JOLTS: Job Openings Fall Sharply, But Hires Still Increase

Job openings dropped 1,117,000, exactly 10.0% in August (-5.4% y/y). The July increase was revised somewhat to 130,000 from 199,000 reported before. The August decline was the steepest since April 2020, in the midst of the COVID recession. The job openings rate (job openings as a percentage of the sum of establishment employment plus openings) was 6.2% in August, down from 6.8% in July and the lowest since 6.0% in April 2021. These series extend back to December 2000.

The drop in job openings was spread across several industries, with the largest in education and health care, 280,000, but 100,000 or more in manufacturing, retail trade, professional and business services and leisure and hospitality.

New hires rose 39,000 in August after dropping 218,000 in July. The August increase was mainly in leisure and hospitality, up 60,000, especially in accommodation and food services, but there were also increases in manufacturing, retail trade and government.

Quits increased 100,000 while layoffs and discharges rose 70,000, with “other separations” increasing 12,000. The quit rate — that is, the number of quits as a percent of total employment — was 2.7%, the same as in July. The high was 3.0% in November and December of 2021.

Layoffs and discharges, that is, involuntary separations, rose to 1,460,000 in August from 1,390,000 in July; that’s a 5.0% increase and was the largest number since 1,512,000 in March 2021. They had fallen 0.7% in July. The layoff rate was 1.0% in August, up from 0.9% where it had held since October 2021, except for December 2021, when it was 0.8%.

Private-sector job openings dropped 1.028 million in August to 9.037 million (-10.2% m/m, -7.6% y/y). Total private-sector hires rose 34,000 to 5.880 million (+0.6% m/m, -2.1% y/y) while total private-sector separations rose 157,000 to 5.607 million (2.9% m/m, +0.5% y/y).

This is the biggest drop on record, ex-pandemic. Goldman Sachs’ “jobs-workers gap decreased by 0.9pp to 2.5% of the labor force—or 4.0mn workers—in August, a significant drop from its peak of 3.6% of the labor force—or 5.9mn workers—in March.”

- This data echoes the headlines from this morning’s KPMG CEO survey whereby 39% of top CEOs have reportedly instigated hiring freezes. It also means that the ratio of job vacancies to the number of unemployed Americans falls from 1.97 to 1.67. Nonetheless, we have to remember that even after today’s drop there are still 4mn more job vacancies than there are unemployed American while the job opening/unemployed Americans ratio is still more than double the average 0.6 figure seen over the past 20 years. Hence there are still plenty of jobs out there and people are still prepared to move roles for better pay and conditions, with the quit rate staying at 2.7%. (…) As such the jobs market is still incredibly tight, but the Fed will take some satisfaction in today’s direction of travel. While business caution is likely to spread, firings are still a way off – note last week’s initial and continuing claims remain very low by historical standards. Payrolls are still set to post a decent increase on Friday – the market is looking for 265,000 – but with the ISM employment index back in contraction territory and the vacancy data softening the momentum will weaken further in coming months. (ING)

The 2022 KPMG CEO Outlook features insights from more than 1,300 CEOs at large companies globally, including 400 in the United States, on the key challenges and opportunities in driving business growth. Key perspectives from U.S. CEOs are highlighted below.

- 91% believe that there will be a recession in the next 12 months; only 34% of U.S. CEOs think it will be mild and short.

- 79% have expected and planned for a recession. 51% are considering workforce reductions over the next six months in preparation for a potential recession.

- 57% predict 6-10% of anticipated earnings could be impacted by a recession in the next 12 months, while 37% predict 0-5% of anticipated earnings and 6% predict 11-20% of anticipated earnings.

- Over the next six months, U.S. CEOs are confident in the resilience of their companies (83%), the domestic economy (80%) and global economy (72%).

- Long term (over the next three years), CEOs are confident in the growth prospects of the domestic economy (93%) and their company (95%), but fewer are confident in the global economy (71%).

![]() Amazon Freezes Hiring in Retail Division The company has been dealing with slowing growth in its retail segment this year.

Amazon Freezes Hiring in Retail Division The company has been dealing with slowing growth in its retail segment this year.

Small businesses represent nearly 95 percent of all U.S. employers. Monitoring their performance — the number of people they employ and wages they’re paying — is an important indicator of the health and direction of the overall economy. The Paychex | IHS Markit Small Business Employment Watch draws from the payroll data of approximately 350,000 Paychex clients to gauge small business wage and employment trends on a national, regional, state, metro, and industry basis.

Hourly earnings growth for workers of U.S. small businesses slowed in September, according to the latest Paychex | IHS Markit Small Business Employment Watch. Hourly earnings growth stood at 4.98 percent in September, falling below 5 percent for the first time since April. The Small Business Job Index, which measures the rate of small business job growth, also slowed slightly from the previous month, down -0.19 percent to 99.75.

“Decreasing for the seventh consecutive month, the jobs index is now below its level from one year ago,” said James Diffley, chief regional economist at IHS Markit.

“With low unemployment levels continuing, small businesses are relying on their current staff to do more, driving an increase hours worked,” said Martin Mucci, Paychex chairman and CEO. “The moderation in hourly earnings growth is of particular note, though, as it may be a sign that the Fed’s actions are possibly having an impact in the battle against inflation.”

In further detail, the September report showed:

- One-month annualized hourly earnings growth fell to 3.35 percent, the weakest growth rate since April 2021.

- Small business employment gains slowed during the spring and summer as monthly decreases averaged -0.26 percent from April through September.

Small business employment

SERVICES PMIs

Eurozone: Private sector output falls at sharpest rate since January 2021

Any hopes of the eurozone avoiding recession are further dashed by the steepening drop in business activity signalled by the PMI. Not only is the survey pointing to a worsening economic downturn, but the inflation picture has also deteriorated, meaning policymakers face an increasing risk of a hard landing as they seek to rein in accelerating inflation.

Business activity has now deteriorated for three successive months, indicating falling GDP, with the rate of decline gathering momentum over the third quarter. A worsening of business expectations for the months ahead and a worryingly steep loss of orders currently point to an even sharper decline in GDP in the fourth quarter.

Soaring inflation, linked to the energy crisis and war in Ukraine, is destroying demand at the same time that business confidence is slumping to levels not seen since the region’s debt crisis in 2012, excluding pandemic lockdowns. Companies and households alike are therefore cutting back on discretionary spending and investment in preparation for a harsh winter.

Private sector business activity across the euro area fell at the sharpest pace since January 2021 in September, extending the downturn into a third straight month. Output in both the manufacturing and service sectors fell at a quicker rate as high inflation, soaring energy costs, rising economic uncertainty and weakening demand drove the euro area economy into a deeper contraction. Total new orders fell to the greatest extent in almost two years, while a considerable drop was seen in export sales.

Employment growth continued to slow in September, reflecting a lack of incoming new work and a sustained drop in the level of outstanding business.

For the first time since March, cost pressures intensified, primarily reflecting sharply rising energy costs and higher wages. Concerns surrounding the economic outlook grew, with business confidence slumping to its lowest level since the first COVID-19 wave in 2020.

The seasonally adjusted S&P Global Eurozone Composite PMI Output Index posted below the crucial 50.0 mark in September for a third successive month, signalling a sustained downturn in business activity across the euro area private sector. At 48.1, this was down from 48.9 in August and pointed to the fastest decline in output since January 2021.

Sector data revealed another broad-based decrease at the end of the third quarter, with contractions accelerating at both manufacturers and service providers. The downturn was stronger at goods producers as high energy costs, ongoing issues with input availabilities and order cancellations impeded production volumes at eurozone factories. Nevertheless, high inflation was also a notable hindrance to services companies during the month.

Overall intakes of new business fell for a third straight month in September, and the rate of decline was the strongest since November 2020.

Of the monitored eurozone constituents, only two saw private sector output grow in September. In Ireland, the rate of expansion edged up slightly. France also recorded an improvement in activity levels, but one that was weak overall and significantly softer than those seen earlier in 2022 following the lifting of COVID-19 restrictions.

