Note: I will be travelling in Asia until April 24. Limited equipment and different time zones will limit the frequency and depth of my postings.

Note: I will be travelling in Asia until April 24. Limited equipment and different time zones will limit the frequency and depth of my postings.

US FLASH PMI

Maybe it’s because I am travelling, but I have seen no major media post on this flash PMI. Yet, it may be revealing. The latest FOMC raised the estimated growth rate from 1.4% to 2.1% and the inflation rate from 2.4% to 2.6% but kept 3 rate cuts this year.

The headline S&P Global Flash US PMI Composite Output Index posted 52.2 in March, down slightly from the reading of 52.5 in February but still signalling a solid monthly improvement in business activity at US companies. Output has now risen in each of the past 14 months.

The overall slowdown in the pace of output growth reflected a loss of momentum in the service sector, where activity rose at the weakest pace in three months. While there were some reports of demand improving, anecdotal evidence also suggested that price pressures had restricted the ability of customers to commit to new projects. As a result, the rate of new business growth in the service sector also softened.

More positive was a sharp and accelerated expansion of manufacturing output in March, with the rate of growth the fastest since May 2022 amid a further solid rise in new orders.

Overall, new orders increased at a slower pace than in February. New business from abroad was up marginally as a rise in manufacturing contrasted with a drop in services.

Business confidence jumped to a near two-year high at the end of the first quarter amid signs of a pick-up in the broader US economy. Some service providers also linked confidence to planned marketing activity. While both sectors posted improvements in optimism since February, the jump in confidence was more marked in the service sector than in manufacturing.

While rates of expansion in output and new orders softened in March, this was not the case with regards to employment. The rate of job creation ticked higher and was the fastest in 2024 so far. Staffing levels rose across both sectors, with jobs growth in manufacturing hitting an eight-month high.

Inflationary pressures picked up in March. The rate of input cost inflation quickened to a six-month high amid faster increases across both monitored sectors. Service providers indicated that higher operating expenses generally reflected increasing wages, while rising oil and gasoline costs were often mentioned by manufacturers.

In turn, companies in the US raised their own selling prices at a faster pace. In fact, the rate of inflation was the sharpest in just under a year and stronger than the series average. Respective rates of output price inflation accelerated sharply across both manufacturing and services, quickening to 13- and eight-month highs as companies passed through higher input costs to their customers.

Commenting on the data, Chris Williamson, Chief Business Economist at S&P Global Market Intelligence said:

“Further expansions of both manufacturing and service sector output in March helped close off the US economy’s strongest quarter since the second quarter of last year. The survey data point to another quarter of robust GDP growth accompanied by sustained hiring as companies continue to report new order growth.

“The brightest news came from the manufacturing sector, where production is now growing at the fastest rate since May 2022. Production gains are linked to improving demand for goods both at home and abroad, driving a further upturn in business confidence in the outlook.

“Service providers meanwhile reported a slower pace of expansion than factories, with the rate of increase also moderating slightly compared to February, linked in part to ongoing cost of living pressures. However, service providers have also become increasingly optimistic about the outlook, with confidence striking a 22-month high in March to suggest the broad-based economic expansion seen in March will persist into the summer.

“A steepening rise in costs, combined with strengthened pricing power amid the recent upturn in demand, meant inflationary pressures gathered pace again in March. Costs have increased on the back of further wage growth and rising fuel prices, pushing overall selling price inflation for goods and services up to its highest for nearly a year. The steep jump in prices from the recent low seen in January hints at unwelcome upward pressure on consumer prices in the coming months.”

Ed Yardeni:

During his presser last week, Fed Chair Jerome Powell was asked if he was sticking with what he had told lawmakers two weeks earlier, i.e., “we are not far from …[beginning] to dial back the level of restriction.” That statement was premised on his assumption that incoming data would give the FOMC “more confidence that inflation is moving sustainably to 2.0%.” One week after he said so, February’s CPI and PPI reports were a bit hotter than expected.

