New global cases are not dropping. Of yesterday’s 85k new cases, 21k (25%) were from the USA, 12k (14%) from Brazil and 10k (12%) from Russia. (Bloomberg data and charts)

- The World Health Organization said the new coronavirus could become an endemic disease that “may never go away.â€

- Trump Says He Disagrees With Fauci’s Concerns Over Reopening “I was surprised by his answer, actually,†Trump told reporters Wednesday at the White House. “Because you know, it’s just — to me it’s not an acceptable answer, especially when it comes to schools.â€

- Coronavirus Spurs Spike in Serious Blood Disorder in Children While children remain at lower risk than older adults of developing severe complications after being infected with the Covid-19-causing SARS-CoV-2 virus, the research published Thursday in the Lancet medical journal shows that their risk isn’t zero.

- Abbott’s Coronavirus Test Falls Short of Rival Device Researchers said the company’s widely used device to swiftly detect coronavirus, including among senior White House officials, missed nearly half of the positive cases detected by another common test.

- Spanish herd immunity is still far off, study finds

PANDENOMICS

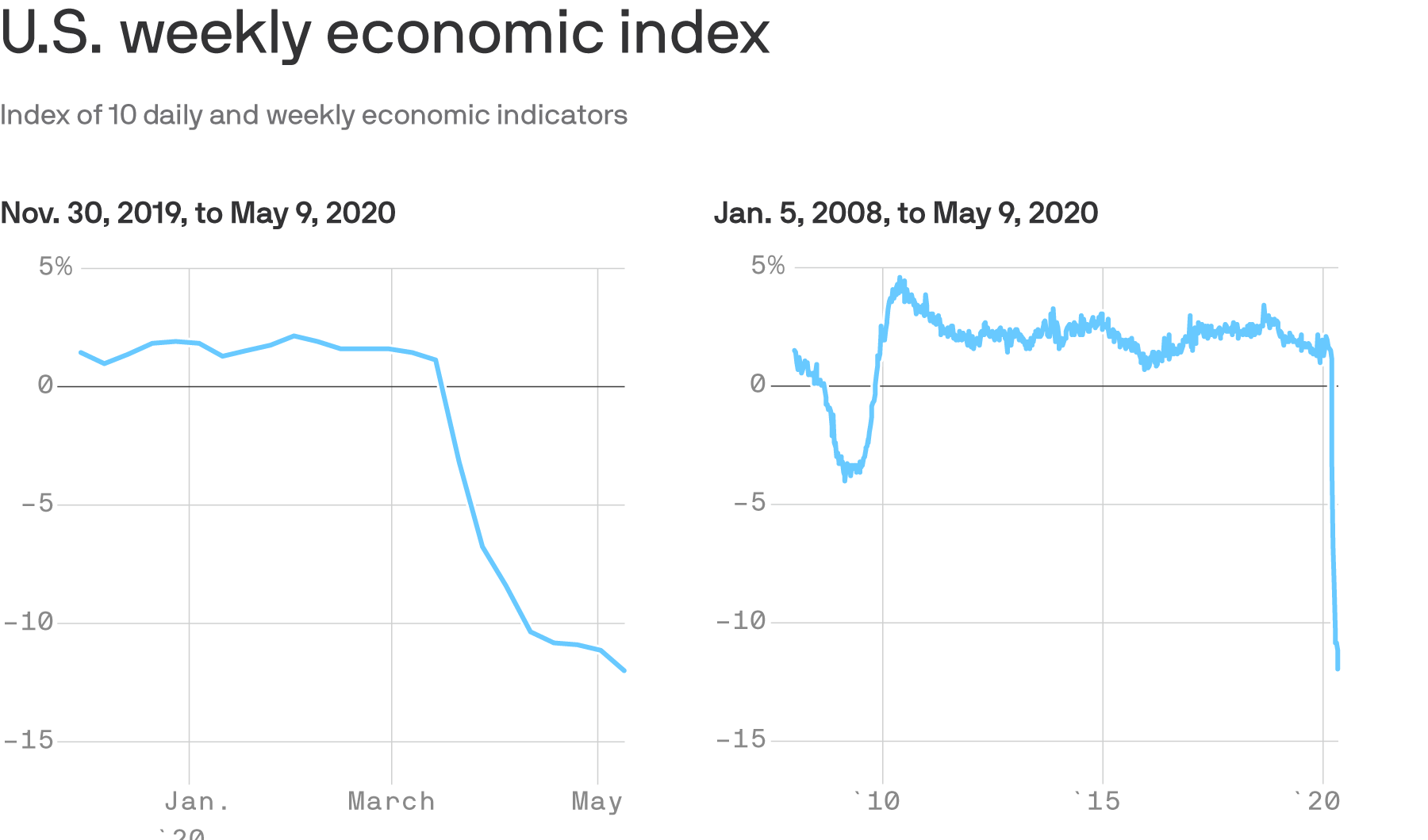

Fed Chairman Warns of Slow Rebound

(…) “There is a growing sense that the recovery may come more slowly than we would like…and that may mean that it’s necessary for us to do more,†Mr. Powell said Wednesday during an online speech and question-and-answer session.

He warned that, with revenues depressed for longer, waves of business bankruptcies could follow, risking a much slower pace of improvement in the job market. “Additional fiscal support could be costly but worth it if it helps avoid long-term economic damage and leaves us with a stronger recovery,†Mr. Powell said.

For example, if small businesses that were viable enterprises before the crisis fail, “we would lose more than just that business. We lose something more fundamental,†he said. “And it won’t be able to be replaced quickly.†(…)

He said the central bank wasn’t considering plans to cut its benchmark federal-funds rate below zero after it slashed the rate to near zero in March. (…) “The committee’s view on negative rates really has not changed,†said Mr. Powell. “This is not something that we’re looking at.†(…)

Mr. Powell said it was possible the jobless rate would peak and start to decline in the next few months but signaled concern that it could remain at an elevated level for a long time.

