The May CPI report was as bad as it could be. Don’t stop at food and energy, inflation is now everywhere.

Inflation Hits New Forty-Year High on Broad Price Gains U.S. consumer inflation reached 8.6% in May as surging energy and food costs pushed prices higher, with little indication of when the upward trend could ease.

May’s increase was driven in part by sharp rises in the prices for energy, which rose 34.6% from a year earlier, and groceries, which jumped 11.9% on the year, the biggest increase since 1979. (…)

Prices for used cars and trucks—a key engine of the past year’s inflation surge—rose 1.8% in May from April, reversing three months of declines. Shelter costs, an indicator of broad inflation pressures, accelerated on a monthly basis in May and were up 5.5%, compared with a year ago.

Airline fares rose 12.6% on the month, the third straight double-digit rise. (…)

“The breadth of inflation pressures in the economy should alarm the Fed,” he said.

On a monthly basis, the CPI jumped a seasonally adjusted 1% in May after rising 0.3% in the prior month. The so-called core-price index, which excludes the often volatile categories of food and energy, increased 0.6% on the month, the same as in April. That compares with an average monthly gain of 0.2% for both measures in the two years before the pandemic. (…)

Food price increases are unusually broad, and every single grocery category measured in the report rose in May from a year ago—most of them by double digits. (…)

The breadth and persistence of these supply problems means that for inflation to ease, demand must come down, said Mr. Knightley of ING. “To get demand into better balance with the supply the onus is on the Federal Reserve to do the heavy lifting,” he said.

Here, there and everywhere:

- Food-at-Home: +11.9% YoY in May; YtD: +15.1% a.r..

- Energy: +34.6% YoY in May; YtD: +38.9% a.r.

- Core CPI: +6.0% YoY in May; YtD: +6.2% a.r.

- Core Goods: +8.5% YoY in May; YtD: +4.6% a.r.

- Core Services: +5.2% YoY in May; YtD: +6.7% a.r.

- Shelter: +5.5% YoY in May; YtD: +5.8% a.r. (last 3 months: +6.6% a.r.)

Taking most essentials out: “All items less food, shelter, and energy”: +6.4% YoY; +7.3% a.r. in the last 2 months

Core Goods ex-vehicles: +7.2% YoY; +4.2% a.r. in the last 2 months

Services less rent of shelter: +6.0% YoY; +12.1% a.r. in the last 2 months.

Medical Care: +3.7% YoY; +4.9% a.r. in the last 2months.

The Atlanta Fed’s sticky-price consumer price index —a weighted basket of items that change price relatively slowly—increased 7.5% a.r. in May, following a 7.1% increase in April. On a YoY basis, the series is up 5.2%. The flexible cut of the CPI—a weighted basket of items that change price relatively frequently—increased 27.9% a.r. in May and is up 18.5% YoY.

- On a core basis (excluding food and energy), the sticky-price index increased 7.3% a.r. in May, and its 12-month percent change was 5.0%. Three-month a.r.: +6.8%.

")

- Inflation May Soon Ease, but Not Enough Excess inventories at retailers might soon act against inflation, but it remains far too high for the Federal Reserve to ease off tightening

(…) The heady demand that the pandemic set off for goods, in combination with supply-chain snarls and the wherewithal to spend provided by government relief programs, are a big part of why inflation has been running so hot. (…)

So after nearly two years of watching prices on household goods go nowhere but up, consumers might be about to see some of them come down.

That could put a dent in the inflation figures. For example, according to the Labor Department, May’s 9.7% increase in prices from a year earlier for household furnishings and supplies—a category that includes appliances and furniture—accounted for about a half percentage point of the gain in core prices.

(…) new- and used-vehicle prices rose 13.7% from a year earlier in May, and contributed about 1.4 percentage points to the gain in core prices. (…)

It is reasonable to expect retailers’ inventory woes to contribute to an easing in inflation in the months ahead. But the Fed is likely to view that as an isolated phenomenon. Absent signs of cooling elsewhere, it is less reasonable to expect the Fed to slow its pace of rate increases.