Yet Powell chose to blow them off in his presser: “I would say that the story is really essentially the same and that is of inflation coming down gradually toward 2% on a sometimes bumpy path, as I mentioned. I think that’s what you still see. We’ve got nine months of 2-1/2 percent inflation now and we’ve had two months of kind of bumpy inflation.”

In the chart below, the black line is where monthly inflation needs to be to achieve a sustained 2% annual rate. The next debate will be on how to define bumpy!

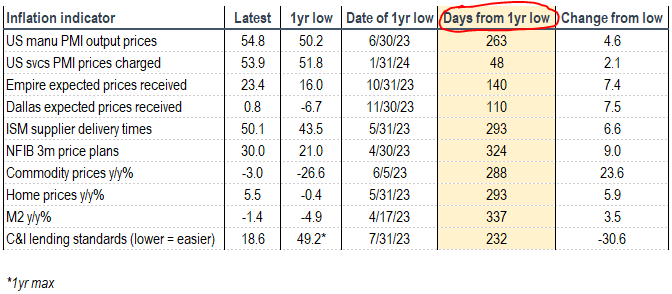

You have surely noted the sharp improvement in the manufacturing PMI sigalling the end of the goods inventory cycle.

Also that “Respective rates of output price inflation accelerated sharply across both manufacturing and services, quickening to 13- and eight-month highs as companies passed through higher input costs to their customers.”

If goods deflation is about to end …

BTW: Source: BofA Global Research

Source: BofA Global Research

Surveillance Special: Powell Serves Up Words Rather Than Answers El-Erian hears a signal of Fed tolerance for higher inflation, and so does the market

In the torrent of words from the Federal Reserve’s statement and Chair Jerome Powell’s press conference, some of the numbers stood out. And underneath the data was an implicit suggestion that the Fed is going to stay quite patient on inflation in order to achieve a soft landing.

“This is a signal and the market is taking it as that, that they will tolerate slightly higher inflation for longer,” Mohamed El-Erian said on the Surveillance Fed special today, unpacking a stand-pat rate decision in which nuance was everything. (…)

“As you see in the equity market today, it’s everybody back in the pool,” BlackRock’s Jeffrey Rosenberg said.

When Powell was asked specifically about recalibrating to something other than the Fed’s 2% inflation target, he offered a lot of words and indicated that this wasn’t the case, but didn’t really address it further. He even suggested that the Fed was going to wait a longer period of time for inflation to get to target.

This, of course, raises a philosophical question: How long can the Fed accept hotter-than-desired inflation before policymakers have de facto adjusted the targeted inflation rate? If you say you’re going to be rich one day but you’re happy only earning a penny a day, is it really your goal to be rich?

William Dudley, the former New York Fed president who is now a Bloomberg Opinion columnist, gently pushed back at Jon’s joking suggestion that Powell’s real message was simply “buy stocks.” But he did detect an important tell in Powell’s response to a question about whether financial conditions were too loose.

“He did not take the bait on financial conditions easing,” Dudley said. “And of course when he doesn’t take the bait on financial conditions easing, what does it do? It causes financial conditions to ease more.”

(…) For context, this is Bloomberg’s measure of financial conditions, and it’s almost as lenient as in 2021 when fed funds were being held at zero:

(…) As it was, the market concluded that the Fed didn’t care about inflation — or was perhaps surreptitiously giving up on lowering it to the official target of 2%. (…)

Unfortunately, Fed governors are no better at predicting the future than the rest of us. Let’s take “long term” to mean four years into the future. This is what the FOMC predicted from 2012 to 2020, with the actual fed funds rate from four years later:

At no point has the fed funds rate been where the FOMC predicted. It stayed far lower than expected throughout the post-crisis decade, then exploded higher — though the governors can be forgiven for not predicting the pandemic. And 2.5% was as high as the rate ever reached in the pre-Covid years. It’s unlikely to fall very far in the future, no matter what the FOMC now thinks.

Should we talk about the FOMC’s inflation prediction record?

Source:

Source:

Source:

Source:  Source:

Source: