U.S. Growth Shows Signs of Slipping Recession fears creep in as key sectors such as housing and consumer spending succumb to high inflation and rising interest rates

Recent reports show sharp declines in key sectors, raising the prospects of a stalled economic recovery and possibly a recession. Home construction across the U.S. fell sharply in May, the Commerce Department said Thursday. Factories in the mid-Atlantic region reduced activity for the first time in two years this month, the Federal Reserve Bank of Philadelphia said. And Americans broadly cut spending at retailers for the first time this year in May, the Commerce Department said earlier this week. (…)

“There really is no road map here,” said Joshua Shapiro, chief U.S. economist at the New York consulting firm Maria Fiorini Ramirez, Inc. “Nobody knows. Anybody that pretends they know is just telling you a story.” (…)

Here’s what we do know:

- inflation is too high, “unhealthy” per Jay Powell who has made it his priority to bring it down quickly;

- the Fed can’t act directly on food and energy prices but it sure can reduce overall demand;

- wages are accelerating thanks to a very unbalanced labor market: too much demand, too little supply;

- only a recession can effectively reduce consumer demand, corporate need for labor and incentivise people to work, all at once;

- Mr. Powell is focused on the task and has warned us that “there will be pain”.

Here’s what we don’t know:

- when the recession, how long and how severe? It may already have started and the sooner the better;

- where will inflation settle, given the numerous supply issues?

More than 60% of executives see a recessionary period in next 12 to 18 months, according to the Conference Board survey

![]() There is a caveat, courtesy of Nordea:

There is a caveat, courtesy of Nordea:

We suspect that the real economy will be less sensitive to a rise in interest rates this time, which means that the Fed could have to move rates more-than-expected before policy gets restrictive. The strongest argument is that the household balance sheets are in a much better shape to sustain their level of spending as the massive injections of money and credit through both monetary and fiscal stimulus have changed household balance sheets dramatically.

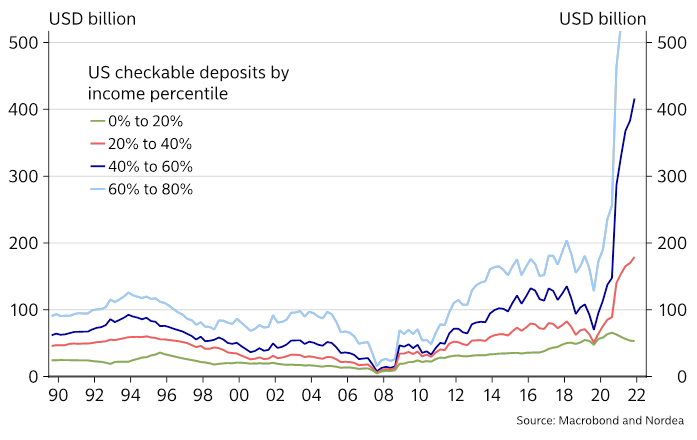

Households in the US have accumulated more than USD 2.5 trillion in excess savings during the pandemic. While a lot of the savings are concentrated among the rich, lower income groups have also saved up a lot. This could mean households that are much more resilient to inflation and higher interest rates, since consumers can continue to spend by dipping into these savings. This also means that nominal spending will continue to be too strong.

Large savings buffer against economic headwinds

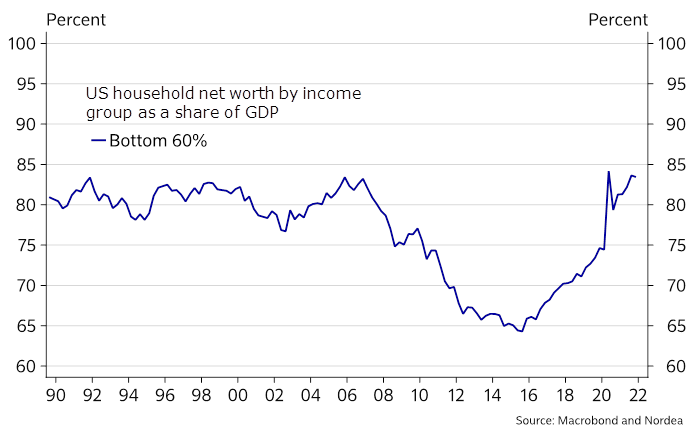

In addition to that, both financial and nonfinancial assets have soared increasing household assets, at a time when households have paid down their debt level. This has resulted in personal disposable income closing a gap of .35 percentage-point (back in 2008) to household liabilities. In sum, these balance sheet changes have contributed to a strong bounce in wealth accumulated by the low- and middle-income cohort (bottom 60% by income), a group which has been squeezed throughout the last decade.

Decade high net worth

![]() Not good news, actually. Like delaying going to the dentist…

Not good news, actually. Like delaying going to the dentist…

Nobody knows how high rates will need to move to cool the economy. We suspect that it will take quite a lot, and that the monetary tightening will continue to be quite a challenge for policy makers and financial markets. Central banks are forced to choose between two undesirable outcomes: Tighten to control inflation at the cost of tipping the economy into a recession, or do not tighten and allow inflation to erode real growth.

The June meeting showed us that the FOMC is clearly in the former camp. There is a distinct possibility that we will see policy rates well north of 4% during next year. While the market will try to time the peak in the fed funds rate and look for the next downturn, the Fed’s balance sheet reduction will move the supply/demand balance in the Treasury market towards a steeper curve. Higher policy rates will also make it less attractive for foreign investors to buy USD bonds. We therefore do not believe the rate curve will invert too much, and certainly not to the extent projected by current market pricing.

On the other hand, about those savings, Bespoke asks a good question:

Would you call the largest destruction of wealth in modern market history a “soft landing”?

@bespokeinvest

U.S. Housing Starts Fall Sharply in May

New residential building activity is feeling the pressure from rising interest rates. Housing starts declined 14.4% during May (-3.5% y/y) to 1.549 million units (SAAR) from 1.810 units in April, revised from 1.724 million. The Action Economics Forecast Survey expected 1.71 million starts.

Single-family starts declined 9.2% (-5.3% y/y) last month to 1.051 million units from 1.157 million in April, revised from 1.100 million. Starts of multi-family units weakened 23.7% (+0.6% y/y) to 498,000 from 653,000.

By region, housing starts were mixed last month. Starts in the South declined 20.7% (-0.7% y/y) to 803,000. In the West, housing starts fell 17.8% (-10.1% y/y) to 356,000. Elsewhere, starts firmed. In the Northeast, starts surged 14.6% (26.3% y/y) to 173,000. Starts in the Midwest rose 1.9% (-17.5% y/y) to 217,000.

Building permits declined 7.0% (+0.2% y/y) to 1.695 million from 1.823 million in April. Permits to build single-family homes declined 5.5% (-7.9% y/y) in May to 1.048 million units. Permits to build multi-family weakened 9.4% (+17.0% y/y) to 647,000.

- Mortgage Rates Hit 5.78%, Highest Level Since 2008 U.S. mortgage rates reached their highest levels in more than 13 years, the latest sign of market tumult tied to the Federal Reserve’s campaign to cool inflation.

Sharply reduced affordability is curbing demand.

Housing units under construction have peaked and will likely decline given lower permits. Housing supply will grow in the second half but construction employment should wane.

Tesla Raises Prices Amid Surging Costs Prices on some of the company’s electric cars are going up by as much as $6,000. The latest price increase applies to certain cars across Tesla’s entire lineup.

(…) The company last raised prices in March, soon after Mr. Musk warned in a tweet that Tesla and his Space Exploration Technologies Corp., or SpaceX, “are seeing significant recent inflation pressure in raw materials & logistics.” (…)

Between 10% and 15% of Tesla’s cost structure is exposed to swings in raw-materials prices, finance chief Zachary Kirkhorn said in April. The rate of cost increases accelerated in the first quarter and the first few weeks of the second quarter, he said, adding that it will take time to impact Tesla’s bottom line because of fixed contracts with suppliers. (…)

U.S. Philadelphia Fed Index Turns Negative in June

The Federal Reserve Bank of Philadelphia’s Manufacturing Business Conditions Index declined to -3.3 during June from +2.6 in May. It was the first negative reading since May 2020. The Action Economics Forecast Survey expected an improvement to 6.0. The percentage of firms reporting improved conditions fell to 16.3% from 22.2% in May. The share reporting weaker conditions was fairly steady at 19.6%. Responses to this month’s survey were collected from June 6 through June 16.

Haver Analytics calculates an ISM-Adjusted General Business Conditions Index from five key components using the same methodology as the national ISM index. The index fell to 53.3 this month from 59.9 in May.

Performance of the sub-indexes remained mixed. The new orders index declined to -12.4 this month from +22.1 in May. The unfilled orders index declined to -7.0 from +17.9 last month. The inventories series weakened to -2.2 from +3.2 in May. (…)

The average workweek measure fell to 11.8 this month from 16.1 in May.

Moving higher was the employment measure to 28.1, which came after May’s drop to 25.5 from the record 41.4 in April. An improved 31.3% of respondents raised employment versus 26.7% in May, while 3.2% reduced payroll sizes after 1.2% did so in May.

Inflation pressures eased. The prices paid reading declined to 64.5 after falling to 78.9 in May. A lessened 70.1% of respondents reported paying higher prices while 5.6% reported paying lower prices. The prices received index declined to 49.2 in June, the lowest level since January.

The Philadelphia Fed also surveys expectations for business activity in the coming six months. The expectations index for future activity collapsed to -6.8 in June. It reached a high of 69.2 twelve months ago. All of the sub-indexes declined m/m. New & unfilled orders, along with delivery times and inventories were greatly negative. Expected prices paid eased slightly from after a sharp decline in May.

The Empire State Manufacturing Index of General Business Conditions rebounded modestly in June after a sharp decline in May. The index increased 10.4 points to -1.2 in June from -11.6 in May. The June reading indicates that general business conditions were essentially unchanged in the month. The Action Economics Forecast Survey had anticipated an increase to 3.4. The index has posted a negative reading in three of the past four months. The percentage of respondents reporting an increase in business conditions increase to 27.6% from 19.9% in May while the percentage reporting a decrease eased to 28.8% from 31.5% in May. The latest survey was conducted between June 2 and June 9. (…)

Both the new orders index and the shipments index rebounded to above zero in June. New orders rose to 5.3 from -8.8 in May and shipments increased to 4.0 from -15.4 in May. The percentage reporting an increase in new orders rose to 34.6% from 24.9% while the percentage reporting an increase in shipments increased to 30.7% from 22.0%. Percentages reporting declines fell for both new orders and shipments. (…)

The number of employees index increased to 19.0 in June from 14.0 in May. The percentage of respondents increasing employment rose to 24.5% from 20.9% while the percentage reducing employment fell to 5.5% from 6.8%. By contrast, the average workweek index fell to 6.4 in June from 11.9 in May.

Inflation indicators remained elevated. The prices paid index rose to 78.6 in June from 73.7 in May after having reached a record 86.4 in April. The prices received index fell for the third consecutive month—to 43.6 in June from 45.6 in May and 49.1 in April. These are still some of the highest readings for these two variables in their history which dates back to 2001.

Looking ahead to the next six months, respondents’ optimism waned, declining to 14.0, the lowest reading since April 2020, from 18.0 in May with declines rather broadly spread across components.

Coincidentally, the NY Fed published its Business Leaders Survey, covering service firms in New York, northern New Jersey, and southwestern Connecticut. The survey was done between June 2 and June 9.

Growth stalled in the region’s service sector, according to firms responding to the Federal Reserve Bank of New York’s June 2022 Business Leaders Survey. The survey’s headline business activity index fell nine points to 2.2. The business climate index also fell, moving down nine points to -36.2, indicating that firms generally viewed the business climate as worse than normal for this time of year. Employment levels continued to grow at a solid clip, and wage increases remained widespread. The prices paid index reached a new record high, and the prices received index remained near its recent peak.

Looking ahead, optimism continued to wane, with firms turning pessimistic about the expected future business climate.

Russian gas flows to France via Germany halted, says pipeline operator

ECB: The hawks are in control

(…) Against an increasingly hawkish central bank amidst mounting signs of price pressures becoming more broad-based, we [Nordea] think that the ECB will hike by 50bp both in September and October. Euro-area inflation should peak during the autumn, allowing the central bank to go back to 25bp steps in December. We expect the ECB deposit rate to rise to 1.75% during the first half of next year, roughly in line with our estimates of the neutral interest rate. Given the headwinds facing the economy, including high energy prices, higher interest rates and likely some further Covid-waves next winter, and falling inflation at that time, we think that the ECB will stop its hikes at around the neutral rate.

