U.S. Initial Jobless Claims Decline; Continuing Claims Range-bound

Seasonally adjusted state initial jobless claims for unemployment insurance declined to 860,000 in the week ending September 12 from 893,000 in the previous week. The Action Economics Forecast Survey anticipated 850,000. (…)

Claims for the federal Pandemic Unemployment Assistance (PUA) program, which covers individuals such as the self-employed who are not qualified for regular/state unemployment insurance, decreased for the first time in four weeks to 658,737 from 868,314. PUA claims are up roughly 170,000 since their near-term low in the week ending August 8. Numbers for this and other federal programs are not seasonally adjusted. (…)

U.S. Housing Starts Decline in August as Multi-Family Weakens

Housing starts declined 5.1% (+2.8% y/y) during August to 1.416 million (SAAR) from 1.492 million during July, revised from 1.496 million. The decline left starts 12.4% below their January peak of 1.617 million. The Action Economics Forecast Survey expected 1.484 million starts in August.

A 22.7% decline (-15.2% y/y) in starts of multi-family units to 395,000 accounted for the drop in starts overall last month. Starts of single-family homes rose 4.1% last month (12.1% y/y) to 1.021 million after surging 10.1% in July to 981,000, revised from 940,000. The latest level was a six-month high, up 50.4% from the April low.

Building permits slipped 0.9% in August (-0.1% y/y) to 1.470 million from 1.483 million in July, revised from 1.258 million. Permits to build single-family homes increased 6.0% (15.6% y/y) to 1.036 million after improving 16.3% in July and 12.6% in June. Permits to build multi-family homes decreased 14.2% (-24.5% y/y) to 434,000 after rising 21.1% in July.

The NY FEd’s latest Weekly Economic Index (WEI):

Goldman Sachs:

The prospects for further fiscal stimulus have dimmed further, as another week has gone by without any progress. At this point, a major stimulus package before the election looks like a long shot and we expect Congress to leave at the end of September without extending the extra unemployment insurance payment, approving another round of stimulus payments, or providing additional support to small businesses or state and local governments.

Next week is likely to bring some clarity. Congress is likely to start moving next week on the final piece of major pre-election legislation, to extend spending authority past September 30, the end of the fiscal year. If fiscal stimulus measures are not included in that bill, or a deal is not announced next week, fiscal stimulus will likely be on hold for the rest of the year. (…)

Failure to pass any additional fiscal measures would likely lead us to downgrade our growth estimates for Q4. By contrast, enactment of the sort of package that President Trump or Speaker Pelosi have both endorsed would likely lead us to upgrade our view for Q4.

Why China’s recovery is not what it seems

(…) As the graph below shows, before 2020 retail sales had grown slightly faster than industrial production, indicating a slow rebalancing in an economy that urgently needed it. But in 2020 that relationship has inverted, with industrial production now growing so much faster than retail sales that it threatens to reverse the past two to three years of China’s limited rebalancing. (…)

What the past few months of economic data tell us is that, not only has sustainable domestic demand barely recovered from the pandemic, but that even this limited recovery has been driven by Beijing’s substantial boosting of the production side of the economy. By expanding public sector investment in logistics and infrastructure, underwriting an expansion of credit to businesses, and otherwise subsidising production, Beijing has bolstered production to create the employment that has indirectly boosted consumption.

Put differently, economic recovery in China (and the world, more generally) requires a recovery in demand that pulls along with it a recovery in supply. But that isn’t what’s happening. Instead Beijing is pushing hard on the supply side, mainly because it must lower unemployment as quickly as possible. It is this push on the supply side that is pulling demand along with it. (…)

China’s “recovery”, in other words, is largely an exacerbation of the problems that have long been recognised by Beijing. It is a supply-side recovery in an economy that urgently needs more domestic demand but that has found it politically very hard to manage the wealth transfers that it requires.

This recovery isn’t sustainable without a substantial transformation of the economy, and unless Beijing moves quickly to redistribute domestic income, it will require either slower growth abroad or an eventual reversal of domestic growth once Chinese debt can no longer rise fast enough to hide the domestic demand problem.

The communist party’s first objective is its own survival. Excerpts from Geopolitical Futures’ Phillip Orchard essay

China’s Trial by Fire

(…) Two weeks ago, in a triumphant speech, Xi said, “The CCP’s strong leadership is the most reliable backbone when a storm hits. The pandemic once again proves the superiority of the socialist system with Chinese characteristics.” (…)

The systemic shock from the pandemic could well have exposed China’s economy as a house of cards. China shut down the bulk of its domestic economy almost overnight. Millions were abruptly out of work. Countless small businesses – which were already weighed down by tariffs and a credit crunch before the pandemic – faltered, searching for rescue from an immature banking system that had already proved ill-suited for meeting the needs of China’s burgeoning private sector. China’s convoluted financial system, already awash in shadow lending and toxic loans, appeared on the brink. Once Beijing was able to reopen most of the economy, it faced a secondary crisis in the form of collapsing demand for Chinese exports as the rest of the world sunk into crisis.

And yet, Beijing has somehow been able to keep its myriad interlocking systemic risks from triggering a cascading crisis. It never even needed to unleash a firehose of stimulus as it did after 2008 – measures that contributed directly to its staggering financial risks today. This week, the Organization of Economic Cooperation and Development predicted that China would be the only one of the world’s 20 leading economies to post positive growth this year. Here, Xi can rightfully take credit for pushing through a series of painful measures to curb financial risk beginning in his first term; these worked better than many expected. Meanwhile, his emphasis on strengthening state-owned enterprises – which in normal times have sapped the economy of its dynamism and are at the core of Western trade grievances – has been validated since SOEs have sopped up surplus labor and kept industrial production humming. Perhaps most important, Beijing’s worst nightmare – a massive spike in unemployment – came true, but without the attendant social unrest. There’s a case to be made that the experience will ultimately make Beijing confident enough to adopt a more sustainable economic model that doesn’t prioritize stable employment at the expense of profitability and dynamism. (…)

Xi’s administration will need all the luck it can get and all the savvy at its disposal because China has no shortage of crises on the horizon. The current pandemic may be under control, but the culture of censorship and institutional rigidity fostered by Xi may keep Beijing unprepared for the next one. The scale of the structural damage on the Chinese economy left behind by the pandemic won’t be fully apparent for years to come. The “grey rhinos” and black swans Xi is always warning about in the financial sector are still out there – and many of Beijing’s critical reform plans aimed at thwarting them have been put on hold. The pandemic, along with the CPC’s increasing dependence on state control, has accelerated the slide toward open hostility between China and the West. The Three Gorges Dam cannot realistically be upgraded. Floods will return. The problems exposed this year are really just the tip of the iceberg.

But to Beijing, the lesson of this year is evidently: trust only the party’s power. Its solution to a dysfunctional public health sector, for example, is to tighten central control over it. The only way to stave off a financial collapse is through painful measures aimed at curbing financial risk, and these can only be implemented with the brute force required to remove opposition and contain the fallout. (…)

Mao may have thrived on a doctrine of perpetual revolution, but Xi appears to be inescapably driven by permanent crises. This mindset is perhaps the inevitable result for a government haunted by China’s history – by the weight of rising public expectation, by the impossible task of meeting the needs of 1.4 billion people, and by the inherent difficulty of trying to make the massive machinery of the state run efficiently through sheer force of central will and ideology. But the downside risk of this mindset for Beijing is obvious – and for China’s neighbors, it’s particularly alarming. Either way, it’s the one Beijing is sticking with, whatever storms may come.

VIRUS UPDATE

Not trending positively in the USA:

Upticks are visible in all regions, even in the NE, if you look carefully:

- France’s daily coronavirus cases rose by more than 10,000 to the highest since the end of lockdown in May, with Health Minister Olivier Veran warning the disease “is again very active” in the country. The uptick in French infections mirrors steady increases across Europe, with the number of new cases in Germany rising Friday by more than 2,000, the most since late April. Portugal on Thursday reported the most new infections in five months, with 770, while Spanish cases rose at a slower pace than the previous day but still by more than 4,500. Health officials blame the increase on social gatherings, especially among younger people, and on travelers bringing the virus back from vacation.

- A surge of Covid-19 cases in London is expected to be announced on Friday, potentially putting the city on track for curbs on socializing in about a fortnight, the Evening Standard said, without saying how it obtained the information. The capital has recorded about 25 cases per 100,000 over the last seven days, rising from 18.8, according to the report.

- India’s epidemic is showing no sign of peaking as the country added more than 96,000 cases overnight, bringing its tally — the highest in the world after the U.S. — to more than 5.2 million. Amid the outbreak, economists and institutions like the Asian Development Bank have cut India’s growth projections from already historic lows. Goldman Sachs now estimates India’s economy will shrink 14.8% for the year through March 2021, while the ADB is forecasting a 9% contraction. The Organization for Economic Cooperation and Development expects India’s economy to shrink 10.2%.

