Powell’s Inflation Outlook at Odds With Markets The Federal Reserve brushed aside recent good news on prices, revising its interest-rate path up and economic growth down.

After raising interest rates by the expected half-percentage point on Wednesday, Fed Chairman Jerome Powell and his colleagues laid out an economic and interest-rate forecast premised on a painful, drawn-out battle with inflation completely at odds with the markets. (…)

In projections released this week, the central bank expects to raise rates ultimately to 5.1% by the end of 2023, a half-point higher than projected in September, and lower them only to 4.1% by late 2024. (…)

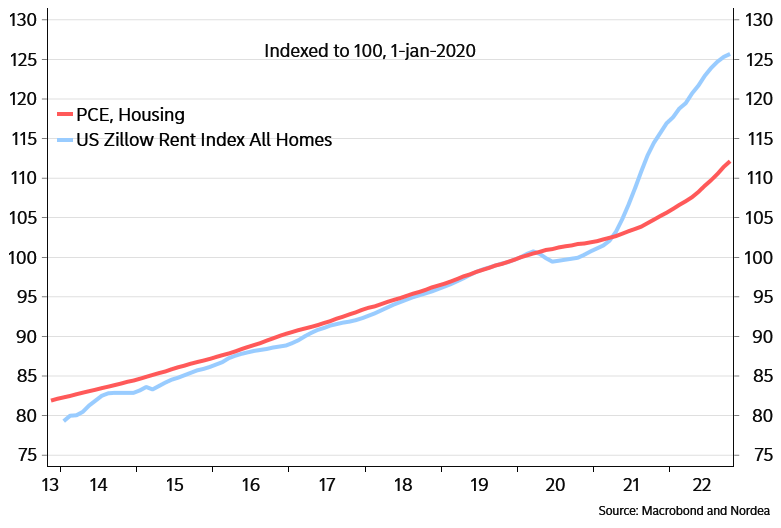

The Fed sees economic growth of just 0.5% next year, down sharply from September’s 1.2% projection and consistent with a recession. It sees unemployment climbing to 4.6% from 3.7% now, higher than projected in September. Such a combination would normally entail lower inflation. Yet the Fed actually raised its inflation forecast for the end of next year, to 3.1%. Excluding food and energy, it increased its “core” inflation forecast to 3.5% from 3.1%. (..)

According to Barclays, bond and derivative markets are now projecting core inflation, using the consumer-price index, of 2.6% at the end of 2023. That equates to 2% to 2.3% using the price index of personal-consumption expenditures preferred by the Fed. In other words, investors think inflation will have returned to the Fed’s 2% target in a year’s time. The stock market rally suggests they don’t think it will take a recession to achieve this. In other words, investors seem to have concluded that inflation was transitory all along and a soft landing—a slowing in growth but no recession—isn’t just possible, but likely.

(…) whatever good news the Fed might have taken from the October and November inflation reports seems to have been more than offset by the November employment report, which showed job growth remaining robust, unemployment near a half-century low, wage growth accelerating and the supply of labor shrinking. “The labor market continues to be out of balance, with demand substantially exceeding the supply of available workers,” Mr. Powell said Wednesday.

The other reason for the dichotomy could simply be that Mr. Powell has a longer memory than investors. He, like most economists and market participants, thought the rise in inflation in 2021 would be short-lived, and stuck with that view for too long. A year ago, the Fed thought core inflation would be 2.7% in the current quarter; it’s coming in at 4.8%. Those errors have been costly: Two years of too-high inflation make it more likely expectations and behavior would change in a way that makes that high inflation entrenched and even more painful to wring out.

Better, then, to assume a path for interest rates and the economy that is more pessimistic than the markets think. “The worst pain would come from a failure to raise rates high enough and allowing inflation to become entrenched,” Mr. Powell said.

- Jerome Powell’s Finest Hawk Feathers The Fed Chairman really, really wants you to believe him on inflation.

This WSJ editorial sums up nicely Powell’s presser:

The Fed Chairman donned his finest hawk feathers and said again and again at his press conference that the central bank hasn’t made enough progress getting prices under control and isn’t going to ease up until it does.

“We have more work to do.”

“Where we’re missing is on the inflation side. And we’re missing by a lot.”

“It will take substantially more evidence” for the Fed to conclude that inflation is falling enough to stop raising rates.

“We’ve made less progress than expected on inflation.” (…)

Mr. Powell really, really, really wants markets to believe there’s not an impostor behind that Paul Volcker mask.