Early data revealed the downturn had hit households least able to bear it. Mr. Powell previewed a Fed survey to be released Thursday showing that among people who were working in February, nearly 40% of those households making less than $40,000 a year had lost a job in March. (…)

The Fed chairman warned of long-lasting damage that could follow. Deep and long recessions leave millions out of work for spells that could erode their skills and leave them in greater debt. Failures of thousands of small businesses would “destroy the life’s work and family legacy of many businesses and community leaders†and erase a main source of job creation when any recovery comes, he said. (…)

Think carefully, like there’s an election in less than 6 months:

Despite Powell’s message earlier in the day that “additional fiscal support could be costly, but worth it,†Mnuchin continues to contend that no immediate action is necessary. He rejected the House Democrats’ proposal to unleash another $3 trillion stimulus package as something Republicans wouldn’t agree to, and that there’s no urgency for additional spending. “Let’s have this money in the economy, let’s take the next 30 days and think carefully,†Mnuchin said. “If we need to spend more money down the road, we’ll come back and do that.â€

- Coronavirus to Cause 17% Unemployment in June A monthly Wall Street Journal survey found economists expect gross domestic product to shrink 6.6% this year, and the unemployment rate to hit 17% this June.

STIMULUS VS LIFE SAVERS

This Goldman’s chart clearly shows that all the dollars directed toward American consumers have almost exactly offset the dollars not earned because of the pandemic/lockdowns. This is not stimulus money that boosts demand and provides pricing power to merchants and thus might result in demand-pull inflation. The payments are economic life savers to prevent a permanent collapse in demand and a depression (my emphasis).

Congress has provided stimulus payments, expanded unemployment benefits, and aid to businesses, and we expect the next phase to include a further extension of unemployment benefits, another round of stimulus payments, and more aid to state and local governments. This fiscal easing has largely offset the hit to private income, resulting in only the modest net decline in disposable income from pre-virus levels in 2020 (…).

The big question is, as states reopen, will all that money finds its way where it would normally have been, a key assumption for the V-shape recovery? Can we realistically expect to be at 100% sometime after re-opening? No way, unless there is genuine mega stimulus on top of the band-aids.

