- Fauci, Other Health Officials Cite Risks of Early Opening In a Senate hearing, top Trump administration health officials said serious risks would continue into the fall as schools looked to reopen.

- New Studies Add to Evidence that Children May Transmit the Coronavirus Experts said the new data suggest that cases could soar in many U.S. communities if schools reopen soon.

- Hong Kong records new local infections, breaking a 23-day streak.

- Germany will reopen borders that slammed shut to stop the spread of the virus, a critical step in re-establishing the free flow of people as the pandemic threatens European integration. Chancellor Angela Merkel’s government aims to return to normal border operations by June 15, as long as the spread of the disease remains under control, Interior Minister Horst Seehofer said on Wednesday.

- Japan may remove the state of emergency in major metropolitan cities including Tokyo and Osaka as early as next week, ahead of a scheduled May 31 expiry, Nippon Television reported, citing unidentified government officials. While the emergency is likely to be lifted for 34 of the country’s 47 prefectures on Thursday after receiving opinions from a panel of experts, areas including Tokyo, Osaka and Hokkaido may have to wait until May 21 as new coronavirus infections are still being found, the report said.

- Confirmed cases rose by 10,028 over the past day to 242,271. The number of new infections topped 10,000 for 11th straight day, but the pace of increase slowed to 4.3%. Moscow reported 4,703 new cases, the lowest number since May 1. Total fatalities rose to 2,212 after 96 more people died.

- U.S. and Canada to Extend Border Controls Until June, Globe Says

Virus Survivors Could Suffer Severe Health Effects for Years

Some recovered patients report breathlessness, fatigue and body pain months after first becoming infected. Small-scale studies conducted in Hong Kong and Wuhan, China show that survivors grapple with poorer functioning in their lungs, heart and liver. And that may be the tip of the iceberg.

The coronavirus is now known to attack many parts of the body beyond the respiratory system, causing damage from the eyeballs to the toes, the gut to the kidneys. Patients’ immune systems can go into overdrive to fight off the infection, compounding the damage done. (…)

Hong Kong’s hospital authority has been monitoring a group of Covid-19 patients for up to two months since they were released. They found about half of the 20 survivors had lung function below the normal range, said Owen Tsang, the medical director of the infectious disease center at Princess Margaret Hospital.

The diffusing capacity of their lungs — how well oxygen and carbon dioxide transfers between the lungs and blood — remained below healthy levels, Tsang observed.

A study of blood samples from 25 recovered patients in Wuhan, the city where the virus first emerged, found that they had not fully recovered normal functioning regardless of the severity of their coronavirus symptoms, according to a paper published April 7. (…)

PANDENOMICS

Lockdowns lifted, what does this mean for the eurozone economy?

(…) The eurozone countries now closest to “normal†mobility levels are Germany at 84% of January levels, Latvia at 82% and Finland at 78%. Austria, Greece, Slovenia, Slovakia and the other Baltic countries have seen their activity levels return to more than 70% of their respective January levels. The Netherlands was among the countries with the highest mobility levels during lockdown, but has only recovered mildly in recent weeks to 70% of normal activity. Spain, France and Italy are still below 50%. (…)

")

Note: index of activity since 15 Feb for retail & recreation, groceries & pharmacies and workplaces using Google COVID-19 Community Mobility Reports with data through 2 May. 100=baseline of activity between 3 Jan and 9 Feb.

So far, GDP declines for 1Q are strongly correlated to the severity of lockdowns ") Source: ING Research, Google COVID-19 Community Mobility Reports, OECD

Source: ING Research, Google COVID-19 Community Mobility Reports, OECD

Note: vertical axis represents the average for the lockdown index of activity between 15 Feb and 31 Mar for retail & recreation, groceries & pharmacies and workplaces using Google COVID-19 Community Mobility Reports. 100=baseline of activity between 3 Jan and 9 Feb.

The impact for 2Q is already much more severe than for 1Q, indicating a larger decline in GDP

") Source: ING Research, Google COVID-19 Community Mobility Reports

Source: ING Research, Google COVID-19 Community Mobility Reports

Chart 3 shows that even though we only have data for roughly one third of the quarter and economic activity will not immediately return to normal, the impact is already about twice as strong in most countries for 2Q than in 1Q. In some advanced economies outside the eurozone it’s even worse than that, look at the US, UK and Australia, for example. That means that the decline in the second quarter will definitely be more severe as the return to normalcy will remain very gradual over the coming months, meaning that the impact will only increase as the weeks go by. Just to give an example, Germany would have to see its mobility surge to more than 10% above the pre-lockdown levels for May and June to see 2Q activity return to its 1Q level. That is out of the question for the moment. All of this means that the unprecedented crisis is currently showing another unprecedented face: the inflow of dreadful traditional macro data will continue, while more experimental and real-time data suggests that the worst is already behind.

Coronavirus Lockdowns Trigger Big Drop in Consumer Prices U.S. consumer prices in April posted their largest monthly decline since the last recession after energy prices collapsed and efforts to contain the new coronavirus disrupted demand for a wide array of goods and services.

The Labor Department said the consumer-price index fell by 0.8% last month, the second month in a row prices have eased since the pandemic reached the U.S. and the biggest drop since 2008. Business closures and stay-home orders aimed at containing the virus have created cheap oil, and falling prices for air travel, clothing, car insurance and other goods and services.

Excluding the volatile food and energy categories, so-called core prices decreased 0.4%, the largest monthly drop in records dating to 1957. (…) Overall prices were up 0.3% from a year earlier, the lowest since 2015, and core prices were 1.4% higher from a year ago, the lowest since 2011. (…)

The Labor Department’s index for gasoline prices tumbled 20.6% in April from the prior month. (…) The price index for food at home posted its largest monthly increase since February 1974. Americans stocked up at the pandemic’s outset. Since then, outbreaks have forced meat-processing plants to close and otherwise snarled supply chains. The April price index for meats, poultry, fish and eggs increased 4.3% from a month earlier. (…)

Indexes for apparel, auto insurance and airfares all posted their largest monthly declines on record. (…)

Price data is all over the map as the lockdowns and supply chains are adapting. The median CPI actually rose 0.1% MoM while the 16% trimmed-mean CPI was unchanged. Food prices rose 1.5% MoM and are up 3.5% YoY.

What is intriguing is that April’s Core CPI is down 0.4% but core Goods are down 0.7% (-0.9% YoY) and core Services are down 0.4% (+2.2% YoY). Maybe just decimals.

For April 2020, trend CPI inflation is estimated to be in the 1.2% to 1.8% range, which is lower than the currently estimated March 2020 range of 1.8% to 1.9%. The decline primarily reflects the impact of extremely weak labor data on the full data set measure. Note that the COVID-19 outbreak continues to impact data collection for the CPI release.

U.S. Small Businesses Optimism Drops to Seven-Year Low

The National Federation of Independent Business (NFIB) Small Business Optimism Index for April fell 5.5 points to 90.9, its lowest level since March 2013. This follows a record 8.1 point drop in March.

Nine out of ten components of the index fell, led by 30 percentage point drop in the share of firms expecting higher real sales to a record -42% (data goes back to 1973). This implies that a net 42% of firms anticipate sales to decline over the next three months. (…)

A net 29% of firms now expect the economy to improve in six months, up from 5% in March. This is the highest level since late 2018. Interestingly, after rising to a three-year high of 92, the small business uncertainty index fell to 75 with the NFIB noting “most owners were quite certain that the economy will weaken in the near-term”.

Deflationary pressures set in with a net -18% of firms raising average selling prices in April down from +6% in March. This is the lowest level in ten years. A record net 3% of small planned on reducing prices. Wage pressures declined with a net 16% of firms raising wages over the next three months — a seven-year low — down from 31% in March. The share of firms expecting to increase compensation decreased to 7% from 16%.

Here’s what another survey of small biz says (NBER):

To shed light on how COVID-19 is affecting small businesses – and on the likely impact of the

recent stimulus bill, we conducted a survey of more than 5,800 small businesses. Several main

themes emerge from the results. First, mass layoffs and closures have already occurred. In our

sample, 43 percent of businesses are temporarily closed, and businesses have – on average –

reduced their employee counts by 40 percent relative to January. Second, consistent with previous literature, we find that many small businesses are financially fragile. For example, the median

business has more than $10,000 in monthly expenses and less than one month of cash on hand.

Third, businesses have widely varying beliefs about the likely duration of COVID related

disruptions. Fourth, the majority of businesses planned to seek funding through the CARES act.

However, many anticipated problems with accessing the aid, such as bureaucratic hassles and

difficulties establishing eligibility.

- At least 3% of restaurant operators have gone out of business, according to the National Restaurant Association.

- Major companies like Neiman Marcus, Forever 21, Gold’s Gym and Modell’s Sporting Goods have announced bankruptcy plans, while 3,000 store closings have been confirmed this year by companies including GNC, Macy’s, GameStop and many others. (Axios)

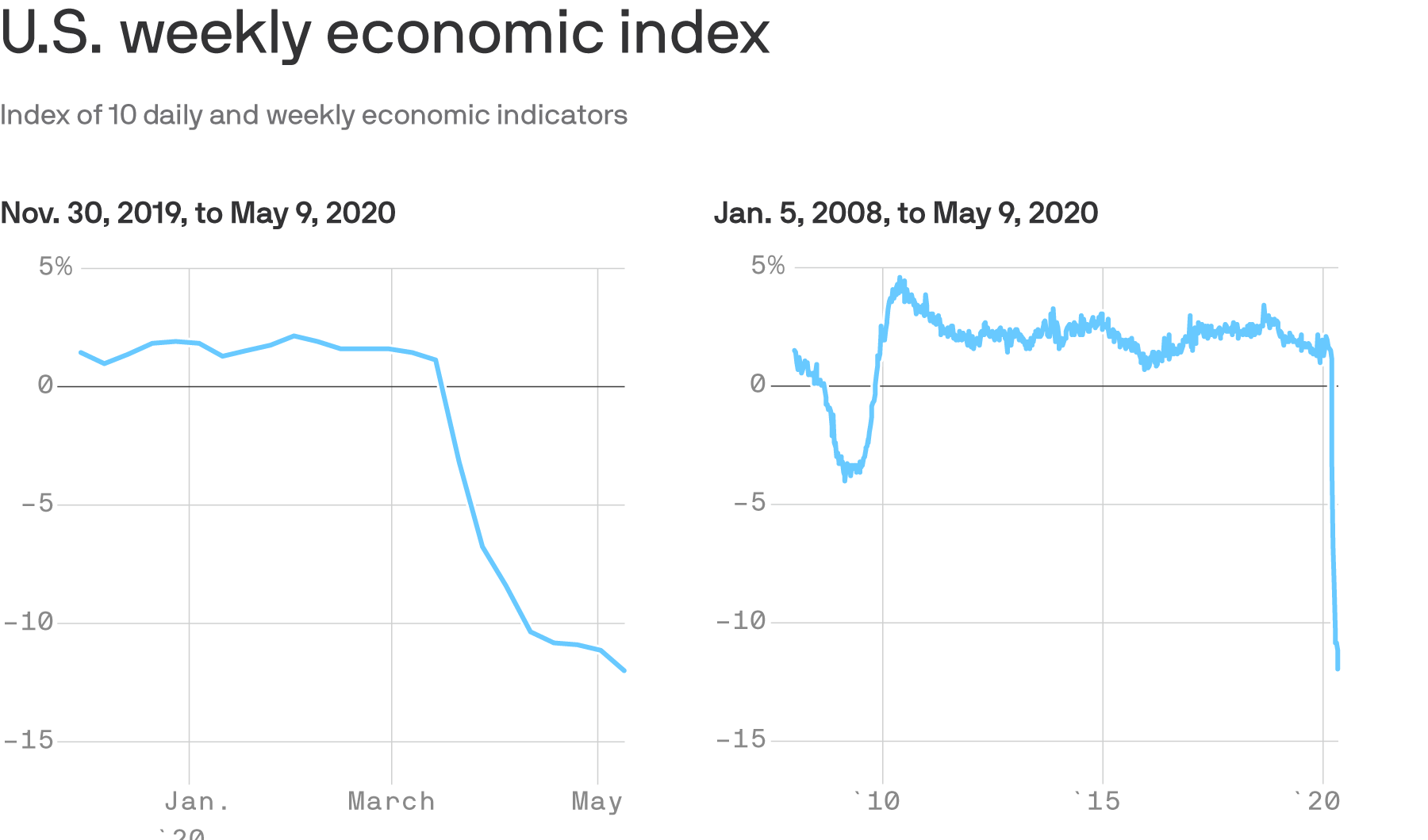

The New York Fed’s new weekly economic index fell to -12 for the week ended May 9, dropping from -11.14 the previous week. The index’s decline is now three times greater than the worst contraction seen during the Great Recession. (Axios)

Reproduced from Federal Reserve Bank of New York; Chart: Axios Visuals

PwC’s COVID-19 CFO Pulse Survey US findings — May 11, 2020

For the first time since the PwC Pulse survey began tracking CFO sentiment in mid-March, a majority of respondents expect that it will take their companies more than three months to recover once the pandemic recedes, of which 27% say it will take six or more months to bounce back (up from 23% two weeks ago).

Source: PwC COVID-19 US CFO Pulse Survey

Source: PwC COVID-19 US CFO Pulse Survey

April 8, 2020: base of 313; April 22, 2020: base of 305; May 6, 2020: base of 288

- Over half of respondents (55%) expect their company to suffer a decline of 10% or greater on revenue and/or profits for this year as a result of the pandemic. That is only slightly higher than the 53% who felt that way two weeks ago.

- A majority of respondents (80%) continue to report that their company is considering implementing additional cost measures — down from 86% two weeks ago — while 31% of CFOs expect layoffs to occur in the next month, compared with 32% who anticipated that in the previous survey.

- In PwC’s consumer sentiment survey, a scant 12% said they would immediately shop in stores once they reopened.

In the past few days:

- Economy Has Likely Bottomed, Poised for Rebound, Says Fed’s Barkin The Federal Reserve Bank of Richmond president believes the U.S. economy is probably at its lowest point in the coronavirus crisis.

- Fed’s Mester Expects Economy to Rebound Some in Second Half of 2020 Federal Reserve Bank of Cleveland leader Loretta Mester believes the economy can start recovering from the coronavirus crisis in the latter half of this year, while adding the economy will likely need additional support from the government.

- Fed’s Harker: Economy Recovery Likely to Be Uneven Philadelphia Fed President Patrick Harker said the U.S. economy’s eventual recovery from the Covid-19 pandemic is likely to be uneven, which could cause problems for the financial system.

This morning, the boss said:

-

Powell Says Washington Will Need to Spend More to Battle Downturn Federal Reserve Chairman Jerome Powell said Congress and the White House will need to spend more money to make sure policy makers’ quick initial response to the coronavirus-induced economic contraction isn’t wasted amid evidence that any recovery will take longer than first thought.

- House Democrats Release $3 Trillion Bill Bill allots $1 trillion for states and local governments, including funds for education, public safety; sum is roughly double Congress’s pandemic spending so far. The House is expected to return to Washington to vote on the bill Friday, but negotiations with Senate Republicans aren’t expected to start until later this month at the earliest.

- We continue to expect another $1.5tn in fiscal measures over the course of 2020-22, with about $550bn in 2020. Without an obvious forcing event this month, we do not expect Congress to enact the next round of fiscal measures until late June. (GS)

- The European Union’s statistics agency Wednesday said industrial output in the 19 countries that share the euro was 11.3% lower than in February, and 12.9% down on the same month last year. That was the largest month-to-month decline since records began in 1991, and much greater than the previous record drop, a 4.1% fall recorded in January 2009.

- Twitter says it will allow its employees to work from home permanently as it restructures its operations.

- The world’s largest container line is bracing for an historic slump in demand. A.P. Moller-Maersk A/S, which controls about one-fifth of the global fleet used to transport goods by sea, has warned that the fallout from Covid-19 will drive volumes down by as much as 25% this quarter.

- IEA Head Sees Oil Use Below Pre-Virus Levels for at Least a Year

- OECD warns extra debt taken on to fight pandemic ‘will haunt us’

Rosenberg: Five major points for investors right now

(…) we’re going to come out of this with a world that is going to be smaller; a world that is more nationalistic and much more protectionist than before – a trend that was already in motion from the trade conflicts that started about a year-and-a-half ago. There will be more regulation and government intervention, and global supply chains becoming more localized, especially in vital areas of national interest, such as medical supplies, food supplies and even semi-conductors. Globalization slows or stalls here, as does the cost-saving strategy of just-in-time inventories, because we have seen, in real time, the importance of having stockpiles on hand. The implications of all this means that for every unit of production, the global corporate cost curve goes up. And since we will still be operating with excess capacity for an extended period of time, this in turn means more compressed profit margins; and this, at a time when share buybacks will be slowed in favour of retention of cash on business balance sheets. (…)

This is why the recovery will be long and drawn out, because what comes next is that a secular change in attitudes toward credit and toward savings.

In the United States, households do not have enough cash on hand to tide them over through this crisis. The future will be one of treating “savings†as sacrosanct, especially for the 73 million U.S. boomers staring retirement in the face and with a much lower nest egg than they thought they had. This will prove to be a major secular shift that also ends up holding back the recovery in consumer spending, and again, that is why a V-shaped recovery is out of the question.

(…) this is what the future holds: rising savings rates constraining aggregate demand for years to come. The only way we don’t end up with more deflation is because localizing global supply chains, stagnant productivity and a higher government presence in the economy will impinge upon the aggregate supply curve. (…)

- Cash-strapped WeWork dumps about fifth of Hong Kong coworking space WeWork, the US operator of shared work spaces, has given up 182,000 sq ft in Causeway Bay and Tsim Sha Tsui, two of Hong Kong’s prime office districts, according to agents familiar with the matter.

- Hong Kong landlords slash Central rents by a third as vacancies hit six-year high Rents in the world’s most expensive office market return to 2017 levels as companies downsize or move somewhere cheaper to save costs amid economy reeling from Covid-19 pandemic

CHINA WATCH

Eyes on China for signs of what lies ahead

Refinitiv tells us that the NBS PMI surveys “suggest that the domestic picture is improving, albeit from very low levels†as both measures bounced slightly above 50, the threshold separating contraction from expansion.

But the official NBS data only means that just a few firms “have seen activity increase relative to an extremely weak March.†Remember, the data measures how many firms are seeing data better than in March vs worse. Nothing to do with how strong the data is.

Markit’s independent and relatively less weighted by large GSEs surveys show that the services sector is still struggling at 44.4 in April.

Goldman’s data:

Intel Capital invests in Chinese chip companies amid tech tensions Intel Capital, the venture arm of chipmaker Intel Corp , has invested in two Chinese startups in the semiconductor sector, the company announced on Wednesday, as part of its latest batch of deals.

(…) Intel Capital has consistently invested in Chinese startups along with small chip companies from around the world. In 2019 and 2018 it announced investments in two Chinese chip startups.

This batch of announced investments comes days after Intel CEO Bob Swan wrote a letter to the U.S. Department of Defense expressing readiness to build a chip fab in the United States, with the goal of ensuring U.S. technological leadership.

This is from Geopolitical Futures:

U.S. chipmaker Intel and Taiwan Semiconductor Manufacturing Co., which produces some 90 percent of the world’s most advanced microchips, are reportedly in talks with the Pentagon and the Commerce Department about building factories in the United States. TSMC is also reportedly in talks with Apple about building a plant in the U.S. Meanwhile, reports suggest U.S. officials are gauging interest from South Korea’s Samsung Electronics about expanding its own contract-manufacturing operations in the U.S.

This is potentially a big deal. Microchip production is one of those areas where the U.S. has at once an immense amount of leverage — through its dominance of semiconductor design and cutting-edge tooling systems — but also an immense amount of vulnerability through its dependence on foreign fabrication. With TSMC, for example, it wants the company to scale back its partnership with Chinese telecom giant Huawei, but it can’t afford to alienate TSMC or damage the company (by, for example, depriving it of U.S.-designed equipment or limiting its access to the U.S. market) to the point where it inadvertently accelerates the growth of upstart Chinese competitors. The U.S. is also concerned about critical fabrication operations concentrated a short missile flight away from mainland China. Taiwan, for its part, wants to find ways to quietly deepen integration with the U.S. and make itself indispensable to U.S. military needs, thereby ensuring that the U.S. would have its back if/when push comes to shove with the People’s Liberation Army.

EARNINGS WATCH

We now have 448 reports in and the Q1è20 blended earnings growth is –12.2% with a 67% beat rate and a +3.1% surprise factor. Seven of the 11 sectors surprised positively with Energy by the largest percentage (+123.8%).

The biggest surprise is that trailing EPS calculated by Refinitiv have risen in recent days, from $157.94 at the end of April to yesterday’s $158.99. This WSJ piece offers an explanation:

Companies Start Reaping Billions in Tax Breaks to Ride Out Economic Slump Oil refiners, restaurant operators count on cushion from tax deferrals and breaks in March coronavirus relief package

New tax breaks expected to total about $650 billion are starting to flow to U.S. businesses, giving them quick cash and longer-term help to ride out the coronavirus-induced economic downturn.

