Jobs Growth, Wage Gains Remained Strong in November The U.S. labor market remains historically tight, with many employers competing for a limited pool of workers and bidding up wages. The jobs data keep the Fed on track to raise rates by a half percentage point this month.

Employers added 263,000 jobs in November, holding near the strong gains of the previous three months, when they averaged 282,000 a month, the Labor Department said Friday. Job growth has slowed from the first half of the year and continues to well exceed its 2019 prepandemic pace, though some large corporations have recently announced layoffs.

The jobless rate remained at 3.7% last month, a historically low level that is pushing up wages. Average hourly earnings grew 5.1% in November from a year earlier, holding above the prepandemic pace of roughly 3%. (…)

Revised wage data released Friday could concern Fed officials because it points to an acceleration in pay gains in recent months. Average hourly earnings grew swiftly in November from a month earlier across industries including retail, transportation-and-warehousing and information services. (…)

The payrolls figures, which are subject to revisions, might overstate the strength of the job market, some economists said. A more comprehensive data set known as the quarterly census of employment and wages shows jobs have grown by 500,000 less in the year through June than payrolls indicate, according to UBS. Because monthly payrolls are eventually adjusted using those more comprehensive figures—which are based on employer tax records—they will likely be revised down. (…)

Other important facts from the employment report:

- The 25-54 age cohort saw its participation rate fall for a 3rd month to 82.4%. It was 83.1% in January 2020. The WSJ asks Where Did Young Male Workers Go?, noting that “the labor force participation among males ages 25 to 54 has slid to 88.4% from 89.3% before the pandemic. Don’t blame long Covid. The decline is most pronounced among young men. Labor participation among males ages 20 to 24 has fallen 1.7 percentage-points since January 2020 versus 0.5 for those ages 45 to 54.”

- The last 3-month job hiring averaged 272k vs the 6-month average of 323k, the 12-month average of 408k and the 2021 average of 562k. Still strong, but less and less so.

- The household survey revealed a 2nd straight drop of 138k after a 328k job loss in October. Actually, the household survey (red) is flat since March 2022 while payroll employment is up 1.8%, or 2.7 million new jobs (+336k per month). How and when will they rejoin?

- Average hourly earnings increased by 0.55% MoM (+6.7% a.r.) in November, +0.68% (+8.3% a.r.) for production and non-supervisory employees. Wages have sharply accelerated from their Q3 levels. Recent monthly increases now substantially exceed their YoY pace of 5.1% and 5.8% respectively.

- Average weekly hours declined by 0.1 to 34.4 hours, the first decline since June. Employers generally cut hours before letting people go. Weekly hours in manufacturing have declined almost non-stop since 2018 while wage growth (red) accelerated. Overtime hours in manufacturing have also been steadily declining and are now at their lowest level outside of recessions since 1990.

- Aggregate weekly payrolls (employment x hours x wages) rose 0.45% MoM in November after +0.63% in October. Q4 is thus averaging +6.5% annualized following +7.4% in Q3 and Q2, 8.4% in Q1 and 12.1% in Q4’21. The stacked bar chart shows that the growth in weekly payrolls came entirely from higher and accelerating wage rates (black) with actual employment (jobs and hours) no longer contributing. Stagflation?

Amazon has started rescinding job offers it had extended to new hires in its retail organization, a sign that the ecommerce giant’s cutbacks have moved beyond its devices division where recent layoffs were concentrated.

Representatives from the retail organization, which is led by Amazon’s CEO of Worldwide Amazon Stores Doug Herrington, this week began calling people who were due to start in January to tell them their jobs were being rescinded, according to two people who had offers rescinded.

So far, this analysis of the employment report was focused on consumer spending power and the economic cycle.

Perhaps more important is the analysis centered on inflation, particularly services inflation, given the sharp acceleration in wages.

As discussed previously, service-providers have two principal cost components: labor and energy. Core services inflation (blue line below) is intimately correlated with wages. The Employment Cost Index – Wages and Salaries (red) has been accelerating since Q1’21 reaching +5.7% in Q2’22 but slowed to 5.3% in Q3.

Hourly earnings growth (black) dipped to 4.9% in October but was 5.1% in November boosted by the sharp month to month acceleration from 0.3% in August to 0.5% in October and 0.55% in November, a 6.1% annualized rate in the last 2 months.

On that basis, services inflation should slow down from October’s +6.5% but rising wages are signalling that the 5% level might be difficult to breach. Fed headache!

Much hope is now placed on rental costs, up 7.0-7.5% YoY in October (40% of core CPI and 55% of CPI-core services). Even Jay Powell regularly educates us on the intricacies of rental inflation in the CPI.

Some key facts:

- CPI-core services is 92% correlated with CPI-Shelter. No surprise given its 55% weight.

- But CPI-Shelter carries a 71% correlation with wages. Renters can only afford what their wages allow. People trade up or down based on their needs but also, mainly, on monthly affordability.

- People need shelter. They either buy or rent. House prices (red) are up 40% since 2019. Rents: 12%.

- There is clearly a housing crisis in the USA. The availability of shelter is at a 40-year low, by a wide margin. Meanwhile, the number of households is up 3.8% since 2019.

- Rental vacancy is at its lowest since the early 1980s. Then, it took a 50% rise in the vacancy rate to gradually bring rent inflation back below 4%.

-

The apparent coming “tsunami” of new apartment buildings (blue below) will provide some relief but rental costs are much more correlated with wages which have yet to show signs of a meaningful slowdown. Note how the increases in new apartment buildings did not prevent rent inflation (red) from accelerating in the late 1990s, the mid-2000s and between 2010 and 2016. Wage trends (black) had a much more significant and direct impact.

In all, when it comes to inflation, we should really focus on wages. The recent trends are not great…The Fed has its work clearly cut out and there are no two ways about it.

- Delta, Pilots Reach Four-Year Deal With 31% in Pay Raises Delta Air Lines Inc. pilots would receive at least 31% in pay hikes over the four-year term of an agreement in principle reached with the carrier.

(…) It provides for an 18% pay increase effective when the final contract is signed, followed by a 5% hike after one year and then 4% after each of the next two years. The agreement also includes a provision to ensure Delta pay exceeds that in any contract for American or United pilots by at least 1% for its term.

(…)

The agreement also provides for a one-time payment after ratification equal to 4% of a pilot’s eligible earnings for 2020, 4% for 2021 and 14% for 2022.

Leaders of American’s union last month rejected a proposed contract that would have raised pay 19% over two years and United pilots overwhelmingly voted down a new labor agreement, saying it fell short of the “industry-leading contract” they deserved. (…)

- Summers Says Fed Will Need to Boost Rates More Than Markets Expect “Six is certainly a scenario we can write,” Summers said with regard to the peak percentage rate for the Fed’s benchmark. “And that tells me that five is not a good best-guess.”

The WSJ Nick Timiraos today, right when the FOMC enters its two-week blackout period:

Fed Could Pencil in Higher Interest Rates Next Year Brisk wage growth could lead officials to consider raising their policy rate above 5% in 2023 to fight inflation even as they prepare to downshift the size of rate increases at their December meeting.

(…) Policy makers expect price pressures to ease meaningfully next year, but brisk wage growth or higher inflation in labor-intensive service sectors of the economy could lead more of them to support raising their benchmark rate next year above the 5% currently anticipated by investors.

They want to guard against raising rates too little and allowing inflation to resurge, or raising them too much and causing unnecessary economic weakness, according to recent public comments and interviews. (…)

Officials could signal a slightly more aggressive rate outlook in their new quarterly economic projections to be released after the coming meeting. Those could show that policy makers expect to keep raising rates in at least quarter-point increments until they see clear signs that the labor market has cooled.

Most officials in September penciled in rates rising to between 4.5% and 5% next year. That landing zone could rise to between 4.75% and 5.25% in the new projections. (…)

Officials are likely to debate next week how much to raise rates in February, with views shaped by how they see underlying price pressures. If inflation slows but the labor market stays tight, they could be more divided over how to proceed.

