PMI drops to lowest since July 2020 amid further loss of new orders

The US manufacturing sector experienced relatively muted operating conditions in August, according to latest PMITM data from S&P Global. Output contracted for a second straight month as new orders fell for a third month in a row amid weak client demand, in turn linked to the impact of inflation and economic uncertainty on customer spending. Although employment rose further, it did so at the slowest pace since January, with backlogs of work rising only marginally. Output expectations strengthened from July’s recent low, but stayed below the series trend.

Supply chain disruptions meanwhile remained historically marked, but the extent to which lead times lengthened was the least severe since October 2020. As a result, pressure on costs moderated, with input prices increasing at the slowest pace since the start of 2021. In an effort to drive sales and pass on some of the moderation in cost burdens, selling prices rose at the weakest rate for a year-and-a-half.

The seasonally adjusted S&P Global US Manufacturing Purchasing Managers’ Index™ (PMI™) posted 51.5 in August, broadly in line with the earlier released ‘flash’ estimate of 51.3, but down from 52.2 in July. The headline index reading was the lowest since July 2020, with latest data indicating subdued overall health conditions across the US manufacturing sector.

Contributing to weak operating conditions was a third successive monthly fall in new orders in August. Manufacturers registered a modest decline in new sales, often linking this to muted client demand following greater economic uncertainty and hikes in prices. The rate of decrease was broadly in line with those seen in June and July. External demand remained weak, as new export orders fell at the second-sharpest pace in 27 months.

In line with weak demand conditions, goods producers indicated a back-to-back decline in production. The pace of contraction quickened from July to the fastest since June 2020. Some companies also noted that ongoing supply chain disruption hampered output amid raw material delivery delays.

On the price front, average cost burdens increased at a further marked rate in August. Hikes in transportation, fuel and metals prices reportedly drove inflation. That said, a number of firms noted reduced costs for some materials, which contributed to the softest overall rise in operating expenses since January 2021.

In response to softer increases in costs, firms raised their selling prices at a weaker rate in August. The pace of charge inflation was the slowest in 18 months, as some companies passed through savings to their customers in an effort to remain competitive.

Vendor performance deteriorated again, but at the slowest rate since October 2020. Nonetheless, transportation and logistics issues remained evident.

Input buying was broadly unchanged on the month in August. Weak client demand and deliveries of materials led to a quicker rise in pre-production inventories. Stocks of finished goods meanwhile fell, as orders were shipped in a timely manner and stock building was not prioritised.

Meanwhile, employment rose at the second-slowest rate in over two years. Backlogs of work also grew at a subdued pace, as weak new order inflows led some firms to delay replacing leavers despite some reports of ongoing challenges finding suitable candidates.

Lastly, output expectations picked up in August, with the degree of confidence in the year-ahead outlook reaching a three-month high. Despite hopes of an uptick in demand, the level of optimism was weaker than the series average.

The ISM is more upbeat:

For a second straight month, the Manufacturing PMI® figure is the lowest since June 2020, when it registered 52.4 percent. The New Orders Index registered 51.3 percent, 3.3 percentage points higher than the 48 percent recorded in July. The Production Index reading of 50.4 percent is a 3.1-percentage point decrease compared to July’s figure of 53.5 percent. The Prices Index registered 52.5 percent, down 7.5 percentage points compared to the July figure of 60 percent; this is the index’s lowest reading since June 2020 (51.3 percent). The Backlog of Orders Index registered 53 percent, 1.7 percentage points above the July reading of 51.3 percent.

After three straight months of contraction, the Employment Index expanded at 54.2 percent, 4.3 percentage points higher than the 49.9 percent recorded in July. The Supplier Deliveries Index reading of 55.1 percent is 0.1 percentage point lower than the July figure of 55.2 percent.

(…) companies continued to hire at strong rates in August, with few indications of layoffs, hiring freezes or head-count reductions through attrition. Panelists reported lower rates of quits, a positive trend. (…)

WHAT RESPONDENTS ARE SAYING

- “Demand from customers is still strong, but much of that is because there is still fear of not getting product due to constraints. They are stocking up. There will be a reckoning in the market when the music stops, and everyone’s inventories are bloated.” [Computer & Electronic Products]

- “Sales in target business softening month-over-month, down 12 percent by revenue. Inventory days are increasing.” [Chemical Products]

- “Strong sales continue. The impact of the chip shortage is slowing, and the decreasing COVID-19 resurgence in Asia is now affecting production more than chips.” [Transportation Equipment]

- “Supply in most groups is slowly increasing, but demand appears to be outpacing — causing pricing to either stabilize or increase.” [Petroleum & Coal Products]

- “Inventories are far too high, and we are on pins and needles to see how quickly and at what magnitude our busy season begins. We will start seeing that in the next few weeks.” [Food, Beverage & Tobacco Products]

- “Continue to struggle with electronic component shortages. Several smaller machine shops are (manufacturing) the pacing item for our production due to lack of direct labor machinists.” [Machinery]