Still this fixation on goods. For the record, again,

- core goods account for 21.4% of the CPI basket, contributing 1.8% to the 6.0% increase in core prices in the last year

- core goods ex-vehicles, new and used: 17.4%, contributing 1.2% to the 6.0% increase in core prices in the last year

- household furnishings and supplies: 4.0%, contributing 0.4% to the 6.0% increase in core prices in the last year

- new- and used-vehicles: 9.1%, contributing 1.2% to the 6.0% increase in core prices in the last year

Yes, goods inflation will eventually ease, even deflate as rising supply overcomes waning/falling demand. Were core goods prices to immediately return to their February 2020 level, their 12.6% decline would reduce CPI by 2.7% to 3.3% from its current 6.0% level, ceteris paribus.

But ceteris non paribus. Perhaps we will get great crops (during La Nina?) and food prices will ease, and perhaps oil prices will stabilize unlike what most “experts” predict. Let’s hope.

But the biggest problem is services (60.3% of the CPI) and the close link between services prices and wages. Service providers’ two most important cost items are labor (sticky) and energy (flexible but geopolitical).

")

Wages were up 5.0% YoY in Q1’22 per the Employment Cost Index. But the Atlanta Fed median wage tracker was up 6.1% during the 3 months ended in May (+6.5% for May alone). Wages in services are also up 6.0% in May. And, so far, there has been no offset from measured productivity, down 1.8% annualized in the last 3 quarters.

![]()

The inflation squeeze is pushing many workers to seek better income and the low unemployment rate gives them the upper hand. Wages for job switchers were up 7.5% YoY in May and companies must adjust pay for their loyal employees accordingly.

The FOMC is very clear: it wants to avoid a wage/price spiral and must therefore curb demand for labor and increase labor availability.

But the unemployment rate never really increases outside of recessions:

And reducing the number of employed persons always requires a recession. The occasional soft landings don’t do the job.

Jay Powell knows this, having already invoked Paul Volcker (there’s never been a Volcker put), but he made sure we know what’s really at stake in a May 12 interview:

“The process of getting inflation down to 2 percent will also include some pain, but ultimately the most painful thing would be if we were to fail to deal with it and inflation were to get entrenched,” Mr. Powell said, speaking during an interview with Marketplace on Thursday. (…)

“If things come in better than we expect, then we’re prepared to do less,” Mr. Powell said. “If they come in worse than when we expect, then we’re prepared to do more.”

Well, the May CPI certainly came in much worse than expected. In the same interview, Mr. Powell said:

“There are huge events, geopolitical events going on around the world, that are going to play a very important role in the economy in the next year or so,” Mr. Powell said on Thursday. “So the question whether we can execute a soft landing or not, it may actually depend on factors that we don’t control.”

Indeed, uncontrolled factors are quickly doing part of the dirty job for the Fed:

This next chart plots the YoY change in inflation on life’s essentials (food, energy and rent, weighted), now +9.4%, the highest since 1980. As mentioned above, CPI less food, shelter, and energy is up 6.4% YoY, and +7.3% a.r. in the last 2 months. The squeeze is total:

Deflating hourly wages with CPI-Essentials shows the rude shock currently absorbed by the average American. Wages were up 5.7% in May but were actually down 3.7% after inflation on essentials. Excluding the pandemic, previous periods with similar shocks forced consumers to drastically cut discretionary expenditures, particularly durable goods.

Real durables are down 7.1% YoY in May but that is against the high pandemic base. In reality, durables consumption is still 25% above its pre-pandemic level while real wages (per the ECI) are down more than 6% and falling.

There is no real demand left for durable goods other than vehicles. But prices of vehicles have skyrocketed 50.6% above their pre-pandemic levels while interest rates are rising rapidly. Prices will surely retreat, but how quickly and how much demand will there be left given higher financing costs amid falling real wages?

Actually, the Fed’s crusade to reduce demand for goods could be fulfilled beyond its dreams. Core goods inflation will surely decline, in fact probably deflate given current high inventories, but unless food, energy and rent costs, not directly impacted by domestic macro trends, abate, the income squeeze will endure.

The May CPI report, and the bond market reaction, will embolden the hawks to demand an even more restrictive monetary policies, right when the fiscal side is hurting, and when retail sales and the housing market, the entire consumer sector for that matter, are entering a very difficult period.

We can hope that “revenge spending” on travel and entertainment will more than offset waning goods consumption. But how revengeful can one really afford to be when airfares, resorts, concerts and restaurants cost 20-35% more than in 2019?

Mr. Powell will finally be right on something: it will be painful. But it may get more painful than needed if the hawks gain the upper hand right when the consumer is priced out and already retrenching.

Recall that Amazon grew its North American sales 8% in its Q1 ended in March. Target and Walmart both said that sales got weaker in March and really soft in April. They reported same store sales growth of 3.3% and 3.0% respectively for their quarter ended in April. CPI core goods-ex-vehicles is up 7.2% YoY.

Never mind black swans, black hawks are the bigger threat.

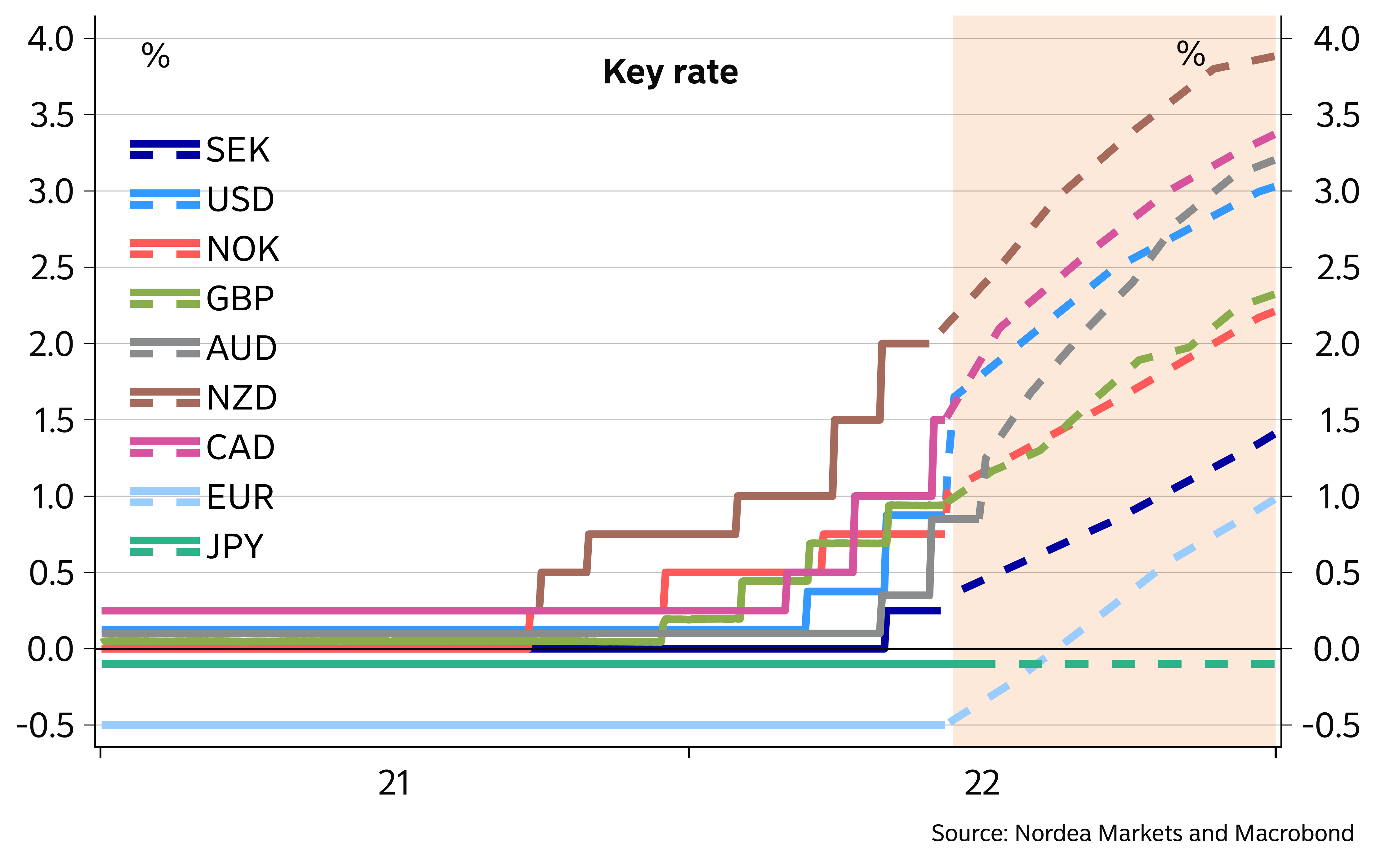

- “The inflation data are unlikely to show a “clear and convincing” deceleration until December. The FOMC is likely to respond to the firmer inflation print and the rise in long-term inflation expectations with a resolutely hawkish message at the June meeting, in addition to the 50bp rate hike it is set to deliver. This should come across clearly in the statement, the economic projections, and the dots. We expect the FOMC to revise the policy guidance in its statement to say that the Committee “anticipates that raising the target range expeditiously will be appropriate until it sees clear and convincing evidence that inflation is moderating.” (Goldman Sachs)

- Fed Task Gets Tougher, Putting 75-Basis-Point Hike Back in View

- Larry Summers Says Fed Forecasts Look Ridiculous, Warns on Rate Delay

(…) “It’s pretty clear that peak-inflation theory, like ‘transitory’ theory is kind of wrong,” Summers told Bloomberg Television’s “Wall Street Week” with David Westin. “The Fed’s forecasts from March, saying that inflation would be coming down to the 2s by the end of the year was, frankly, delusional when issued, and looks even more ridiculous today.” (…)

“The debate has been between 25 and 50 basis point moves a couple months from now,” Summers said. “I think a more fruitful deliberation would be between 50 and 75 basis points.” (…)

(…) Wholesale gasoline prices point toward an increase in average U.S. gasoline prices from $5 to $5.50 over the next couple of weeks. Critical to the forecast for growth and inflation is that energy prices, including gasoline, are near their peaks and will steadily decline through the rest of this year and into next.

What if we’re wrong? (…)

In the first scenario, U.S. prices at the pump average $6 per gallon in the latter half of 2022. In the second scenario, prices surge to $7 per gallon. In both scenarios, gasoline prices quickly return to our baseline forecast by mid-2023. A general rule of thumb is that a $10 increase in the price of a barrel of oil results in a $0.25 increase in the price of a gallon of gasoline.

Further, every penny change in retail gas prices adds or subtracts $1.28 billion in consumer spending over the course of a year. Therefore, the economic costs of higher gasoline prices increase quickly and are likely nonlinear. Gasoline prices at $6 or $7 would be psychological thresholds and would likely weigh heavily on consumer sentiment and potentially increase the economic costs of higher prices at the pump.

Gasoline prices at $6 per gallon shave 0.4 percentage point off U.S. GDP growth in the third quarter, dragging output from the annualized growth rate of 3.6% in our baseline to 3.2%. In the final quarter, the hit to GDP growth is 1.2 percentage points. The decline is a function of a reduction in real consumer spending.

U.S. consumer prices, which we forecast to moderate steadily after peaking in the first half of 2022, instead accelerate to an average of 8.3% in the third, more than a percentage point higher than our baseline. In the fourth quarter, prices rise 7.3%, 1.4 percentage points hotter than our forecast of a 5.9% increase. (…)

At $7 per gallon, GDP growth in the U.S. slumps to 3.1% in the third quarter and 1.1% in the fourth. This marks a half percentage point and 1.6-percentage point reduction from our baseline, respectively. The inflationary impacts of $7 gas are similarly pronounced. The CPI jumps 8.6% in the third quarter and 7.7% in the fourth.

- Inflation Will Crank Up Your Air-Conditioner Bill This Summer All those boxes indicate record-high Sunday forecasts. Texas electricity use soared to an all-time high yesterday, breaking a record set in Aug. 2019. (Bloomberg)

Photo: Weatherbell.com (via Axios)

Photo: Weatherbell.com (via Axios)

We could well be about to witness the mother of all perfect storms for consumers: broad inflation, spiking interest rates, layoffs and continued pressures on food and energy prices even as the economy weakens.

Can the one percenters, or even the top 20-percenters, save the day for everybody else, given their wealth and high excess savings? They also eat, drive and borrow. They also own a lot of financial assets which are not performing too well in this environment.

Perhaps a different kind of squeeze, but a squeeze nonetheless: an unwelcome bear hug after having splurged on houses and other stuff at inflated prices!

BTW:

Luxury U.S. Housing Market Is Cooling Economic uncertainty fueled by rising interest rates, volatile stocks and frothy prices is leading to a luxury slowdown, with a housing bubble in Austin near bursting.