(…) Mr. Powell and the Fed are still rebuilding their credibility after the 2021 fiasco of claiming inflation would be “transitory.” The Fed stuck to that line for months even as prices rose, and the result has been the worst inflation in 40 years. Markets still may not be sure that Mr. Powell and the Fed won’t wilt under political pressure when the jobless rate begins to increase or there’s a financial scare bigger than the crypto meltdown. (…)

Last December the median forecast by Fed officials for the fed funds rate in 2022 was 0.75%-1%. In March it was 1.75%-2%, then 3.25%-3.5% in June, 4.25%-4.5% in September, and now it’s 5%-5.25% for 2023. The trend underscores how badly the Fed misjudged inflation and the medicine required to break it. (…)

Mr. Powell said no officials had projected rate cuts next year and that they weren’t likely to consider lowering interest rates until policy makers are confident inflation is moving down to the Fed’s 2% goal in a sustained fashion.

Bloomberg Economics:

The most striking part of the updated SEP is how unified the committee is on the need to raise rates more aggressively – significantly higher than the 4.8% terminal rate markets had priced in ahead of the meeting. It’s also clear that officials recognize the amount of expected tightening will push the economy into recession.

But

“The market is not buying the Fed’s increasingly hawkish position that they are going to raise rates to a higher-than-expected level and keep them there,” said Lindsey Piegza, chief economist at Stifel Nicolaus & Co. “The market clearly thinks inflation is going to be on a much more desirable path than the Fed is anticipating.”

Source: Federal Reserve, ING

- John Authers: “The Fed has told us very clearly that it’s more hawkish than we thought, and it’s inherently very dangerous to ignore it. Investors aren’t supposed to fight the Fed. It’s one of the most constant aphorisms driven into the mind of any investor that they should never do it.”

Lastly, and importantly, Powell answered a question on changing the Fed’s 2% inflation target: “We’re not going to consider that under any circumstances.”

But Powell added: “it may be a longer-run project at some point.”

Another debate has been officially launched!

Business Inflation Expectations Decrease Significantly to 3.1 Percent

- How do your current sales levels compare with sales levels during what you consider to be “normal” times?

")

- By roughly what percent are your firm’s unit sales levels above/below “normal,” if at all?

")

- How do your current profit margins compare with “normal” times?

")

- Looking back, how do your unit costs compare with this time last year?

")

Goldman Says Commodities Will Gain 43% in 2023 as Supply Shortages Bite

Bank of England raises interest rates by half a percentage point Rates at the highest level in 14 years

China’s Economy Struggled in Zero Covid’s Final Month Retail sales tumbled as locked-down consumers cut back on spending, while industrial production lost momentum as factories grappled with Covid restrictions and slowing overseas demand.

(…) Data Thursday showed retail sales in China tumbled 5.9% in November from a year earlier as locked-down consumers cut back on spending, while industrial production lost momentum as factories grappled with tight Covid restrictions and slowing overseas demand for their products. Unemployment in big cities rose to 5.7% from 5.5% in October, while investment in buildings, machinery and other fixed assets slowed. (…)

“The customers haven’t come back. There are barely any now,” said a saleswoman at a woman’s footwear store in a Beijing shopping mall, who gave her surname as Xin. “Who can imagine after reopening, there would be even fewer customers?” (…)

@C_Barraud

Matthews Asia’s generally upbeat Andy Rothman’s recent note strikes an optimistic tone on China:

I remind investors that following the end of zero-COVID, China is likely to remain the only major economy engaged in serious easing of fiscal and monetary policy, while much of the world is tightening.

Chinese households have been in savings mode since the start of the pandemic with family bank balances up 42% from the beginning of 2020. The net increase in household bank accounts during this period is equal to US$ 4.8 trillion, which is larger than the GDP of the UK.

Those funds should fuel a consumer rebound in China and a recovery in mainland equities, where domestic investors hold about 95% of the market.

Déjà vu in the USA with the difference that the wealth effect remains quite negative for Chinese who have most of their savings in real estate:

China’s Home Price Slump Persists as Buyer Demand Remains Weak

New-home prices in 70 cities, excluding state-subsidized housing, slid 0.25% last month from October, when they fell 0.37%, National Bureau of Statistics figures showed Thursday. Sales dropped 31% from a year earlier, worsening from a 23% decrease in October, according to Bloomberg calculations based on official data. (…)

The slump in home values also persisted in the closely watched secondary market. Existing-home prices dropped 0.44%, easing slightly from 0.47% a month earlier, the figures showed. (…)

In 30 major cities tracked by CRIC, only 26% of projects offered were successfully sold. (…)

- China’s Leaders Plot Pivot Back Toward Boosting Economy Senior officials are setting a robust GDP growth target of more than 5% for next year as they loosen Covid rules and de-emphasize ideology

U.S. to remove some Chinese entities from red flag list soon, U.S. official says

The Biden administration plans to remove some Chinese entities from a red flag trade list, a U.S. official told Reuters on Wednesday amid closer cooperation with Beijing.

The plan to remove them soon from the so-called “unverified” list is thanks to greater willingness from the Chinese government to permit U.S. site visits, the person said.