- The infection-fighting antibodies that people with Covid-19 naturally produce appear to decline over time, with 58% of volunteers in one trial showing no sign of them two months after testing positive.

Moderna Vaccine Study Results Could Come in Late October Company also released the guidelines for the shot’s final-stage trial

A large, pivotal study of Moderna Inc.’s MRNA -1.38% Covid-19 vaccine could yield a preliminary answer about whether the shot works safely as early as October, though it’s more likely to be November, the company’s leader said.

Moderna Chief Executive Stephane Bancel said in an interview the timing will depend on rates of infection in the U.S. locations where the trial is being conducted, because the study is comparing whether fewer vaccinated people come down with symptomatic Covid-19 than unvaccinated people.

Researchers will assess this at intervals after a certain number of cases occur, ranging from 53 cases to 151 cases. (…)

Pfizer Chief Executive Albert Bourla, in recent television interviews, also gave an end-October time frame. Its vaccine is being developed with partner BioNTech SE.

If Moderna’s interim results are positive, the company could seek government authorization for emergency use of the vaccine soon thereafter, Mr. Bancel said. That could lead to quick distribution of any available doses, which Moderna has been manufacturing. (…)

Even if the trials provide positive results this fall, most people wouldn’t be able to get vaccinated until next year because supplies will be limited early on. (…)

Goldman, quite interestingly: “Just as safety concerns can lead to trials being ended, compelling statistical evidence can lead to the early disclosure of success; when the drug is compellingly effective and safe, it is unethical to refuse it to those participants in the placebo group and beyond.” So watch for disclosure in mid-to-late October. No announcement could be interpreted negatively.

FLUidity

From RBA’s Richard Bernstein:

I recently ventured to one of America’s largest pharmacy chains to get a flu shot. My doctor emphatically told me to get one because of the potential complications of COVID-19. I made an appointment through the pharmacy chain’s app, but upon arriving I was told that there were no flu shots available. This was the second branch of the particular chain in which I was informed there were no flu shots.

(…) the pharmacist felt obligated to share with me why I couldn’t get my flu shot. (…)

He mentioned:

1. The pharmacy chain can’t keep enough of the flu vaccine in stock and local pharmacies have no idea when new shipments will be delivered. Local

pharmacists have no ability to manage flu shot inventory.

2. The chain doesn’t have enough pharmacists to administer flu shots. If one

comes to the pharmacy with an appointment at a busy time, the pharmacy

might not be able to honor the appointment and one might have to wait well

over an hour because the pharmacist(s) are too busy filling prescriptions. Ill

patients necessarily have priority over preventative medicine.

3. The chain’s app doesn’t have access to inventory, so people are making

appointments only to find, as I did, that there are no flu shots available. (…)It’s typical for people to get flu shots each fall, but there is increased demand

this year because of COVID-19. The pharmacist effectively outlined how the

production and distribution chains can’t handle this year’s increased demand for flu shots.If the US health care system can’t handle increased production and distribution of flu vaccines when there has been advance notice regarding increased demand, how will it cope with the production and distribution of a COVID-19 vaccine? Everyone KNEW more people would need flu shots this year. Yet, there is limited coordination to produce enough flu vaccines and, equally important, to effectively distribute and administer them.

The CDC on August 19:

For the upcoming flu season, flu vaccination will be very important to reduce flu because it can help reduce the overall impact of respiratory illnesses on the population and thus lessen the resulting burden on the healthcare system during the COVID-19 pandemic.

Flu vaccine is produced by private manufacturers, so supply depends on manufacturers. Vaccine manufacturers have projected that they will supply as many as 194 to 198 million doses of influenza vaccine for the 2020-2021 season. (…)

Currently, manufacturers have indicated there are no significant delays in the distribution of influenza vaccine this season. Shipments have begun with doses of vaccine being distributed as production and approval is finalized. Vaccine distribution is expected to go on longer this season because a record number of doses are being produced. CDC will continue to provide weekly updates on total influenza vaccine doses distributed throughout the 2020-2021 influenza season.