Companies reporting tax deferrals or benefits exceeding $100 million each include fast-casual chain Chipotle Mexican Grill Inc., CMG -0.44% Walt Disney Co., American Airlines Group Inc. AAL -4.46% and oil refiners Valero Energy Corp. VLO -3.45% and Marathon Petroleum Corp. MPC -1.50%

So far, more than 50 publicly traded companies have disclosed tax savings and deferrals totaling at least $2.8 billion, according to securities filings. Money is also going to private companies that don’t report earnings. (…)

The tax breaks, enacted in March, are a crucial piece of the government’s attempt to prop up businesses during the coronavirus pandemic, alongside Federal Reserve lending and the Small Business Administration’s loan-forgiveness program.

“They’re tinkering with the levers they have to get cash into the pockets of businesses, with the exception of just outright handing cash to them,†said David Hasen, who teaches tax law at the University of Florida. (…)

Generally applicable tax provisions are different. They aren’t limited by an application process, a dollar cap or specific agency approvals. Instead, they are available broadly to companies meeting the criteria in the law, and they are designed to generate cash quickly.

Oil-industry companies get money from the tax system while policy makers debate whether they should get lending support. Airlines can get tax refunds on top of grants from a separate Treasury Department program.

In all, businesses are likely to get about $650 billion in tax cuts, accelerated deductions and deferred payments in 2020 and 2021, according to the Joint Committee on Taxation. The net cost will shrink over time as deferred payments are made and companies use deductions now instead of in the future.

Many companies told investors that they are still analyzing the provisions; they may disclose more details later this year. Some may only realize tax-break benefits as they book 2020 losses that make them eligible. (…)

Companies can postpone some payroll taxes from this year until 2021 and 2022. They can cash out certain old credits instead of waiting. American Airlines, for example, said it would get $226 million from accelerating credits.

The breaks with the biggest impact now are retroactive changes designed to get cash to companies quickly. Companies with losses in 2018 and 2019 can carry those losses back up to five years. They can offset past profits and get tax refunds immediately.

Those changes to losses carry an extra bonus: Instead of using those losses to offset future profits taxed at 21%, companies can use them against past profits taxed at 35%.

Although the March bill was broadly bipartisan, some Democrats now say some of those changes on losses went too far, and the House bill introduced Tuesday would limit them. (…)

Companies’ numbers can’t necessarily be compared to each other, and some may not disclose changes that affect only cash flow or are too small to be deemed material. (…)

This will need further analysis and explanations.

In the meantime, the recent drop in equity prices combined with the slight uptick in trailing EPS and yesterday’s drop in inflation from 2.1% to 1.4% have triggered a

Change in the Rule of 20 Strategy

Change in the Rule of 20 Strategy

The Rule of 20 P/E has declined to 19.3 and the R20 Fair Value has increased to 2950 and reversed its 4-month declining trend.

As a result, the Rule of 20 Strategy reduces cash from 60% to 10%. We shall see if earnings data get revised or not to better reflect “operating†profits. But the rule is the rule…

")

- A Harris Poll survey of ordinary Americans released today found nearly a quarter (23%) have put more money into the stock market, compared to 19% who have taken money out and 45% who made no changes.

Druckenmiller Says Risk-Reward in Stocks Is Worst He’s Seen

(…) “The consensus out there seems to be: ‘Don’t worry, the Fed has your back,’†said Druckenmiller on Tuesday during a webcast held by The Economic Club of New York. “There’s only one problem with that: our analysis says it’s not true.†(…)

“It was basically a combination of transfer payments to individuals, basically paying them more not to work than to work,†he said. “And in addition to that, it was a bunch of payments to zombie companies to keep them alive.â€

Druckenmiller said he thinks that the current liquidity will soon shrink as U.S. Treasury borrowing crowds out the private economy and even overwhelms Fed purchases. (…)

“I pray I’m wrong on this, but I just think that the V-out is a fantasy,†the legendary hedge fund manager said, referring to a V-shaped recovery. (…)

ZeroHedge has more on that here.

EVOLUTION?

Thanks Pat. ![]()

")

")

")