- “Overall, I have seen much improvement in the availability of raw materials. However, trucking issues continued, and production capacity within some industries remains tight. I have growing concerns that as cement and mineral companies run ‘all out’ to meet demand, we will see more downtime due to maintenance (issues).” [Nonmetallic Mineral Products]

- “Demand is softening; however, we are continuing to produce to replenish inventory.” [Primary Metals]

- “Orders are still strong through the end of the year, but there is a feeling that customers may start pulling back on orders, either cancelling them or pushing them into 2023.” [Plastics & Rubber Products]

- “Business conditions are good, and demand is strong. Securing enough raw material supply to keep up is still a challenge.” [Miscellaneous Manufacturing]

You may have noticed that, in spite of the ISM’s more upbeat report vs S&P Global’s, I have highlighted the more negative comments from ISM respondents. That is because I put more weight on S&P Global surveys which have proven more accurate in the past decade.

“The ISM is only surveying large companies while the S&P Global survey covers small, medium and large companies in the correct proportions, as defined by the official data. The S&P Global survey is also the only survey to incorporate a national weighting system for its survey responses based on company size and sector contribution to total manufacturing output, ensuring each company’s response contributes appropriately to the survey index each month.”

That said, the ISM reach remains deep and wide. The WSJ, like all other media and sell-side reports I have seen, only mentions the ISM survey:

Stocks extended their drop after the Institute for Supply Management reported some good news. Business activity continued to expand in August, while the prices that companies reported paying dropped more than expected.

Why is the market trading lower?

“Good news is being traded as bad insofar as it provides Powell further cover to continue aggressively tightening policy,” writes Ian Lyngen, head of U.S. rates strategy at BMO Capital Markets.

Joseph Brusuelas, chief economist at RSM US, agrees, saying the data “does not read like one where the economy is either in or soon will be falling into recession.” Given the strength of the economy, the Fed has a case to keep up aggressive policy tightening, Mr. Brusuelas writes.

Nobody mentioned S&P Global’s PMI which was pretty economy bearish:

- New orders fell for a third month in a row amid weak client demand

- External demand remained weak, as new export orders fell at the second-sharpest pace in 27 months.

- Employment rose at the second-slowest rate in over two years

Hopefully, the Fed looks at both surveys…

…Although, yesterday, the Atlanta Fed boosted its Q3 GDPNow estimate from 1.6% to 2.6% “after this morning’s construction spending release from the US Census Bureau and this morning’s Manufacturing ISM Report On Business from the Institute for Supply Management.” July construction spending fell 0.4% MoM after -0.5% in June. All of the boost in the GDPNow estimate, and then some, came from the “strong” ISM number…

A similar situation occurred in late 2018-early 2019 when IHS Markit PMI, now S&P Global, was alone in accurately predicting the decline in output registered by the official data in the first quarter of 2019.

This ING chart also suggests that the recent ISM numbers are likely optimistic:

US and Chinese manufacturing purchasing managers’ indices

Other world PMI surveys are all from S&P Global and consistent with the U.S. PMI.

Yesterday, we saw that China, the Eurozone and the UK all reported very weak manufacturing survey data, all with very weak new orders.

Now Canada is joining the list:

Canada: Manufacturing conditions deteriorate for first time in over two years

August data revealed the first downturn in operating conditions across the Canadian manufacturing sector since the COVID-19 pandemic began in the first half of 2020. The deterioration in performance reflected sharp and accelerated contractions in output and new orders and the first fall in employment in over two years. At the same time, renewed declines were recorded in buying activity, backlogs and pre-production inventories. Subsequently, optimism towards output in the year ahead moderated with concerns over the macroeconomy weighing slightly on sentiment.

There were, however, positive signs on the price front where output and input price inflation eased to 18- and 19-month lows, respectively. Nevertheless, rates of inflation in both cases were above trend.

The seasonally adjusted S&P Global Canada Manufacturing Purchasing Managers’ Index® (PMI®) registered at 48.7 in August, down from 52.5 in July,thus indicating a deterioration in manufacturing performance. The latest fall was only modest but ended a 25-month sequence of growth.

A key reason for the latest decline was a marked and accelerated fall in new orders. Firms indicated that client hesitancy, growing uncertainty and a general lull in domestic demand conditions were behind the latest reduction in new orders.

Similarly, international demand for Canadian manufactured goods weakened in August. In fact, exports fell sharply and at the quickest rate since June 2020.

Meanwhile, manufacturing production declined for the second month in succession. The rate of decline was sharp and the quickest since June 2020 amid weak inflows of new work. Firms also indicated that supply-chain difficulties persisted to impact production. (…)

Turing to prices, average cost burdens rose once again in Canada’s private sector, with 35% of panellists reported higher costs in August compared to July while only 7% saw them fall. Higher transportation and material costs were overwhelmingly mentioned by panellists.

Output charges also continued to rise midway through the quarter. The rate of increase was marked compared to the historical average with panellists blaming sustained increases in cost burdens.

