![]() Note: I am travelling in Asia until April 24. Limited equipment and different time zones will limit the frequency and depth of my postings.

Note: I am travelling in Asia until April 24. Limited equipment and different time zones will limit the frequency and depth of my postings.

Brisk Hiring Bolsters Fed’s Cautious Stance on Rate Cuts U.S. added 303,000 jobs in March, significantly more than the expected 200,000.

The unemployment rate slipped to 3.8%, versus February’s 3.9%, in line with expectations.

Average hourly earnings rose 4.1% from a year ago, the smallest gain since June 2021. (…)

Fed Chair Jerome Powell in recent months has signaled, however, that he no longer regards strong hiring as something to fear. That is because the labor force has been growing steadily, largely due to a strong rebound in immigration. As a result, brisk hiring isn’t stoking concern on Powell’s part that the economy is at significant risk of overheating.

“The economy actually isn’t becoming tighter, which it ordinarily would. It’s actually becoming a little looser, and you’re seeing inflation come down—very unusual situation,” Powell said on Wednesday. (…)

A few Fed officials have said there is no need to consider lowering rates pre-emptively. Given the “meaningful risks” that inflation runs at closer to 3% than the Fed’s 2% goal, it is “much too soon to think about cutting interest rates,” said Dallas Fed President Lorie Logan in remarks Friday.

Traders continue to walk back expectations for interest-rate cuts this year. Interest-rate futures now imply that one or two quarter-point cuts are more likely to the market than the three forecast by Fed officials in March. (…)

Private education and healthcare added 88,000 jobs last month, while leisure and hospitality added 49,000. Combined, the two have accounted for 1.5 million of the 2.9 million jobs the U.S. has gained in the past year. (…) Relative to the trend during the five years before the pandemic, there are some 2.7 million fewer jobs in those sectors than might have been expected. (…)

Source: U.S. Department of Labor and Wells Fargo Economics

Other facts:

-

Employment growth has gathered speed in each month of the year (+256K in January, +270K in February and +303K in March).

-

The three-month average pace of payroll gains (276K) is running at its strongest pace in a year.

-

The workforce participation rate rose to 62.7% from 62.5% the prior month, its highest level since November.

Wells Fargo pretty much echoes the current consensus on wages and inflation:

Average hourly earnings (AHE) picked up slightly in March (+0.3%) and over the quarter (4.4% annualized). However, on a year-over-year basis, wage growth slipped to nearly a three-year low of 4.1% in a sign inflationary pressures from the jobs market continue to gradually subside. With fewer workers quitting their jobs and businesses reporting that they are having an easier time filling positions, we expect wage growth to slow a bit further in the months ahead, although wage gains do not need to ease much further to allay concerns over inflation.

The Fed’s preferred measure of labor costs, the Employment Cost Index, currently suggests compensation cost growth has returned to a pace that is nearly consistent with the central bank’s 2% inflation goal after accounting for labor productivity growth.

Source: U.S. Department of Labor and Wells Fargo Economics

On the other hand, labor income keeps growing at more than 5% (+5.3% in Q1, +5.9% in March), sustaining overall consumer demand (never mind savings and the wealth effect) and potentially boosting retail sales (goods) growth back up.

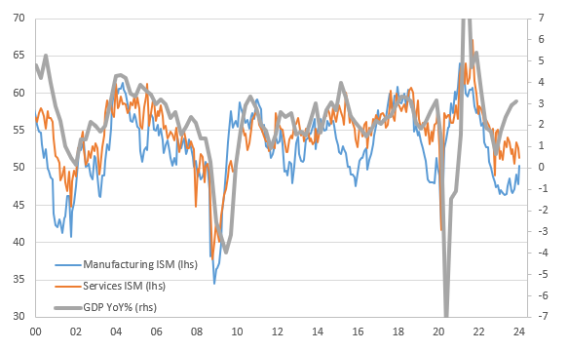

According the recent PMI surveys, the inflation battle is not over:

Some companies indicated that cost considerations had led them to hold off on hiring.

In fact, higher wages were a key factor behind the latest increase in input costs, according to respondents. Panellists also reported rises in transportation and material prices. As a result, input costs increased sharply during the month, with the rate of inflation accelerating to a six-month high. The latest rise was also sharper than the series average as 23% of companies recorded inflation over the month.

In turn, the pace of output price inflation also quickened markedly from that seen in February to the fastest since July 2023 as companies passed higher input costs through to their customers. As with input prices, the rise in charges was also faster than the average since the survey began in 2009.

Rates of both input cost and output price inflation quickened, and were at six- and ten-month highs respectively. Sharper price rises were seen in both monitored sectors.

The sustained upturn is being accompanied by renewed upward price pressures, however, with wage growth in particular driving costs higher. Rising raw material and fuel prices are also adding to cost burdens, which is in turn driving average selling prices for goods and services higher at a rate not seen since July of last year. Both manufacturers and services providers alike are seeing intensifying cost and selling price inflation rates, which is likely to feed through to higher consumer price inflation in the near term.