Problem is, the virus is not going away just yet. So we will need more bridging until we truly get on the other side, hoping unemployment is restored to some “decent†level and the consumer does not save too much and consumes the economy out of this hole. If that is not wishful thinking… at least until the virus goes away…

- JPMorgan’s U.S. credit card holders spent 40% less due to coronavirus The overall fall in spending was 8 times larger than the average drop in household credit card spending in the first month of unemployment during regular times, according to the report.

(…) The JPMorgan Chase Institute studied anonymized spending data from more than 8 million Chase credit card customers for the period from March 1 to April 11.

Credit card users who report household incomes of less than $26,000 reduced spending by 38%, while wealthier cardholders, with incomes of more than $95,000, reduced spending by 46%. The group says the difference largely reflects higher average spending by wealthier households. (…)

- German luxury car maker BMW said that the recovery of demand in China provided some cause for hope, while Europe and the U.S. are still in decline. “In April, we already delivered nearly 14% more vehicles to customers than in April 2019. We know from our Chinese customers that consumption there will quickly bounce back, thanks to pent-up demand,†BMW Chief Executive Oliver Zipse told shareholders during a virtual annual general meeting on Thursday. BMW sales plunged 88% in China in February, as the country locked down to stop the spread of the coronavirus. But as the economy began opening in March, and auto makers opened their dealerships, customers have begun buying new cars again. “Demand for cars in countries like Spain, Italy and the UK will probably be very slow to recover,†he said. “The same applies to the U.S.â€

- In its monthly oil-market report, the IEA projected global demand to drop by 21.5 million barrels a day this month, while crude-producing nations and companies slash output by 12 million barrels a day.

- Lloyd’s, a marketplace of insurance syndicates, estimates underwriting losses covered by the global insurance industry will total around $107 billion this year, comparable to claims paid out for catastrophic hurricanes in 2005 and 2017. It also predicts a $96 billion loss in the industry’s investment portfolios, or money set aside to pay future claims. “This is something the likes of which we have never seen before,†Mr. Neal said, referring to the amount of underwriting losses coupled with the fall in investment value.

- Canadian malls collect just 15 per cent of May rent from tenants This follows April’s figure of around 25 per cent.

![]() As reported by STR, U.S. industry wide hotel RevPAR decreased 74.4% last week (week ended May 9) from year-ago levels. The prior week had seen an 76.8%.

As reported by STR, U.S. industry wide hotel RevPAR decreased 74.4% last week (week ended May 9) from year-ago levels. The prior week had seen an 76.8%.

Over the last 28 days, U.S. RevPAR is down 77.0%. Industrywide RevPAR for the U.S. was down 19.3% in 1Q20 (January and February RevPAR were up 2.2% and 1.7%, respectively). (Raymond James)

![]() This update comes from Black Box Intelligenceâ„¢ (formerly TDn2Kâ„¢) data from over 50,000 restaurant units and $75 billion in annual sales.

This update comes from Black Box Intelligenceâ„¢ (formerly TDn2Kâ„¢) data from over 50,000 restaurant units and $75 billion in annual sales.

- The number of restaurants reopening their dining rooms has steadily increased in recent days. As of Saturday, May 9, on average almost 30% of the restaurants operated by the companies that participated in our Restaurants Recovery Sales Flash survey opened their dining rooms in some capacity.

- Dine-in sales still represent a small percentage of the total. During the last week, dine-in sales have represented an average 11% of total limited-service sales and 13% of total sales in full-service restaurants. This remains a dramatic shift for full-service, which tended to see roughly 86% to 88% of their sales coming through dine-in in the last year.

- Comp sales for the industry were -45% during the week ending May 3, a 2.5 percentage point improvement since last week and the best result since week ending March 15.

[April was –55%] - Despite many companies beginning to bring back employees from furlough, of those people employed by chain restaurants back in January, only 45% of them remain actively employed today on average.

- Restaurant companies held on to most of their managers. Of those employed back in January, on average 75% of restaurant managers remain actively employed today.