(…) The number of luxury homes—defined as the top 5% of the market—that sold during a three-month period from Feb. 1 to April 30, 2022, dropped 18% compared with the number of sales during the same period in 2021, according to a new report from the real-estate brokerage Redfin. (…)

Prices are still holding, but they are unlikely to keep reaching new heights as buyers retreat, according to Sheharyar Bokhari, a Redfin senior economist. (…)

Richard Steinberg, a luxury real-estate agent at Compass, said he has been having “the price-reduction conversation“ with clients on at least 50% of his exclusive listings. Without offers or the promise of deals, many of them will have no choice but to listen, he said.

Mr. Steinberg said he sees the greatest reduction in activity on properties priced between $2 million and $5 million, a price range in which he says buyers typically rely on mortgage financing and are dealing with increased interest rates. Above $5 million, buyers are less concerned about interest rates, but they are expecting that the shifts in the financial markets will result in bargains on the real-estate front. (…)

- US inflation is now middle of the pack, 48th of 111 countries covering the most up-to-date data available

Source: Jim Reid, Deutsche Bank (via https://ritholtz.com/)

U.K. Economy Shrinks for Second Month as Outlook Dims The economy contracted again in April, as surging inflation weakened consumer spending, and programs designed to contain the spread of Covid-19 were wound down.

Jobless Rate Hits New Record Low in Canada, Wages Accelerate

The economy added 39,800 jobs in May, Statistics Canada reported Friday, surpassing the 27,500 gain anticipated by economists. The nation’s jobless rate fell to 5.1%, from 5.2%, bringing it to the lowest in data going back to 1976.

Masking the overall gain in net new jobs was a massive shift of part-time employment to full-time — another sign of a tight labor market. Full-time employment jumped by 135,400, with part-time jobs down 95,800.

The average hourly wage rate was up 3.9% from a year ago, an acceleration from 3.3% in April. (…) Wage gains for permanent workers hit 4.5%, up from 3.4% in April. (…)

The bulk of the new job gains came from the unemployment ranks, with the labor force growing by just 11,800 during the month. (…)

Canada’s economy has added more than 1 million jobs over the past year, with employment nearly half a million [+2.6%] above February 2020 levels. [USA: -0.5%]

The unemployment rate, based on U.S. methodology, was 4.1% in Canada in May, versus 3.6% south of the border.

Note that employment in goods manufacturing declined 43k in May, in spite of very positive PMI surveys.

A wave of layoffs and hiring freezes in the American tech sector is set to hit Canada hard, industry watchers say. They warn that although job cuts have already happened here, bigger reductions lay ahead.

“The message everyone is receiving is: ‘Protect your capital.’ There will be many more layoffs, no question,” said Jacques Bernier, managing partner with Montreal “fund-of-funds” firm Teralys Capital.

“It’s going to be a bloodbath,” said billionaire Vancouver investor and entrepreneur Markus Frind, who owns a majority of online furniture seller Cymax Group Inc. and backs several venture capital firms, all of whom are telling their companies to review their spending plans. “It’s going to be way worse than 2008,″ when the credit crisis sparked a recession. (…)

Valuation Trauma Is Refusing to End for S&P 500 in Free Fall

(…) Beyond just the real-time upheaval, one of the more tangible consequences of the central bank’s campaign has been to make fixed-income investments increasingly more attractive versus equities. One measure, a version of what’s known as the Fed model in which the S&P 500’s valuation is plotted against that of investment-grade bonds, is flashing ever-more worrisome signals for stocks.

Relative to its price, the S&P 500 “pays out” just under 5% in earnings as of Thursday, data compiled by Bloomberg show, versus the 4.4% average yield on investment-grade corporate bonds. The 0.54 percentage-point difference is close to the slimmest advantage that equities have held over credit since 2010.

Juxtapositions like that are making it hard to dive back into riskier assets as investors size up which ones will bear the brunt of a hawkish central bank bent on cooling growth.

