Stanley Druckenmiller Admonishes Short Term Thinking, Warns On Debt (By Mark Melin)

Like Blackrock’s Larry Fink, Duquesne Capital’s Stanley Druckenmiller thinks society is borrowing from its future and “is in a short term bubble.” (…)

“Everyone is managing for the short term, and that is the problem with the Fed,” Druckenmiller said. While some are succeeding by ignoring short term, quarter-to-quarter fiscal results, it is the exception rather than the rule, as epitomized by U.S. central bankers. It was the Fed, Druckenmiller says, that “was late in recognizing the situation” that led up to the 2008 financial crisis, and then acted to right the ship. “What they did in 2009 was unbelievable creative, forceful and terrific.” While the best path forward is often best viewed from hindsight, the big question remains that “who knows what would have happened without (the Fed action)?” (…)

After six years of artificial market stimulation “you would have thought we would have gotten out of emergency measures,” he said. “At some point over six years when you have zero rates and quantitative easing, you cause investors to move out the risk curve” and emerging markets are allowed to act irresponsibly and engage in borrowing that “would never be allowed” in a history. (…)

Druckenmiller thinks an excessively accommodative stance by the central bank is “unnecessary” and “causing irrational behavior by governments, investors, corporations.” This behavior “is rampant in our whole society” and is “pulling demand forward today… borrowing from the future. There is a misallocation of resources. We are going to pay the piper at some point.”

When Druckenmiller mentions “the chickens will come home to roost,” he addressed the seldom publicly discussed issue of actual government debt obligations being obfuscated. He pegs real government debt liabilities at $205 trillion, a number that has been echoed by academics and economists. As first publically identified by Boston University’s Larry Kotlikoff and actively discussed in private meetings among quantitatively focused hedge fund managers, the government does not categorize as accounting liabilities money due retiring seniors for social security and medical benefits, as well as certain national defense obligations. Although it received scant press attention, Kotlikoff along with over 5,000 top academics and economists, called on the government to engage in accounting that properly accounts for its full liabilities.

“Sometime between now and 2030 this is going to be a problem, a big problem,” he said, quoting the outer edge of the range. The problem is in part demographic, as between now and 2050 the over 65, non-working population will grow at 117 percent while the working age population, from 18 to 64, grows at only 17 percent. While those taking retirement benefits from the system will grow dramatically, this spending growth comes off an already high level of entitlement spending on seniors.

Druckenmiller pointed out that the government currently spends $8,000 per child in the U.S. and over $44,000 on each senior. This spending gap is only going to grow on an aggregate basis as 11,000 new retirees are pulling benefits from a “lock-box” social security system that is bereft of assets.

Druckenmiller earlier said he was “worried about the eventual consequences and who is going to pay for it, which is not going to be me.” The answer, according to academics such as Kotlikoff, is to start addressing the situation by at least properly accounting for the situation, the first step. 9…)

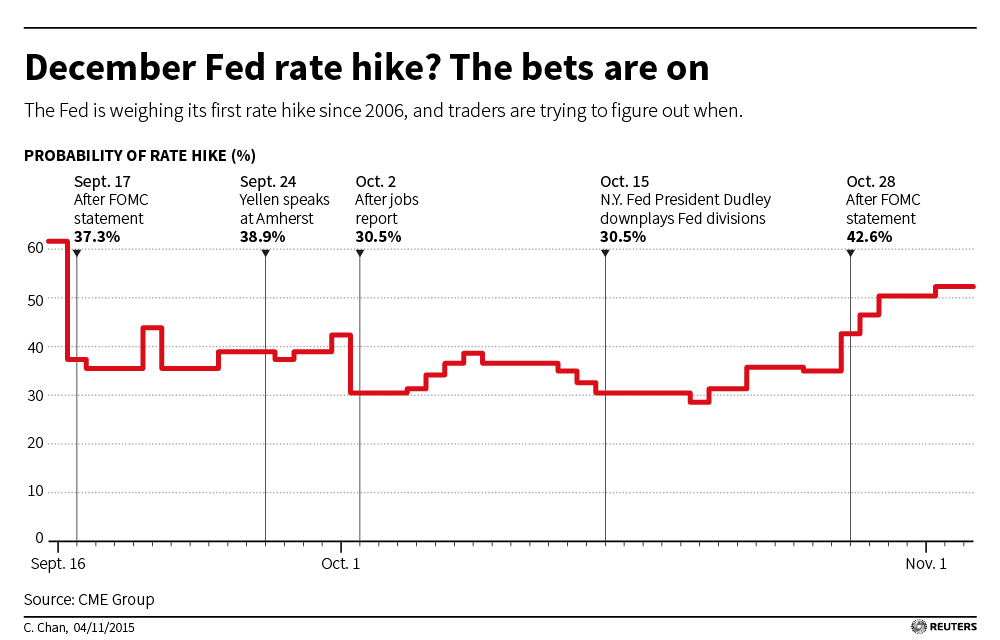

Druckenmiller said he is anticipating chaos, a market condition under which he has thrived and generated his biggest absolute returns. He is currently “working on assumption we may have started a primary bear market in July” and “can see myself getting very bearish, but can’t see myself getting very bullish.” He is currently shorting euro on assumption that central bank quantitative easing is going to remain strong in Europe as it is reduced or eliminated in the US amid “heavy breathing” regarding potentially raising rates. It is that “heavy breathing” that could turn into decisive action in December or might just turn out to be bad breath.

Yogi Berra: “When you come to a fork in the road, take it!”

From Gavekal’s Charles gave via John Mauldin:

(…) So, what is the fork now in front of us? To the right, we have what I would call the return to a normal cycle. The great disturbance of 2008-2009 has finally been absorbed. The US economy continues to grow, albeit more slowly than before. The US dollar has made its high, and long yields their lows, together with US inflation. If the world follows this road, it is now time to underweight America and move capital out of the US.

By contrast, to the left we have the risk of something unexpected: a massive rise in the value of the US dollar, similar to the one which followed the last great Keynesian experiment initiated in the 1970s by Federal Reserve chairman Arthur Burns. Most of the time, people analyze currencies on a flow basis, looking at differences in interest rates, current accounts, capital flows, purchasing parities, and so on. For 90% of the time this approach works. However, once in a while, a problem of stock arises.

By 1981 the short position on the US dollar—the dollars borrowed internationally—was greater than the US money supply. Technically the market had been cornered, and the dollar went ballistic. In 1985, in what amounted to the first great quantitative easing in history, the Fed extended massive swaps to the world’s major central banks to allow them to break out of the corner. Something similar happened in 2008.

My concern is that we could be in a similar situation again today (just see the latest BIS Quarterly Review). If we are, then the US dollar will go through the roof, US interest rates will fall by at least half, and US inflation will turn negative. I am not saying that the world economy definitely will take this left hand fork; I am saying that it could.

So, for investors, the solution is not to bet on one or other outcome, but to build a portfolio which will deliver acceptable performance whichever happens. This is difficult, because the two scenarios are clearly not compatible with each other. The only hedge against the second scenario, which would devastate countries and companies with US dollar debts and negative cash flows, is for investors to hold a sizable proportion of their assets in US zero coupon bonds, with a preference for constant durations of seven years or more, which would rally even as equity markets tanked. In parallel, investors should buy far out of the money US dollar calls to

protect their portfolios against a six sigma event, praying that these calls never move into the money.On the equity front, if we are moving into deflation, investors should own only the shares of companies selling goods and services elastic to prices. These are easily identified, because today they are the ones with rising sales. Investors should eliminate companies which have falling sales from their portfolios, as these companies are obviously selling goods and services which are inelastic to price. In the second scenario, they would get killed. During the latest earnings season fewer than half US companies reported rising sales, so equity portfolios investing only in companies selling goods and services elastic to prices will have massive tracking errors against the indexes. This is the price you will have to pay if you want to survive.