Some officials could seek to push through another half-point rate rise in February because they see a greater risk that inflation won’t decline enough next year. Without signs of slower hiring, they could worry that inflation could pick up again.

Others see inflation as being driven primarily by supply bottlenecks and an overheated housing market. They think that as activity cools and supply-chain woes ease, inflation will rapidly decline and be closer to 2% in the coming year, and they would prefer a quarter-point rate increase in February. (…)

The labor market remains a source of concern because officials are worried that rising prices could be sustained by continued income growth and strong demand for workers. They are uneasy because even if corporate hiring executives and workers expect high inflation to subside over the next few years, employees could demand and receive bigger raises that keep paychecks and prices rising in lockstep. (…)

Mr. Powell said last week that wage growth had been running around 1.5 to 2 percentage points too high. “We want wages to go up strongly, but they have got to go up at a level that is consistent with 2% inflation over time,” he said.

He made his comments two days before the Labor Department reported that hourly earnings growth increased in November at its strongest pace since January. (…)

If 3.5% wage growth “is consistent with 2% inflation over time” (assuming 1.5% productivity gain), Mr. Powell’s math says wage growth is now running 3.0 to 3.5 percentage points too high.

BTW, NYC’s new open-pay laws will push wages up. How long before it spreads out?

- Is Your Colleague Earning More Than $200,000 a Year? Now You Can Find Out As a salary transparency law takes effect in New York City, postings show pay ranges for jobs at companies from Amazon to PwC

CEO optimism down, not out

The latest Business Roundtable (BRT) survey of its members — the chief executives of some of the world’s largest companies — still shows healthy expectations for sales, hiring plans and investment. But the results, shared first with Axios, do point to a gloomier outlook than just a few months ago — and a marked deterioration from last year. (…)

Surveyed executives were dialing back near-term revenue expectations, as well as hiring and investment plans at their respective companies.

- The result is a continued decline in the BRT’s CEO Economic Outlook Index, which dropped 12 points from last quarter. It’s down 40 points since its peak at the end of last year.

- Still, the most recent reading remains on par with its long-run average and, notably, above the level that would signal a recession.

U.S. employment at their respective companies will grow, 47% of surveyed members said, while 50% said so in the prior quarter.

- 65% expect sales will increase, compared to 72% in Q2.

- 43% plan to increase capital spending, four percentage points fewer than last quarter.

The survey of 170 CEOs was fielded from Aug. 12 to Sept. 7, a period in which inflation numbers cooled, but the Fed was sounding awfully hawkish.

Judging by their expected orders, the survey must have missed Philly-based execs:

Oil Price Rises After Russia Cap Kicks In The West imposed sanctions on Russian crude, pitching the energy conflict with Moscow into an unpredictable new phase that could inject further volatility into global oil markets.

(…) Most-actively traded futures contracts for Brent, the benchmark for international crude sales, gained 1.9% as of Monday morning in London, rising to $87.16 a barrel. Analysts at ING Group ING 0.08%increase; green up pointing triangle said prices got a boost from loosening Covid-19 restrictions in China, which are likely to boost demand in the world’s second-biggest economy. (…)

How Russia responds is the first big unknown for traders and officials. On Sunday, Deputy Prime Minister Alexander Novak said the Kremlin was considering ways in which it could ban companies from applying the price cap, and that output could fall.

“We will sell oil and petroleum products to those countries that will work with us on market terms, even if we have to slightly cut production,” Mr. Novak said in an interview with a state-owned broadcaster. (…)

Europeans Cut Back on Spending, Pointing to Recession Ahead In contrast to the U.S., retail sales in Europe fell sharply as consumers were hit by much higher heating and electricity bills

(…) In response [to higher energy costs], households cut their spending on other goods, with the European Union’s statistics agency Monday recording a 1.8% drop in retail sales from September, the largest fall since July 2021. (…)

ING: “The drop of 1.8% month-on-month was broad-based. We saw declines for both food and non-food retail trade with only fuel sales ticking up. We saw a broad-based decline by country, too. Germany and France both experienced drops of almost 3% while the Netherlands saw a small dip. Spain was the exception among bigger countries with an increase of 0.4%.”

