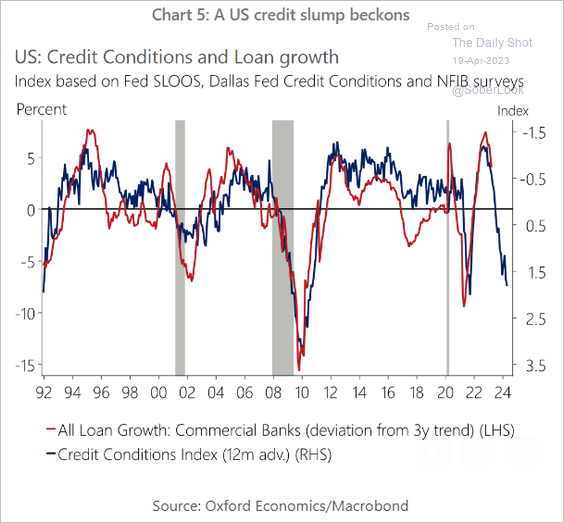

No doubt about housing:

Home Prices in March Posted Biggest Annual Decline in 11 Years Home sales fell in March, a sluggish start to the crucial spring selling season as higher mortgage rates damped momentum from the previous month.

U.S. existing-home sales decreased 2.4% in March from the prior month to a seasonally adjusted annual rate of 4.44 million, the National Association of Realtors said Thursday. March sales fell 22% from a year earlier.

March marked the 13th time in the previous 14 months that sales have slowed. The housing market had a surprisingly strong February, when sales rose a revised 13.75% from the previous month. But after mortgage rates ticked higher, March sales resumed the extended period of declines. (…)

The national median existing-home price decline of 0.9% in March from a year earlier to $375,700 was the biggest year-over-year price drop since January 2012, NAR said.

Median prices, which aren’t seasonally adjusted, were down 9.2% from a record $413,800 in June. Home prices in the western half of the U.S. experienced some of the biggest gains for many years but are now falling the fastest. (…)

Home prices are declining the most in the West. But in other parts of the country, prices are still rising from a year earlier because inventory of homes for sale is unusually low for this time of year. (…)

Nationally, there were 980,000 homes for sale or under contract at the end of March, up 1% from February and up 5.4% from March 2022, NAR said. (…)

The number of homes for sale is up from a year ago because houses are sitting on the market longer. But the number of new listings in March fell 20% from a year earlier, according to Realtor.com.

Housing starts, a measure of U.S. home-building, fell 0.8% in March from February, the Commerce Department said this week. Residential permits, which can be a bellwether for future home construction, dropped 8.8%. (…)

Advisor Perspectives plots actual home sales and population-adjusted sales:

Auto Dealers Feel the Squeeze Lithia and AutoNation add to the drumbeat of bad news for the business of selling cars

(…) AutoNation said on Thursday that on a same-store basis, it sold 2.8% fewer new vehicles and 17.5% fewer used cars in the first quarter compared with a year earlier. Lithia Motors on Wednesday said it sold 6.3% fewer new vehicles and 2.4% fewer used vehicles over the same period. Cars are sitting on lots for longer as a result: Lithia said there were about 52 days of supply of new vehicles in the first quarter, up from 47 days a quarter earlier. AutoNation is carrying 25 days’ worth of new vehicle supply, up from 19 days from the prior quarter. (…)

Fed Officials Back Another Hike While Watching Banking Fallout More hawkish comments despite strains in the banking industry.

Cleveland Fed President Loretta Mester, typically among the more hawkish of policymakers, said she favored getting rates above 5% because inflation was still too high. (…)

Atlanta Fed President Raphael Bostic, asked if he stilled backed a “one and done” rate-hike approach, said “it is my view,” and noted that policy works with a lag.

“Once we get to this point, we’ll have moved firmly into restrictive space. And then I think it’s time for us to let the restrictive action work its way through. And that will take some time,” he said.

Neither he nor Mester vote on monetary policy this year.

Philadelphia Fed chief Patrick Harker, who does vote on the policy-setting Federal Open Market Committee in 2023, had a similar message.