U.S. rail traffic significantly worsened in April but trying to find a bottom

Week 18 carloads are originations through the week of 5/2/2020 Source: Association of American Railroads and Stifel research

CHINA WATCH

Vast Numbers of Unemployed Will Undermine China’s Recovery Millions of Chinese people are being thrown out of work by the collapse in global demand and a slow restart of the domestic economy. A lack of clarity about exactly how many is making it harder to gauge the chances for recovery.

(…) analysts from BNP Paribas SA said the real unemployment rate including non-urban residents could have reached 12% in the first quarter, and as many as 130 million people could have suffered some kind of job disruption. (…)

From Markit’s April PMI surveys:

- Manufacturing: “Reduced amounts of new work led firms to cut their staff

numbers again in April. Furthermore, the rate of job shedding

quickened from March.†- Services: “The sustained drop in total new work led to a further fall in

employment across the sector. Moreover, the rate of job

shedding was the quickest recorded since data collection

began in late-2005.â€

George Magnus in today’s FT:

(…) More suddenly than we could have expected, China now has a major unemployment problem. From an economic perspective, we may have arrived at what we could call ‘Peak China’. Put another way, it’s the moment when a major demand shock and balance sheet and other growth-sapping economic factors are colliding. (…)

Meanwhile, the structural headwinds China was facing anyway in the 2020s, arising from over-indebtedness, demographics, low productivity and weak institutions, have just become a whole lot bigger and more intractable. (…)

The Yuan, as stated, is likely to depreciate, perhaps considerably so in the next two to three years. China is still ageing faster than any other nation on Earth and the weaknesses and shortcomings in its social and healthcare insurance systems are being exposed by the current crisis, adding to the need for responses that will place additional downward pressures on growth. (…)

If, as some analysts think, China’s unemployment rate is now somewhere either side of 20 per cent and graduate employment prospects are the worst ever, there are truly reasons for worry. If SMEs, many of which take on a high proportion of graduates, are going to continue to suffer economically and be sidelined politically, the outlook for entrepreneurship and commerce is not propitious. (…)

At the end of my Red Flags book, I wrote that China faced daunting economic challenges but that we should never ignore what these might imply for the Communist Party’s politics and survival instincts and for its governance system at home and abroad. The pandemic can be seen as another significant red flag pointing to a brittleness in Xi Jinping’s China, which would make it more unpredictable and volatile.

Soaring Prices, Rotting Crops: Coronavirus Triggers Global Food Crisis

(…) Prices for staples such as rice and wheat have jumped in many cities, in part because of panic buying set off by export restrictions imposed by countries eager to ensure sufficient supplies at home. Trade disruptions and lockdowns are making it harder to move produce from farms to markets, processing plants and ports, leaving some food to rot in the fields.

At the same time, more people around the world are running short of money as economies contract and incomes shrivel or disappear. Currency devaluations in developing nations that depend on tourism or depreciating commodities like oil have compounded those problems, making imported food even less affordable.

“In the past, we have always dealt with either a demand-side crisis, or a supply-side crisis. But this is both—a supply and a demand crisis at the same time, and at a global level,†said Arif Husain, chief economist at the UN’s World Food Program. “This makes it unprecedented and uncharted.†(…)

The biggest danger going forward, economists say, is that the pandemic’s dislocations will affect not just existing food stocks but planting and harvesting in coming months. (…)

PANDEMONIUM

- China’s record Brazil soyabean imports impede US trade target Beijing faces ‘Herculean’ effort to meet phase one trade goals with Washington

- China steps up U.S. soybean buying with million-ton purchase Brazilian sales start to wane

- U.S. officials said in a bid to steal intellectual property related to coronavirus treatments and vaccines.

- Trump Says U.S. Is Looking at Chinese Companies on Exchanges President Donald Trump said he is “looking at†Chinese companies that trade on the NYSE and Nasdaq exchanges but do not follow U.S. accounting rules. “We are looking at that very strongly,†Trump told Fox Business host Maria Bartiromo in an interview that aired Thursday morning.