Elsewhere, economic trends worsened in September. Spain recorded its first decrease in business activity since January, while the downturn in Italy accelerated. In Germany, private sector output levels fell at a rate which, excluding pandemic-hit months, was the sharpest since the global financial crisis in 2008-09.

A key factor pulling back demand was inflation, according to surveyed companies. This was especially evident in the manufacturing sector, where factory orders dropped at the quickest pace in almost two-and-a-half years. Overall cost pressures intensified during September, marking the first month in which inflation has accelerated since March. This primarily stemmed from energy prices, although mentions of rising material prices and wages were also seen. In response, selling prices were raised once again in September. The rate of output price inflation was the strongest for three months as companies opted to pass higher cost burdens on to their clients.

In another sign of growing economic weakness, demand for euro area goods and services from non-domestic customers also fell at a considerable pace in September. Overall, new export business declined at the strongest pace since June 2020.

Business confidence across the euro area sank to its lowest level since the initial outbreak of COVID-19 amid growing fears of recession, concerns around a prolonged period of high inflation and the prospect of further spikes in energy costs. The outlook was particularly gloomy among manufacturers, who were pessimistic as a whole towards the next 12 months.

Lower business confidence fed through to hiring decisions in September, with the rate of job creation across the euro area slowing to an 18-month low. Backlogs of work also fell further as lower new business intakes enabled firms clear some of their outstanding business.

The S&P Global Eurozone Services PMI Business Activity Index fell to 48.8 in September, down from 49.8 in August to its lowest level since February 2021. Overall, this marked back-to-back monthly decreases in services activity across the euro area.

The volume of incoming new business continued to fall at the end of the third quarter. The rate of decrease was unchanged from August, which was the sharpest in a year-and-a-half. Nonetheless, the rate of contraction was modest overall.

Weak demand conditions were underscored by a renewed reduction in backlogs of work. Latest survey data signalled the first drop in outstanding business volumes since March 2021. Employment levels continued to rise across the euro area service sector, although the rate of job creation was the joint-slowest since April 2021.

Meanwhile, price pressures intensified in September. Rates of input cost and output charge inflation accelerated to three-month highs. Lastly, business confidence slumped to a level unseen since the start of the COVID-19 pandemic.

Global Trade Slowdown Points to Possible Recession, Lower Inflation World trade in goods is set to slow more sharply than previously expected next year, possibly easing inflationary pressures but raising the risk of a global recession, the World Trade Organization said.

With the surge in energy costs and rising interest rates weakening household demand, exports and imports should increase by just 1% in 2023, down from a previous forecast of 3.4%, the World Trade Organization said Wednesday.

A slowdown in trade flows driven by weakening demand could help bring down price pressures by unblocking supply chains and reducing transport costs. It also means there is an increased risk that the global economy will contract. (…)

The WTO also lowered its forecast for global economic growth in 2023 to 2.3% from 3.3%, and warned of an even sharper slowdown should central banks raise their key interest rates too sharply.

“One has to watch out if there are supply-side constraints that are not responsive to interest rates,” Ms. Okonjo-Iweala said. “There is a danger you could overshoot.” (…)

The Organization for Economic Cooperation and Development on Tuesday said the annual rate of inflation across the Group of 20 largest economies was unchanged at 9.2% for the third straight month in August. (…)

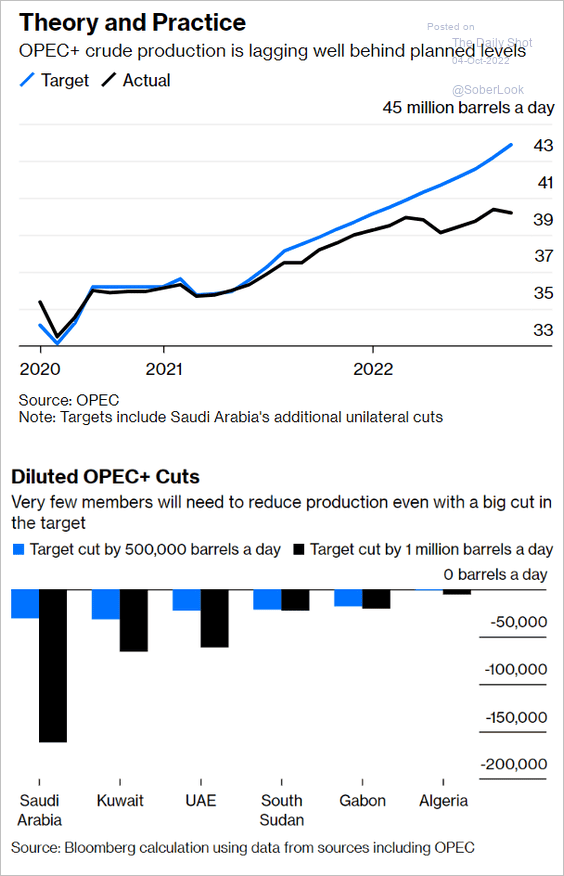

UAE set to support Saudi Arabia and Russia on oil output cuts Influential Gulf state’s backing ahead of Opec+ meeting could hinder US efforts to stop deal

- Saudi Aramco chief sounds alarm over global oil capacity Head of world’s biggest producer says ‘world should be worried’ about supply limitations

Manhattan’s Housing Market Is Starting to Cool With Sales Stalling

Sales of co-ops and condos dropped 3.7% in the third quarter from the previous three months and more than 18% from a year earlier, appraiser Miller Samuel Inc. and brokerage Douglas Elliman Real Estate said in a report Tuesday. The median price on transactions completed slipped 7.6% to $1.15 million from the second quarter. (…)

The number of Manhattan homes entering contract in September was down roughly 32% from a year earlier, the sixth consecutive month of year-over-year decreases. The high-end part of the market has been hit the hardest, with contracts for homes priced at $4 million or more falling nearly 50% in September from a year earlier. (…)

The median price was up 3.6% from the same time a year ago. The number of closings, while down from last year, was 14.3% higher than the third-quarter average of 3,231 over the previous decade.

The benchmark price for a home in Canada’s largest city fell a further 1.2% from August, adding to the string of declines that began in April, according to data released Wednesday from the Toronto Regional Real Estate Board. (…) Only 5,038 homes were sold during the month, down 44% from a year earlier. (…)

New listings fell to their lowest level for the month of September in 20 years, the real estate board said. (…)

Meanwhile, in Vancouver, long Canada’s most expensive real estate market, benchmark prices fell 2.1% in September, bringing the cumulative decline in the last six months to 8.5%. But sellers were still coming to market, with new listings up 27% from the month before, according to data from the city’s real estate board.

China’s Covid-19 cases climbed to the highest in more than two weeks as outbreaks during a week-long holiday spark worries ahead of the politically significant Party Congress

Micron to Spend Up to $100 Billion on Chip Factory in New York The semiconductor plant in Clay, N.Y., would be the largest in the U.S., as Washington tries to boost the industry.

(…) Micron’s new New York and Idaho factories would raise the portion of the company’s production in the U.S. to 40% from 10% in about 10 years, Mr. Mehrotra said in an interview. (…)

(…) Intel Corp. and Texas Instruments Inc. also have unveiled chip-factory investments in the U.S. in recent months, among a host of companies evaluating plant-building in the U.S. to tap new federal and state incentives. (…)

Europe has its own chip-industry funding in the pipeline and is aiming to double its share of the global market to 20% by 2030. Some of the world’s largest non-U.S. chip makers, including Taiwan Semiconductor Manufacturing Co. and South Korea’s Samsung Electronics Co., have laid out plans for hundreds of billions of dollars of manufacturing growth in the coming years, with their sights set on a bigger share of a lucrative market where the cost of manufacturing is climbing sharply.

Samsung’s contract chip-making business said this week that it planned to increase its manufacturing capacity for the most advanced chips by 70% a year. (…)