“I anticipate that some additional tightening may be needed to ensure policy is restrictive enough to support both pillars of our dual mandate,” he told an event organized by the Wharton School of the University of Pennsylvania in Philadelphia later on Thursday evening.

“Once we reach that point, which should happen this year, I expect that we will hold rates in place and let monetary policy do its work,” Harker said in his prepared remarks. (…)

“I expect to see tighter credit conditions for households and businesses that may slow economic activity and hiring,” Harker said. “But the full extent is still unclear.”

Another 25bps hike will immediately increase funding costs further. There will be pain, blood for some.

This chart plots corporate debt level, business sales and inflation, all indexed at 100 on December 2013.

Observations:

- Four years after ZIRP, corporate debt exploded 80%, far above business sales growth of 37%.

- Business sales had flattened in 2018’H2 through the end of 2019 while inflation was creeping up.

- The pandemic money smorgasbord boosted sales 30% but debt level nonetheless rose 13%.

- It also fueled 17% inflation.

Now, sales are flattening again while inflation and debt keep rising.

Corporate debt is now 7.1% of sales, up 30% from 5.4% at the end of 2013.

The cost of debt, measured by the bank prime rate, was 3.2% in 2013. It’s now 8%. Simplistic math says that financing cost could now be 10.2% of sales, from 3.2% in 2013. Goldman Sachs says that funding costs for mixed capital structures (bonds-loans) are now 7%, up from 4.8% in 2022.

(BTW, Lithia Motors and AutoNations’ floor plan interest expenses last quarter were more than five times what they were a year earlier. (WSJ))

That economy-wide squeeze may not transpire into profit margins (inversed scale on chart above) just yet because much debt was fixed but financing costs will surely explode upon refinancing in coming quarters/years.

The pandemic boosted corporate margins but sticky wages and rising financing costs could narrow the unusually wide gap between debt/sales and margins in coming years. No wonder CFOs are actively cutting costs, they see their refinancing schedules. American corporations will be particularly challenged by maturing debt costs through 2025.

(Data: S&P GLobal)

GavekalResearch:

Investors are waking up to how in the last boom most of the excesses took place in the US. Over the past 15 years or so, capital in the US was both very cheap and easily accessible, whereas in Japan and Europe, while capital was cheap, banks weren’t exactly lending hand over fist, and in most emerging markets capital was never stupidly cheap nor easily accessible. It stands to reason therefore that if capital was wasted, it was most likely wasted in the US.

So if you agree that handing out cheap and plentiful money is the financial equivalent of giving adolescent boys fast cars and free whiskey, you will not be surprised if, as the price of capital rises, most of the financial accidents take place in the US. Purely on anecdotal evidence, it does feel as if most of the stupidity of recent years—Theranos, FTX, GameStop, Bed Bath & Beyond—was a US phenomenon.

Ratings firms are on track to cut the most US corporate bonds to junk since the early part of the pandemic, further boosting funding costs for some companies just as economic growth is slowing.

In the first quarter, a total of $11.4 billion of bonds were downgraded to high yield status, a figure that’s about 60% of 2022’s full-year total, according to Barclays Plc research. Full-year volume is on pace to be the highest since 2020 when the pandemic sparked a massive wave of downgrades, according to the bank’s estimates. (…)

Barclays expects downgrades to junk status to accelerate in the second half of the year as slowing economic growth puts additional strain on blue-chip borrowers. The bank this year expects between $60 billion and $80 billion of these securities known as fallen angels, according to a note by strategists led by Dominique Toublan. (…)

Flash Eurozone PMI hits 11-month high amid resurgent service sector activity

The seasonally adjusted HCOB Flash Eurozone Composite PMI Output Index, based on approximately 85% of usual survey responses, rose for a sixth consecutive month in April, up from 53.7 in March to 54.4, its highest since May of last year. The latest reading indicated a fourth consecutive month of growth with the rate of expansion having accelerated throughout the year to date, contrasting with the six-month period of decline seen in the second half of 2022.

Growth became increasingly uneven in April, however, with the service sector reporting its strongest expansion for a year whereas manufacturing output contracted at the sharpest rate since December, falling back into decline after two months of marginal growth. The resulting outperformance of services relative to manufacturing was the widest seen since early-2009, and the survey has not yet previously recorded such a strong service sector expansion at a time of manufacturing decline.