- China is “extremely dissatisfied” with lawsuits filed over the coronavirus pandemic by U.S. elected officials like Missouri attorney general Eric Schmitt, and is “mulling punitive countermeasures” state-run news reports. (Global Times)

Why vaccine ‘nationalism’ could slow coronavirus fight

- France warns against giving any country priority access to vaccine

- Sanofi CEO’s Remarks on Vaccine Plans Stir Outrage in France

Sanofi Chief Executive Officer Paul Hudson’s suggestion that the U.S. may get the French drugmaker’s coronavirus vaccine first sparked outrage in France, with one government minister calling the prospect “unacceptable.â€

“For us, it would be unacceptable that there be privileged access for this or that country on a pretext that would be a financial pretext,†Junior Economy Minister Agnes Pannier-Runacher said in an interview Thursday on Sud Radio.

The U.S. will likely be first in line should Sanofi succeed in developing a vaccine because the country was the first to fund the French company’s research, Hudson said this week in an interview with Bloomberg News. The U.S., which expanded a vaccine partnership with the company in February, expects “that if we’ve helped you manufacture the doses at risk, we expect to get the doses first,†Hudson said. (…)

More than 140 world leaders and experts signed an open letter released by UNAIDS and Oxfam on Thursday, calling for a “people’s vaccine†as well as treatments that would be available swiftly to all for free. (…)

Supplies of an experimental shot from the University of Oxford will be prioritized for the U.K. before other parts of the world, Pascal Soriot, CEO of AstraZeneca Plc, which will manufacture the vaccine, said last month. (…)

Asked on BFM Business TV if the U.S. would be first in line for a Sanofi vaccine, Olivier Bogillot, the head of Sanofi France, said, “No, I don’t confirm it. It’s evident that if Sanofi discovers a medicine, a vaccine against Covid-19, and if it’s effective, it will be available to all.â€

Sanofi has partnered with U.K. rival GlaxoSmithKline Plc on the project supported by the U.S. and says it could make 600 million doses annually. (…)

Wall Street Heavyweights Sound Alarm About Stock Prices

Legendary investors Stan Druckenmiller and David Tepper were the latest to weigh in after a historic market rebound, saying the risk-reward of holding shares is the worst they’ve encountered in years. Druckenmiller on Tuesday called a V-shaped recovery — the idea the economy will quickly snap back as the coronavirus pandemic eases — a “fantasy.†Tepper said Wednesday that next to 1999, equities are overvalued the most he’s ever seen. (…) Managers including Bill Miller, Paul Singer and Paul Tudor Jones have all voiced doubts about markets or the economy. (…)

Tepper, who runs the $13 billion Appaloosa hedge fund, told CNBC on Wednesday that valuations are “nuts†for some individual stocks on the Nasdaq. He also highlighted banks and airlines as difficult areas in which to invest right now. (…)

Trump attacked “so-called ‘rich guys’†in a tweet Wednesday. “You must always remember that some are betting big against it, and make a lot of money if it goes down,†Trump wrote about the stock market. “Then they go positive, get big publicity, and make it going up. They get you both ways.†(…)

RBC’s Calvasina Warns of ‘Significant’ Drawdown in U.S. Stocks

BMW faces dividend showdown as it pursues state subsidies German industry under fire for rewarding investors while seeking government support

TECHNICALS WATCH

- 13/34–Week EMA Trend (CMG Wealth)

U.S. Warships Support Malaysia Against China Pressure in South China Sea American officials accuse Beijing of coercing smaller countries out of developing offshore resources and say Navy presence shows U.S. commitment to region

")

") Source: ING Research, Google COVID-19 Community Mobility Reports, OECD

Source: ING Research, Google COVID-19 Community Mobility Reports, OECD") Source: ING Research, Google COVID-19 Community Mobility Reports

Source: ING Research, Google COVID-19 Community Mobility Reports

Source: PwC COVID-19 US CFO Pulse Survey

Source: PwC COVID-19 US CFO Pulse Survey

")

")

")

")