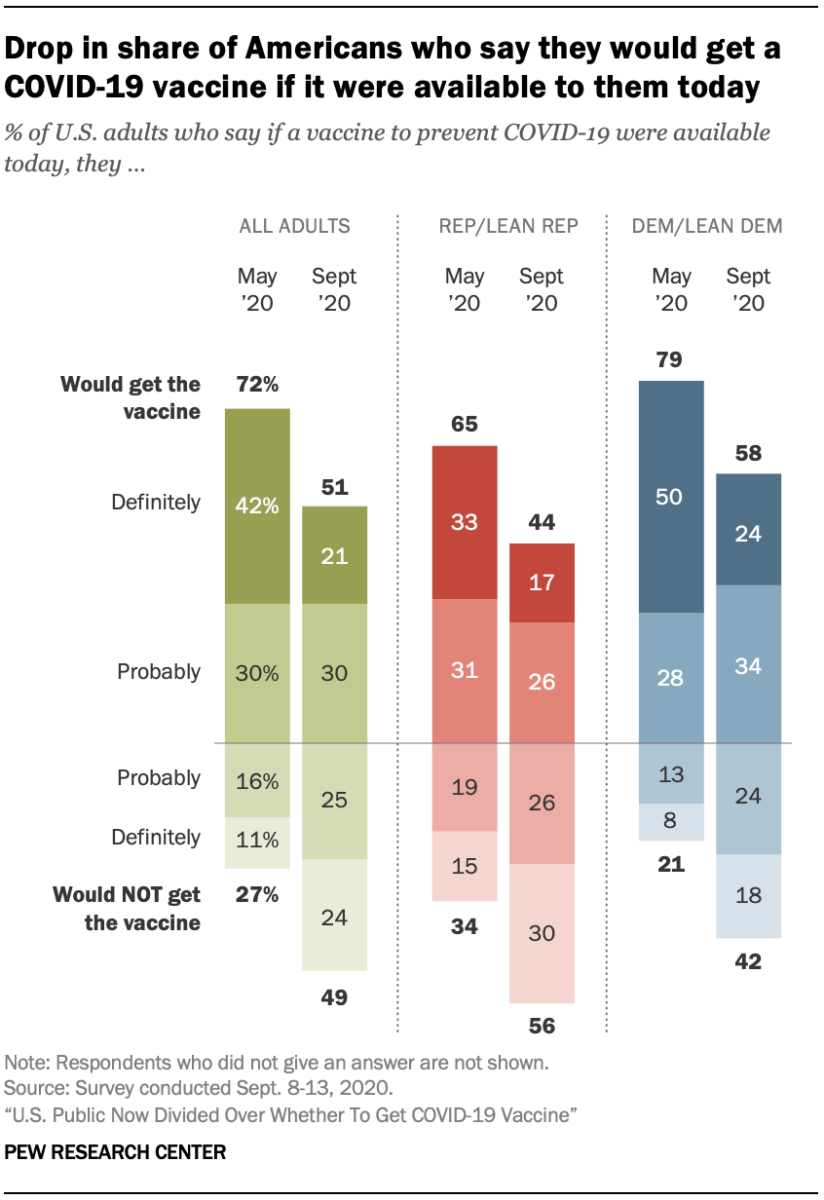

But if Americans don’t care…even Dems are not sure.

EQUITIES

Zero Hedge informs us that “Bloomberg notes that during the week ended September 11, insiders sold $473 million in shares while only buying $9.5 million.” INK’s analysis suggests insiders have been more net sellers since mid-July and that “insiders are sticking to their value strategy of favouring stocks that are cheap relative to their growth prospects. Unfortunately, the value opportunities in the market are rare and are found primarily in the Energy and Financials sectors.”

Inside vs outside:

China’s Stock Bulls Spark a Decoupling in Market Prices Some mismatch between a company’s shares listed on China’s mainland and their counterparts in Hong Kong isn’t unusual. But the growing gulf is creating a strange situation where companies can simultaneously have two radically different valuations.

(…) On Friday the premium for shares trading in Shanghai and Shenzhen, compared with equivalent stocks in Hong Kong, topped 45%, the highest since February 2016, according to the Hang Seng AH Premium Index. (…)

That is partly because trading onshore is dominated by mom-and-pop investors rather than the big institutions that hold more sway in Hong Kong and other international markets. That can mean shorter time horizons and more focus on headlines and price momentum than on corporate fundamentals, investors and analysts say. (…)

And while A and H shares in the same company carry similar economic rights, they aren’t fungible, meaning they can’t be exchanged for each other. (…)

For your enjoyment from Axios:

Jupiter and its enticing moon Europa shine in a new photo by the Hubble Space Telescope, AP reports.

- Hubble snapped the picture last month when the planet was 406 million miles away, and the Space Telescope Science Institute in Baltimore released it yesterday.

Europa, which is smaller than our own moon, appears as a pale dot alongside its giant, color-streaked gas planet.

- Jupiter’s Great Red Spot is unusually red.