“In a downturn, earnings will be hit, which will impact equities directly, even if multiples don’t change, while the vast majority of investment-grade companies have plenty of room to avoid credit-rating downgrades,” said Peter Tchir, head of macro strategy at Academy Securities. “The corporate bond yield versus the S&P 500 dividend yield seems attractive to me outright, let alone when I’m worried about the economy.” (…)

“There’s more room to drop for equities as stock investors are still in the denial stage about the Powell Put being gone and inflation being both a demand and supply shock,” Gokhman said. “Conversely, bond investors are wavering between the depression and acceptance stages. Sad as that sounds, it’s a better place to be.” (…)

The valuation correction has not run its course yet. At today’s pre-opening of 3800, the Rule of 20 P/E is 23.7, still 15% overvalued. This chart only uses actual data, no forecast.

Some may want to use the conventional P/E and find comfort at 16.1x forward EPS.

It is only 6.8% above its median but

- that does not account for rising inflation and

- it uses current forward earnings, 9.5% above trailing EPS and far from assuming any recession risk.

Earnings pre-announcements remain negative as we approach the end of Q2. More companies have pre-announced so far in Q2 than at the same time in Q1. Factset comments:

More S&P 500 companies have issued negative EPS guidance for Q2 2022 compared to recent quarters as well. At this point in time, 102 companies in the index have issued EPS guidance for Q2 2022, Of these 102 companies, 71 have issued negative EPS guidance and 31 have issued positive EPS guidance. This is the highest number of S&P 500 companies issuing negative EPS guidance for a quarter since Q4 2019 (73). The percentage of companies issuing negative EPS guidance for Q2 2022 is 70%, which is above the 5-year average of 60% and above the 10-year average of 67%.

The highest negative ratios are in Consumer Discretionary (83%- soft sales, lower margins) and Industrials (77%-often-cited strong USD).

Analysts are reacting, mainly on S&P 500 companies…

…but remain hopeful that all is good with EPS growth in Q2 (5.4% vs 6.8% on April 1), in Q3 (11.1% vs 10.6%) and in Q4 (10.9% vs 10.4%), continuing into 2023 (9.6% vs 9.8%).

They have never gone through inflation…

Meanwhile, other “investors” are having another difficult lesson:

Bitcoin Falls to Late-2020 Levels Amid Crypto Selloff This year’s rout in bitcoin deepened, with the world’s biggest cryptocurrency dropping amid a broader selloff fanned by concerns about rising U.S. interest rates.

![]() Almost Daily Grant’s remembers that (my emphasis)

Almost Daily Grant’s remembers that (my emphasis)

Last fall, Celsius raised $750 million in an upsized series B fundraising round, valuing the company at $3.5 billion. Duly emboldened, CEO Alex Mashinsky told Cointelegraph that he expected his company’s valuation to “double or triple” from that figure within the following 12 months. Underpinning that confidence, a relationship with an infamous crypto cornerstone: As Mashinsky informed Bloomberg last fall, Tether, the progenitor of so-called stablecoins under the same name, loaned $1 billion to Celsius at an interest rate of roughly 5% to 6%.

Stinky, stinky…

Other than that:

- Inflation Cuts Online Fashion Down to Size Pure e-commerce retailers may have better growth prospects, but costs are rising faster for home delivery than for physical stores.

- Without Cheap Russian Energy, Some European Factories Must Close Industrial energy costs are soaring in the wake of Russia’s war on Ukraine, hobbling European manufacturers’ ability to compete in the global marketplace.

- Mexico Takes Aim at Private Companies, Threatening Decades of Economic Growth Populist President Andrés Manuel López Obrador is seeking to reclaim state control over the oil-and-gas and electricity sectors. “It’s a closing off of Mexico.”

WHAT A WONDERFUL WORLD!

- China Warns of Risk of War Over Taiwan While Pledging Peace

- China vows to ‘crush’ any attempt by Taiwan to pursue independence

- U.S. Defense Secretary Warns That China’s Military Is Increasingly Aggressive Lloyd Austin says Chinese aircraft and ships are engaging in provocative behavior in the Indo-Pacific region.

- US pledges to maintain military capacity to defend Taiwan Lloyd Austin warns China against ‘provocative’ activity at Asian defence forum

![image_thumb[6]](https://i0.wp.com/www.edgeandodds.com/wp-content/uploads/2022/06/image_thumb6.png?ssl=1 "image_thumb[6]")

![image_thumb[8]](https://i0.wp.com/www.edgeandodds.com/wp-content/uploads/2022/06/image_thumb8.png?ssl=1 "image_thumb[8]")

(

(