The improved performance was driven in part by faster growth of new orders. Measured across manufacturing and services, new orders rose for a third successive month in April, expanding at the steepest rate since May 2022. However, while growth of new business in the service sector hit the highest since April 2022, new orders in the manufacturing sector fell at the steepest rate for four months.

Order book growth nevertheless lagged that of output, the relatively faster pace of output growth being supported by companies fulfilling orders placed in prior months, causing backlogs of work to fall, albeit exclusively in manufacturing.

Whereas falling backlogs in factories point to lower manufacturing production requirements in coming months, an increase in backlogs in the service sector indicates a shortage of operating capacity. Hence employment growth in manufacturing slowed to the lowest seen over the past 27 months, but service sector jobs growth picked up to the fastest since July 2007. The resulting overall increase in employment was the largest for 11 months.

Inflation trends also varied markedly by sector. Input costs in the goods producing sector fell for a second straight month and at the sharpest rate since May 2020, pulled lower by reduced costs for energy in particular as well as for a wide variety of other inputs. In contrast, service sector input costs continued to rise sharply, the rate of increase remaining elevated, often linked to higher staff costs. Service sector input cost inflation nevertheless moderated slightly to the lowest since October 2021. Measured across goods and services, input cost inflation consequently sank to the lowest since February 2021, cooling for a seventh straight month yet remaining well above the survey’s long-run average.

Average prices charged for goods and services also continued to rise at a pace well above the survey’s long-run average, though the rate of increase moderated sharply to the lowest for two years. Despite hitting a 15-month low, service sector charge inflation remained especially strong and higher than anything recorded by the survey prior to the pandemic. But manufacturing charges rose only modestly, registering the smallest increase since November 2020, the rate of inflation having eased sharply from the strong pace seen at the start of the year. (…)

Finally, optimism about the year ahead dipped further from February’s 12-month high, down slightly in both manufacturing and services, but remained among the highest seen over the past year. Sentiment has improved considerably since the lows seen late last year, attributed by survey respondents to fewer energy market concerns, lower recession risks, improved supply chains, and a peaking of inflation pressures. (…)

The New Sneaky Way Hackers Are Stealing Your Data at the Airport A seemingly convenient public charging port could lead to a data breach.

The New Sneaky Way Hackers Are Stealing Your Data at the Airport A seemingly convenient public charging port could lead to a data breach.

Public charging ports, which have proliferated in airport terminals in recent years, might feel beneficial if your device needs to juice up before your flight. But now, the FBI is warning travelers against using them all together due to cybersecurity concerns.

“Bad actors have figured out ways to use public USB ports to introduce malware and monitoring software onto devices,” states the FBI’s warning, which went out on Twitter in early April.

This cyber-theft tactic is commonly called “juice jacking,” according to privacy expert Amir Tarighat, CEO of cybersecurity firm Agency. It involves “concealing implanted malware within the physical charging cord or port, so when you connect your phone to a public charging station it’s exposed,” he says.

If an airport charging station is compromised and your device is infected, troves of personal information could be accessed. “Your passwords, your cards, your account number—if a hacker can get into your phone, they could get access to all of it,” Tarighat says.

Beyond simply stealing your data, malware presents a more complex scope of concerns, according to Tarighat, like installing spyware that can instruct the device to do something like download an app, pay for a product, screen record, or track what you type on your keyboard (a type of spyware called key-logging).

Of course, we all need to charge our devices while in transit. But it’s best to use your own USB cord plugged directly into an old fashioned wall outlet or even into a portable charger you brought from home. Public charging ports should be avoided outside the airport, too, whether they’re in hotels, event spaces, or on the street corner. Cyber-attacks could happen at any of them, regardless of their location. (…)

Aside from the public charging stations, there are other surreptitious ways hackers can access the personal information on your device from the airport terminal. “Definitely avoid public Wi-Fi hotspots,” says Tarighat. “Those networks don’t have the same protections as your at-home Wi-Fi. If the public network isn’t secure, hackers can hijack your session and log in as you, leaving your private documents, photos, and login credentials up for grabs.”