That said, input cost and output charge inflation eased to 19-and 18- month lows, respectively. (…)

(…) That should happen on Sept. 7, with money markets leaning toward a hike of 75 basis points, which would take the policy rate to 3.25%. That would be the fourth oversized rate increase this year, capping 300 basis points of tightening since March.

Some economists predict the Canadian central bank may signal a pause after its anticipated hike next week, especially after the release on Wednesday of GDP data that suggested the economy may be cooling faster than expected. (…)

U.S. Light Vehicle Sales Ease During August

The Autodata Corporation reported that light vehicle sales during August fell 1.0% (+1.4% y/y) to 13.37 million units (SAAR) from 13.50 million in July. Sales remained roughly one-quarter below the April 2021 peak. Vehicle sales comprise about four percent of real consumer expenditures.

Sales of light trucks led last month’s overall decline, falling 2.2% (+3.8% y/y) to 10.44 million units following a 2.8% July gain. (…)

Auto sales rose 3.5% during August (-6.4% y/y) to 2.93 million units, a four-month high, after holding steady in July. (…)

Imports’ total share of the U.S. vehicle market rose to 24.8% in last month, the highest level in six months. (…)

Wards Auto estimates sales of 13.18M in August per CalculatedRisk.

America Could Face Its Own Gas Crisis, or Worsen Europe’s Summer heat is still lingering in the U.S., but a peek at domestic natural-gas prices is a chilling reminder

U.S. natural gas inventories inched up by 61 billion cubic feet in the week ended Aug. 26, according to data released Thursday morning by the Energy Information Administration. That leaves stockpiles 11.3% lower than their five-year average—a gap that has widened throughout the so-called injection season, when natural-gas inventory builds up ahead of winter. (…)

There are still two months left in the seven-month injection season, but natural-gas prices are already at levels last seen in 2008, a year when the U.S. was producing 43% less of the fuel than it did in 2021. U.S. natural gas benchmark Henry Hub futures briefly touched $10 per million British thermal units last week. Prices edged up slightly after the EIA’s storage report on Thursday morning to roughly $9.17 per MMBtu. The sticker shock is far worse in Europe, where front-month natural-gas futures are trading at the equivalent of roughly $70 per MMBtu as Russia chokes off supplies. (…)

And then there is the potential for resource nationalism that could compound Europe’s woes. Last year, an industry group representing manufacturers urged the Energy Department to require a reduction in LNG exports to allow the U.S. to fill up more natural gas in storage. Although the DOE hasn’t commented on LNG exports thus far, Energy Secretary Jennifer Granholm did send a letter to oil refiners urging them to focus on building U.S. inventories.

Even the best friendships can be chilled when the mercury drops.

BTW: U.S. oil demand keeps falling, not a sign of a strong economy, but supply is declining just as rapidly:

(Princeton Energy Advisors)

World Food Prices Extend Drop as Supply Uptick Offers Relief

FYI:

- At the close of [August], a portfolio comprised of 60% stocks and 40% bonds, as measured by the S&P 500 and Bloomberg U.S. Aggregate Index, respectively, is nursing a 13.9% year-to-date loss, notes Compound Capital Advisors founder Charlie Bilello. That’s by far the worst such showing on record going back to 1976, exceeding the 9.5% and 6.1% losses incurred by that 60/40 strategy over the first eight months of 2002 and 2008, respectively. (ADG)

- Chinese firms have defaulted on $37.3 billion of offshore debt so far in 2022, data from Bloomberg show, exceeding the combined total of the past four full years. (ADG)

Apple overtakes Android to pass 50% share of smartphones used in US

Apple overtakes Android to pass 50% share of smartphones used in US- Supreme Court approval craters

Just 28% of Democrats and Democratic-leaning independents view the court favorably — down 18 points from January, and nearly 40 points since 2020. Positive views of the court among Republicans and Republican leaners ticked up since the beginning of the year — 73%, up eight points from 65%. (Axios)

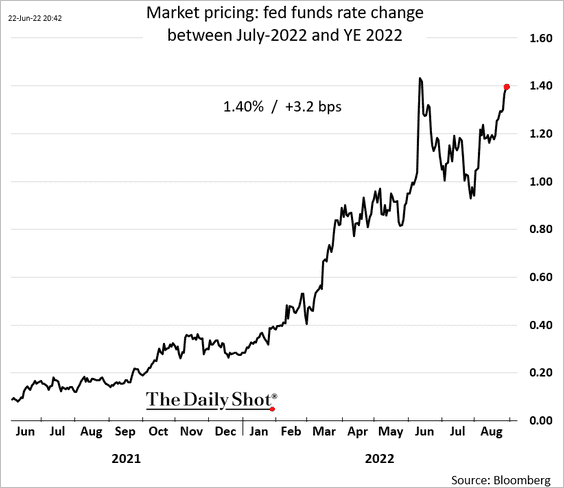

(The Market Ear)

(The Market Ear)