EARNINGS WATCH

During the months of October and November, analysts lowered EPS estimates for S&P 500 companies for the fourth quarter by a larger margin than average. The Q4 bottom-up EPS estimate (which is an aggregation of the median EPS estimates for Q4 for all the companies in the index) decreased by 5.6% (to $54.58 from $57.79) from September 30 to November 30.

In a typical quarter, analysts usually reduce earnings estimates during the first two months of a quarter. During the past five years (20 quarters), the average decline in the bottom-up EPS estimate during the first two months of a quarter has been 2.1%. During the past 10 years, (40 quarters), the average decline in the bottom-up EPS estimate during the first two months of a quarter has been 2.7%. During the past 15 years, (60 quarters), the average decline in the bottom-up EPS estimate during the first two months of a quarter has been 3.5%. During the past 20 years (80 quarters), the average decline in the bottom-up EPS estimate during the first two months of a quarter has been 2.9%.

While analysts were decreasing EPS estimates in aggregate for the fourth quarter, they were also decreasing EPS estimates in aggregate for CY 2023. The bottom-up EPS estimate for CY 2023 declined by 3.6% (to $232.52 from $241.22) from September 30 to November 30. (Factset)

Source:

Source: Apple’s Warning About China Business Shareholders are going to want to know how companies are diversifying risk from the People’s Republic.

The news over the weekend that Apple plans to move much of its iPhone supply chain out of China is the most important signal to date that Western CEOs are wising up about business risks in the People’s Republic. Any corporate board that isn’t doing the same is doing a disservice to shareholders.

Apple hasn’t announced its investment plans. But the Journal reports that the company is telling suppliers that it will move more assembly of Apple products elsewhere in Asia, especially India and Vietnam. This will no doubt be costly given that other countries lack China’s workforce of engineers and network of suppliers. (…)

The greatest risk is Mr. Xi’s determination to swallow Taiwan on his watch—by force if necessary. In that event, the political pressure on Western companies to abandon China would be overwhelming. U.S. firms had to abandon multi-billion-dollar investments in Russia after the invasion of Ukraine, and the example should concentrate minds in corporate boards about China risks.

A buzzword in parts of Europe these days is “China for China,” meaning to locate production for the Chinese market within China but otherwise cordon China off from the rest of the global supply chain to minimize risk. This is a big change for Europe, but it still entails significant financial risk if companies are forced to divest in a hurry. (…)

Iran Disbands Morality Police, Considers Changing Hijab Laws Move is aimed at trying to quiet protests that have taken place across the country, analysts say

(…) President Ebrahim Raisi echoed his remarks in a televised speech Saturday, saying Iran’s Islamic system was enshrined in its constitution but adding, “There are methods of implementing the constitution that can be flexible.” (…)

A decision to formally disband the morality police would likely involve Iran’s Supreme Leader Ali Khamenei, who has strongly defended mandatory hijab in recent years, and the Supreme Council of the Cultural Revolution, a government panel appointed by Mr. Khamenei that created the police force.

“The people’s problem with the Islamic Republic is not only the hijab,” said Azam Jangravi, who was jailed in Iran for protesting against the veil, and now lives in Canada. “Even if they remove the hijab, the people want regime change.” (…)

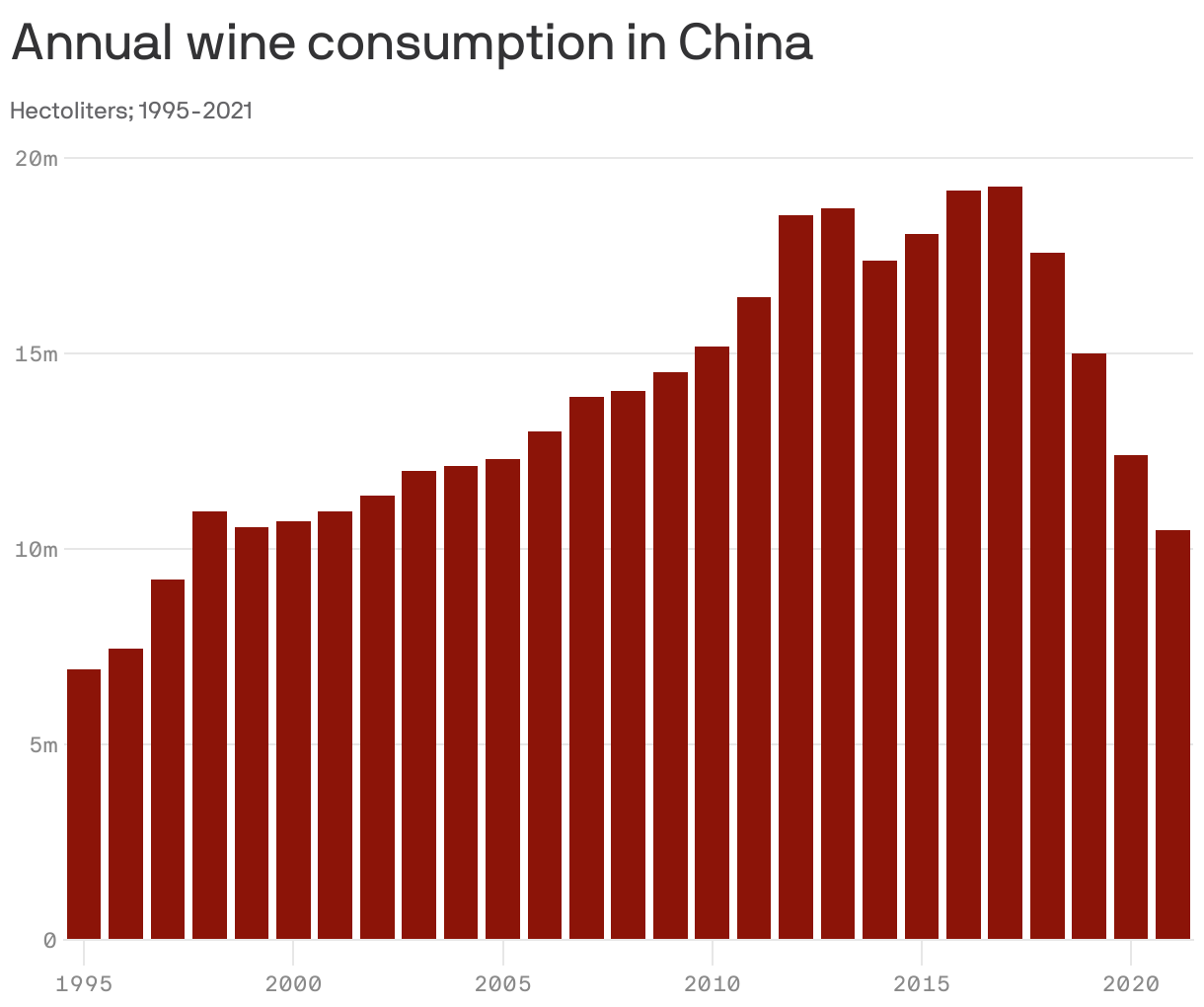

Stop wining!

Chinese wine consumption last year totaled just 10.5m hectoliters. That’s the lowest number since 1997, when China’s population was 200 million smaller and its GDP was a mere 5% of its 2021 size.

In most of the world, wine sales are overwhelmingly to people who want to drink the stuff. That’s not the case in China, where only about 2.5% of adults drink wine at least once a month.

- Instead, most wine is bought by people who don’t intend to drink it. Instead, they give it away as gifts, during festivals like Chinese New Year, the Mid-Autumn Festival, or Singles Day.

- The pandemic caused massive disruption to Chinese gift-giving, as wine fell out of favor. Perhaps people realized the recipients weren’t drinking their gifts.

Just as in the rest of the world, people who drink wine at home ended up drinking more of it during the pandemic. But so far there’s no indication that China’s population is going to become a global force in the wine world. (Axios)

Why other rich nations have surpassed the U.S. in protecting pedestrians, cyclists and motorists.

@fcastofthemonth

@fcastofthemonth