Worldwide PMI survey data compiled by S&P Global found average prices charged for goods and services to have risen globally at the fastest rate for ten months in March. The rate of inflation has now accelerated for two successive months, after having cooled to a 39-month low in January.

Although still running well below the highs seen during the pandemic, the upturn in the PMI selling prices index from 53.5 in February to 53.8 in March indicates that inflationary pressures remain elevated by historical standards.

By comparison, this index averaged just 51.2 in the decade preceding the pandemic; a time when global consumer price inflation averaged 2.7%. The current PMI readings are consistent with global inflation running close to 4%. Note also that the PMI data tend to lead changes in the annual rate of consumer price inflation by around six months, providing a valuable steer on the likely near-term path of inflation.

With this in mind, the suggestion from the PMI is that global inflation looks likely to remain sticky at an elevated level by historical standards as we head into mid-year.

The main area of stubborn price pressure remains the service sector, which reported the steepest price rise for eight months globally in March, the rate of increase running well ahead of the average seen prior to the pandemic.

Manufacturing prices rose for an eighth successive month in March, in a further sign that the disinflationary impact from falling goods prices has faded, but the rate of increase moderated slightly to a pace just below the pre-pandemic ten-year average.

Looking at the anecdotal evidence provided by PMI respondents globally, the main reason cited for charging higher prices was the need to pass on higher labour costs amid upward pressure on wages and salaries. These labour cost pressures hit an eight-month high, running at close to four-times the long-run average.

However, March also saw some renewed upward pressure on prices from both raw material costs and strengthening demand, the latter adding to firms’ pricing power. Energy, in contrast, remained a downward driver of prices on average globally.

The steepest rates of selling price inflation were recorded in the UK and the US in March, although directions of travel varied. While the rate of increase slowed in the UK, albeit remaining similar to that seen in the prior eight months, the rate accelerated sharply in the US to hit a ten-month high.

And now, oil prices are up 20% YtD.

We might have to increase the [20%] odds of a 1970s-like scenario [second peak in inflation] if the price of oil continues to rise. Our very good friend Steve Soukup posted an April 6 article titled “Saudi Arabia and the Tale of Two Presidents.” You should read it. The basic thesis is that the Saudis might like to see President Joe Biden lose to Donald Trump. So they might do whatever they can to boost the price of oil before the November election. Both the Saudis and Russians started reducing their output last summer. (…)

The price of oil has also been rising on mounting geopolitical risks (…). A direct confrontation between Israel and Iran would rapidly boost the price of a barrel of Brent crude oil over $100.

Meanwhile, the price of gold is soaring in new high territory (chart). Another wage-price spiral attributable to rising oil prices would be very reminiscent of the Great Inflation of the 1970s, when the price of gold soared. (…)

US Consumer Borrowing Rises, Driven by Credit-Card Balances

Total credit rose $14.1 billion after a revised $17.7 billion gain in January, according to Federal Reserve data released Friday. The median estimate in a Bloomberg survey of economists called for a $15 billion increase.

Revolving credit, which includes credit cards, climbed $11.3 billion in February. Non-revolving credit, such as loans for vehicle purchases and school tuition, increased $2.9 billion. (…)

Total credit expanded at a 3.4% annual rate in February after growing 4.2% the month prior.

Canada Unemployment Rate Jumps to 6.1% in March The number of employed working-aged people dipped by 2,200 from the month before

Employment nationally slipped by 2,200 in March from the month before, the first decline since a similar dip last July, while the unemployment rate was 0.3 percentage point higher at 6.1%, Statistics Canada reported Friday.

The jobless rate was well above the 5.9% expected by economists and at a full percentage point ahead of a year earlier is the highest since November 2017, outside a bump-up in unemployment at the start of 2022 when workplaces were again struck with a new strain of Covid-19.

When calculated using U.S. Labor Department methodology, Canada’s unemployment rate was 0.2 point higher at 5.2%. That contrasts sharply with stronger-than-expected 303,000 jobs growth in the U.S. in March and the slip in the unemployment rate to 3.8%. (…)

The labor force grew 57,700 last month but the employment rate, the proportion of the working-age population that is employed, was down for a sixth straight month to 61.4%, 0.9 percentage point lower than a year earlier. (…)

Average hourly wages for permanent employees rose 5.0% from a year earlier, matching the advance economists anticipated and up from 4.9% growth the prior month.

Statistics Canada’s survey showed the weakness in employment was entirely on the back of a pullback in self-employment, which offset modest rises in the numbers of both private and public sector workers. Canada’s public sector has been a big driver of recent hiring, and compared with a year earlier the segment has added some 202,000 jobs where the private sector has increased by 141,000. (…)

NBF:

The just-released March employment report revealed an unprecedented quarterly increase in Canada’s working-age population: a whopping 300,000 people in Q1 2024 (or 3.7% annualized). Economists, businesses, municipalities, and even our own central bank are struggling to calibrate business plans or policies against a demographic unknown.