This 3-D Map Shows the Cities Where Most Economic Activity Happens in the USA

How Millennials Are Changing Wine

How Millennials Are Changing Wine

“SO MANY MILLENNIALS ARE interested more in the narrative of the wine rather than the wine,” said Jason Jacobeit, the 29-year-old head sommelier of Bâtard restaurant in New York. “A lot of mediocre wine is being sold on the basis of a story.”

Mr. Jacobeit lamented the fact that few of his generational peers took the time to understand why certain wines are greater than others. The rustic sparkling wine Pét-Nat (short for pétillant-naturel), for example, may be hip and fun, but it will never be as great as Champagne. Mr. Jacobeit said that his peers need to learn to distinguish the difference between “being excited about wine and wine that is genuinely exciting.”

Taylor Parsons, the 35-year-old wine director of République in Los Angeles attributes these “gaps” in millennials’ wine knowledge to their incessant search for the next cool thing, be it orange wine or Slovenian Chardonnay. “We get tons of requests for Slovenian Chardonnay,” he said.

Which might just mean you’ll soon be seeing many more Slovenian Chardonnays on restaurant wine lists. After all, millennials have been heralded as the generation capable of changing everything. The largest generation to date at 75 million strong, they certainly have clout. This group of 18- to 34-year-olds is technologically savvy, environmentally engaged and eager for stories about the things they love. They’ve helped transform the way we connect with one another, but will they also (re)shape the way we drink? I’d say “perhaps,” although a millennial might answer “Yaaaasssss!” (…)

So how and where are millennials getting their wine education? “Millennials don’t like ratings, but they like some kind of review,” said Adam Teeter, the 32-year-old editor and co-founder of VinePair, a New York-based online wine magazine for millennials. “They have a great thirst for knowledge.” (…)

Yet with conventional wisdom holding that millennials don’t care about luxury and aren’t loyal to brands, it’s little wonder that wine producers all over the world—like every other business—are scrambling to figure out what they want.

And it’s safe to say that whatever millennials do want, they’ll probably get it; by 2017, they’ll have more buying power than any other demographic group. So though boomers and Gen Xers helped build and sustain the wine business over the years, companies big and small are paying attention to millennial habits and marketing their products accordingly. (…)

E.&J. Gallo Winery’s Carnivor Cabernet is a perfect example. Launched in 2013 and priced at $15, the wine is aimed at young male drinkers. “Millennials are very driven by word-of-mouth, so we engage key influencers in conversation about our product,” Molly Davis,Gallo’s vice president of marketing, wrote in an email about the brand’s strategy. In other words, they send bottles to bloggers and hold tasting events. Carnivor Cabernet’s website is heavy on social media, promoting the hashtag #DevourLife and featuring a feed from its Instagram account. And the company has put together a guide to meat cuts, with recipes, in the hope of furthering its millennial appeal. (…)

The Cour-Cheverny was acceptable, but the back story I told them—an obscure white grape (Romorantin) that almost disappeared—was deemed uncompelling. “Maybe if the story was more interesting I would have liked the wine more,”

said Steven, a 32-year-old lawyer. In this regard, at least, my focus group supported the research I’d found. (…)

Will millennials in the end “revolutionize” wine—or banking or dining, for that matter? Will they render wine scores obsolete and classic wines like Bordeaux and Burgundy mere runners up to…Slovenian Chardonnay? Perhaps. They’ve certainly done their part to promote small producers creating interesting wines in odd corners of the globe. But to truly claim their position as the most powerful consumers in the world, they’ll need to develop a broader context and a deeper understanding of the entire world of wine—and not just an appreciation of a good story or a few obscure grapes.

{kind=link}