While we see risks both ways, risks are tilted towards the central bank stopping its hikes already earlier, if the geopolitical risks materialise, the economy slows down more clearly and inflation recedes quickly. (…)

SENTIMENT WATCH

The worst bout of selling in S&P history

In the past seven sessions, more than 90% of stocks in the index have declined on five days. Since 1928, that has never happened before. This is the most overwhelming display of selling in history.

There have been a handful of times when there was a majority of days with more than 90% declining stocks, clustered in the 1930s and post-financial crisis eras. Forward returns were very volatile after these signals, but all preceded a higher price in the S&P 500 6 or 12 months later.

Over the past five days, fewer than 1.6% of stocks in the index have held above their 10-day moving averages. That has been matched only twice before in recent decades. Both endured extremely volatile and choppy conditions for months before experiencing excellent long-term gains.

The push lower on Wednesday made investors in many stocks finally capitulate, so more than 43% of stocks in the S&P fell to 52-week lows on the same day. In recent decades, that has been exceeded only by October/November 2008, December 2018, and March 2020.

What the research tells us…

Well, pretty much the same as it has been all week. We are in a bear market, everything is horrible, and there is no sustained interest among buyers. Every bullish setup gets met immediately with a slap upside the head. About the only potential silver lining is just how bad things have become. The level of selling pressure we’ve seen this week has been rarely – if ever – matched in many decades. One-sided behavior like this has a strong history of being contrarian…but that was also the case in May, and here we are at lower lows. So for new buyers, it seems like patience is a better virtue, and for existing holders, it seems as though it’s too late to sell.

And this from Goldman Sachs:

Retail investors have turned into sellers in recent months — with one exception. “There’s been a very dramatic reversal in the buying of retail turning into the selling of retail in the last five months,” Marshall tells host Allison Nathan. “The one area that I would say is an exception here, and something we’re watching very closely, is in the ETF market. ETF inflows have continued at a very consistent rate all through 2020, 2021, and even into 2022. So investors, the buy-and-hold investors, as separate from retail day traders… are continuing to allocate to equities through buying of ETFs.”

Retail investors’ participation in markets is stabilizing. “I think we’re finding our steady state in terms of retail participation in the U.S. equity markets,” Jeria says. “I think it’s going to look like 15% for the near future. It’s higher than the baseline that we had pre-COVID. And we can explain that, again, because of zero commissions, because of the gamification aspect that’s here to stay.”

It seems retail is off the stock picking game but seeks to stay in the big game. But that game has also been unraveling lately with the big names taking it on the chin. Full capitulation needed.

OTHER THAN THAT

- McDonald’s will pay $1.3 billion to settle probes in France where it was accused of dodging taxes by unfairly shifting revenue to Luxembourg and Switzerland. Top financial prosecutor Jean-Francois Bohnert said the total amount to be paid by McDonald’s is two-and-a-half times larger than the taxes it skipped — nearly 470 million euros.

- Lego will invest $1 billion in its first US factory because of rising demand in the Americas.

In One Chinese City, Protesters Find Themselves Thwarted by a Red Health Code Plans to protest in Zhengzhou against banks for freezing deposits were thwarted when would-be protesters’ health codes turned red—prompting accusations authorities were using the Covid tool for social control.

(…) Mr. Ye said that as soon as he arrived in Zhengzhou and scanned the code on his smartphone to exit from the train station, his green code switched color, prompting local officials to confine him in a hotel. Two days later, when he left the region without having been able to carry out his protest plan, the code flipped back to green, he said. (…)

In between the change of colors, Mr. Ye and others say dozens of bank customers who had come to Zhengzhou to protest and whose health codes had also turned red were grounded inside a remote hotel. For Mr. Ye, the setting was familiar. In May, he said, he spent some time confined at the same hotel by local authorities after he and hundreds of bank customers held signs outside the local headquarters of the bank regulator, demanding the return of their savings.

Authorities in Zhengzhou and Henan haven’t provided an official explanation of why the codes of Mr. Ye and others were switched and then switched back. (…)

Pretty bad for confidence in the system; also pretty bad for confidence in banks and access to own funds…