As today’s Hot Chart shows, based on current population numbers, we estimate that Canada’s population is on track to reach just under 41.5 million people this year. As shown, this is well above even the most aggressive scenario published by Statistics Canada (most forecasters have historically based their projections on the intermediate scenario). Recall that in its January MPR, the Bank of Canada projected population growth of 2% in 2024.

The current path is at least 3%, or 50% faster than the BoC assumed. As Canada’s famed demographer David Foot once said, “demographics explain two-thirds of everything.” With that in mind, we can’t wait to see what the BoC will forecast next week, as there are currently no Statcan scenarios to guide us.

EARNINGS WATCH

The beat goes on!

The usual 20 early reporters are in: the beat rate is 90% with a surprise factor of +13.4% for actual earnings growth of 42.9% on revenues up 4.7%. This from 11 consumer-centric companies and 5 ITs.

Overall, 112 S&P 500 companies have issued quarterly EPS guidance for the first quarter. Of these companies, 79 have issued negative EPS guidance and 33 have issued positive EPS guidance. The number of companies issuing negative EPS guidance is above the 5-year average of 58 and above the 10-year average of 62. In fact, this quarter ties the mark with Q2 2019 and Q1 2016 for the second-highest number of S&P 500 companies issuing negative EPS guidance for a quarter since FactSet began tracking this metric in 2006. The record-high number is 82, which occurred in Q1 2023.

Seven sectors have seen more companies issue negative EPS guidance for Q1 2024 compared to their 5-year averages, led by the Industrials (14.0 vs. 7.7), Information Technology (25.0 vs. 20.4), Consumer Staples (7.0 vs. 2.7), and Health Care (12.0 vs. 8.4) sectors.

The percentage of companies issuing negative EPS guidance is 71% (79 out of 112), which is also above the 5-year average of 59% and above the 10-year average of 63%. This quarter marks the second-highest percentage of S&P 500 companies issuing negative EPS guidance since Q3 2019 (72%), trailing only Q1 2023 (75%).

At this point in time, 263 companies in the index have issued EPS guidance for the current fiscal year (FY 2024 or FY

2025). Of these 263 companies, 141 have issued negative EPS guidance and 122 have issued positive EPS guidance.

The percentage of companies issuing negative EPS guidance is 54% (141 out of 263).

Goldman Sachs:

Consensus expects 3% year/year EPS growth for the aggregate S&P 500 index, a deceleration from the 8% growth posted in 4Q earnings season. This quarter’s expected growth rate is the highest pre-season bar set by consensus since 2Q 2022. Notably, aggregate results have exceeded pre-season EPS growth estimates in each of the previous four quarters by an average of 4 pp.

S&P 500 margins are expected to sequentially trough in 1Q. Bottom-up consensus expects the S&P 500 will post 10.9% net margins in 1Q, a 28 bp sequential contraction but a 2 bp yr/yr expansion. Energy, Materials, and Health Care are each expected to post yr/yr margin contractions of greater than 100 bp. The 10 S&P 500 stocks with the largest market caps are expected to expand margins by nearly 400 bp year/year while the remaining 490 firms in the index will see margins fall by 57 bp.

The 10 largest S&P 500 companies are expected to grow sales by 15% year/year and post EPS growth of 32%. In contrast, the remaining 490 firms are expected to grow topline by just 2% year/year and deliver EPS growth of -4%.

Upward EPS revisions for the largest stocks have meant revisions for the index have been better than average. Since mid-2023, S&P 500 consensus 2024 EPS has been cut by just 1% compared with -6% at this point in the average year since 1985. Excluding the 10 largest stocks – which have had their EPS estimates raised by 18% – revisions are in line with the historical average (-6%, Exhibit 6).

Another record:

- Dwindling magnificence: From the Magnificent 7, to the Fab Four two weeks ago and now to the Magnificent 3:

The 13-34 week EMA trends now have 2 downs, 5 ups, some quite extended:

TSLA

APPL

GOOG

META

AMZN

NVDA

MSFT

-

Who Owns Stocks: We should probably expect the red part to go up as life expectancy goes up (went from about 75yrs to almost 80yrs over that period — that’s about 5 more years of compounding!). The younger crowd made a bit of a comeback as the pandemic stimulus made stocks cool again. But the 40-54 years cohort has been squeezed the most — perhaps due to rising house prices meaning mortgage payments take priority over saving and investing (maybe also people having kids later in life). (Callum Thomas)

Source: @KobeissiLetter

FYI

![]() Americans bought a record 1.2 million EVs in 2023, according to Cox Automotive’s Kelley Blue Book. That’s 7.6% of the total U.S. new-vehicle market, up from 5.9% in 2022.

Americans bought a record 1.2 million EVs in 2023, according to Cox Automotive’s Kelley Blue Book. That’s 7.6% of the total U.S. new-vehicle market, up from 5.9% in 2022.

- But EVs’ share fell back to 7.1% in the first three months of 2024.

- Cox is sticking with its forecast for 10% EV share by the end of 2024. Throw in hybrids and plug-in hybrids, and Cox says “electrified” vehicles could comprise almost 24% of new car sales by then. (Cox Automotive is part of Cox Enterprises, which also owns Axios.)